Kontoor Brands, Inc. KTB expects to unlock faster growth following the divestiture of Lee to focus entirely on Wrangler and Helly Hansen, which management views as iconic brands with substantial global growth opportunities. The planned divestiture of Lee is expected to reduce operational complexity, support more focused investment decisions, accelerate execution and improve returns.

Kontoor Brands believes Wrangler can become a $5 billion global brand by 2030, supported by significant expansion opportunities across women’s apparel, non-denim categories and digital capabilities. Management highlighted that Wrangler’s female business currently represents only 10% of revenue despite the women’s denim market being larger than men’s, creating a substantial growth runway. The company also plans to accelerate investments in AI, loyalty programs and U.S. full-price store expansion, particularly across Western and Southern U.S. markets.

Helly Hansen continues to represent a significant global growth opportunity for Kontoor Brands as well, with management expecting the brand to become a major contributor to future growth and profitability. The company highlighted substantial expansion potential in the United States, where Helly Hansen remains underpenetrated despite being one of its fastest-growing markets. Management plans to accelerate investments across sport and workwear through increased spending on talent, direct-to-consumer capabilities, wholesale expansion and brand-building initiatives, while targeting a clear path toward double-digit growth in its home market.

Kontoor Brands also noted that streamlining its portfolio is expected to free up enterprise-level resources and investment capacity, allowing the company to further advance strategic initiatives and better position the brand for accelerated growth beginning in 2027 and beyond. Overall, the company’s sharper focus on Wrangler and Helly Hansen could accelerate long-term growth by unlocking higher-margin opportunities, expanding global reach and strengthening investments in digital, women’s apparel and outdoor categories.

The Zacks Rundown for KTB

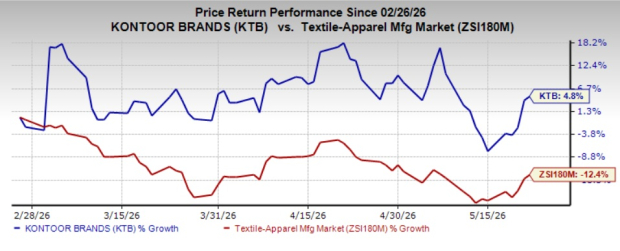

Shares of KTB have gained 4.8% in the past three months against the industry’s decline of 12.4%.

Image Source: Zacks Investment Research

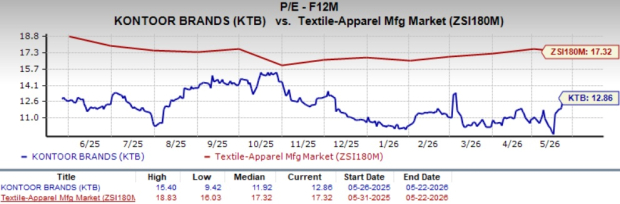

From a valuation standpoint, KTB trades at a forward price-to-earnings ratio of 12.86X, lower than the industry’s average of 17.32X. KTB currently carries a Zacks Rank #4 (Sell).

Image Source: Zacks Investment Research

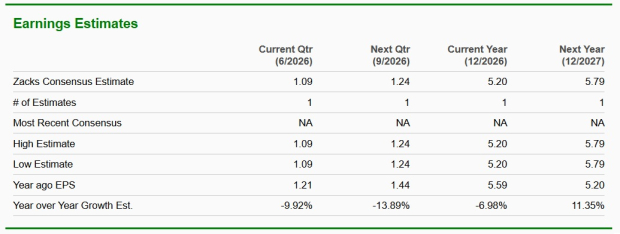

The Zacks Consensus Estimate for KTB’s current fiscal year earnings implies a year-over-year decline of 7%, while the same for the next fiscal year earnings implies a 11.4% year-over-year increase.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

Vince Holding Corp. VNCE provides luxury apparel and accessories in the United States and internationally. It operates through Vince Wholesale and Vince Direct-to-Consumer segments. At present, the company carries a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for VNCE’s current fiscal-year sales implies growth of 4.5%, and the same for earnings implies a decline of 15.9% from the year-ago figures. VNCE has delivered a trailing four-quarter earnings surprise of 647.2%, on average.

Columbia Sportswear Company COLM engages in the design, development, marketing, and distribution of outdoor, active, and lifestyle products in the United States, Latin America, the Asia Pacific, Europe, the Middle East, Africa, and Canada. At present, COLM carries a Zacks Rank of 2.

The Zacks Consensus Estimate for COLM’s current fiscal-year sales and earnings implies growth of 2.6% and 0.8% from the year-ago figures. COLM delivered a trailing four-quarter earnings surprise of 44.1%, on average.

Superior Group of Companies, Inc. SGC produces, manufactures, and sells promotional products and branded uniforms, and healthcare apparel and accessories in the United States and internationally. At present, SGC carries a Zacks Rank of 2.

The Zacks Consensus Estimate for SGC’s current fiscal-year sales and earnings implies a growth of 2% and 28.3%, respectively, from the year-ago figures. SGC delivered a trailing four-quarter negative earnings surprise of 81.9%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Columbia Sportswear Company (COLM): Free Stock Analysis Report

Vince Holding Corp. (VNCE): Free Stock Analysis Report

Superior Group of Companies, Inc. (SGC): Free Stock Analysis Report

Kontoor Brands, Inc. (KTB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).