Cardinal Health’s CAH fiscal third-quarter results suggest that the company’s “Other Growth Businesses” are evolving from complementary assets into a meaningful profit engine, underscoring management’s strategy to diversify beyond its traditionally low-margin pharmaceutical distribution business.

In the third quarter of fiscal 2026, revenues from the segment surged 34% to $1.7 billion, while segment profit climbed at an even faster rate of 52%, highlighting the increasing earnings leverage of these higher-margin operations.

The momentum was broad-based, with strength coming from Nuclear and Precision Health Solutions (NPHS), At-Home Solutions and OptiFreight Logistics. NPHS continued to benefit from rapid adoption of theranostics, where revenues gained more than 30%, supported by Cardinal Health’s investments in isotope production capabilities and rising demand for targeted cancer therapies. Management emphasized growing engagement with pharmaceutical innovators, which includes the Actinium-225 platform that is already supporting more than 15 clinical trials globally.

At-Home Solutions is benefiting from the secular shift of healthcare services toward home-based care. Demand remained strong, aided by the successful integration of the Advanced Diabetes Supply (ADS) acquisition. Cardinal Health has now onboarded nearly 500,000 new patients and about 1,000 employees. The company is also migrating ADS volumes into its distribution centers, creating scale efficiencies and a stronger chronic-care platform. The business is also generating synergies with pharma through its ContinuCare Pathway program, which now serves 165,000 patients.

OptiFreight Logistics added another layer of growth, with revenues increasing nearly 20%, reflecting rising demand for cost-efficient healthcare logistics solutions. Together, these businesses are not only diversifying Cardinal Health’s revenue mix but also expanding exposure to faster-growing, higher-margin healthcare niches — potentially making them an increasingly important driver of long-term profitability.

Peer Update

Align Technology’s ALGN future growth appears increasingly tied to deeper penetration of digital orthodontics and improved operating leverage. In the first quarter of 2026, the company reported record clear aligner shipments of 686,000 cases, supported by double-digit growth in international markets, especially APAC, EMEA and Latin America, while North America stabilized.

Future demand drivers for ALGN include expanding adoption among teens and children through products such as Invisalign First and Palatal Expander. Apart from product adoption, growing DSO partnerships, and financing initiatives are improving affordability and case conversion. Align Technology’s profitability is likely to be driven by AI-enabled treatment planning, lower refinement rates, operational efficiencies and higher-margin product configurations requiring fewer aligners, supporting sustained margin expansion.

CONMED’s CNMD long-term growth and profitability outlook is likely to be driven by its focused portfolio strategy and higher-margin surgical platforms. Following the strategic divestiture of its gastroenterology business, management is concentrating resources on AirSeal, Buffalo Filter and BioBrace, which target attractive growth categories in the healthcare segment.

AirSeal should benefit from increasing robotic and laparoscopic surgeries, where penetration is still low. The U.S. laparoscopic procedures exceed 3 million annually, representing significant growth opportunity. Buffalo Filter has a favorable tailwind from expanding smoke-free operating room legislation, while BioBrace adoption continues to strengthen as surgeons embrace biologic soft-tissue repair solutions. Improving supply-chain reliability and a richer product mix should also support margin expansion and profit recovery.

CAH’s Price Performance, Valuation and Estimates

Shares of CAH have lost 2.4% so far this year compared with the industry’s 8.2% decline.

Image Source: Zacks Investment Research

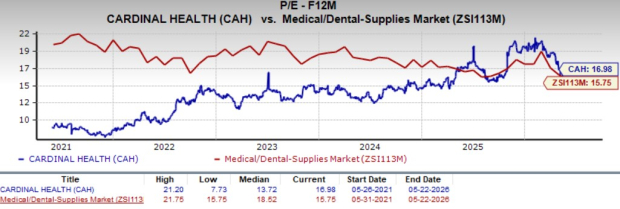

From a valuation standpoint, Cardinal Health trades at a forward price-to-earnings ratio of 16.98, above the industry average. It is also higher than its five-year median of 13.72. CAH carries a Value Score of A.

Image Source: Zacks Investment Research

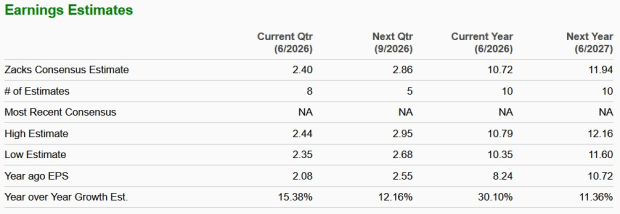

The Zacks Consensus Estimate for Cardinal Health’s fiscal 2026 earnings implies a 30.1% rise from the year-ago period’s level, followed by 11.4% expected growth in fiscal 2027.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CONMED Corporation (CNMD): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).