Valued at a market cap of $31.6 billion, Workday (WDAY) stock is down almost 60% from all-time highs. Investors are worried about AI replacing software services companies such as Workday, which has driven its stock price lower in the past year.

However, Workday just posted its best first-quarter growth in new bookings in five years, beat Wall Street estimates on both earnings and revenue, and raised its full-year profit margin forecast. For a tech stock that has been beaten down in 2026, this report could be a meaningful turning point.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comThe numbers suggest Workday's artificial intelligence strategy is working, and the market is starting to believe it.

Workday Beats Earnings and Lifts its Margin Outlook

On May 21, Workday reported fiscal first-quarter results that came in ahead of analyst expectations across the board.

The company posted adjusted earnings of $2.66 per share, topping the $2.51 consensus estimate, while revenue of $2.54 billion edged past the $2.52 billion forecast. Net income jumped to $222 million from just $68 million a year earlier, a more than threefold increase.

Subscription revenue, the company's core business, rose 14% year-over-year to $2.35 billion. The 12-month subscription backlog grew 15.5% to $8.81 billion, a sign that clients are committing to more spending ahead. Operating cash flow surged 52% to $696 million. For the full fiscal year 2027, management raised its non-GAAP operating margin guidance to 30.5%, up from the 30% it projected as recently as February.For the second quarter, Workday called for subscription revenue of roughly $2.46 billion and a 30% adjusted operating margin, both in line with or slightly above analyst expectations.

Why Workday's AI Momentum Is Key to Growth

Workday CEO Aneel Bhusri, who returned to lead the company earlier this year, replacing Carl Eschenbach, called the first quarter as the "best first quarter of new ACV growth in five years." More than a quarter of all expansion revenue from existing customers came directly from AI products. Deals that included AI were more than 50% larger on average than those that did not.

The company's agentic AI solutions are now approaching $500 million in annualized revenue. New bookings from these products grew more than 200% year-over-year in the first quarter. The number of customers using at least one organically built Workday agent more than doubled quarter-over-quarter to over 4,000.Workday also announced two new AI products at its Sana AI Summit in New York: a travel and expense agent that automates bookings, receipts, and policy checks, and an IT service management tool built on top of the company's existing HR and payroll data.

These are the kinds of moves that show Workday is not just defending its existing turf but expanding into new categories. "The 150th feature in HR or finance is not going to move the needle for our business," Bhusri said on the earnings call. "The next agentic application will."

The Bottom Line on Workday Stock

Investors have spent much of 2026 worrying that generative artificial intelligence will disrupt large enterprise software players like Workday. This quarter pushes back hard on that thesis.

Workday holds a genuinely differentiated position.

It manages over 80 million users and processes roughly 1.4 trillion transactions annually, giving it a data foundation that pure AI startups simply cannot replicate overnight. Its business process and security framework give AI agents the guardrails enterprises require before they will trust automation with payroll or financial close processes.Bhusri said he wants to keep headcount as flat as possible through the fiscal year while using the company's own tools and third-party AI to drive productivity. That is a credible path to continued margin expansion, which is exactly what long-term shareholders want to see.

www.barchart.com

www.barchart.comAnalysts tracking Workday stock forecast revenue to increase from $9.55 billion in fiscal 2026 (ended in January) to $15.8 billion in fiscal 2031. In this period, free cash flow is projected to improve from $2.78 billion to $4.87 billion. If WDAY stock is priced at 15x forward FCF, which is below its three-year average of 27x, it could more than double within the next four years.

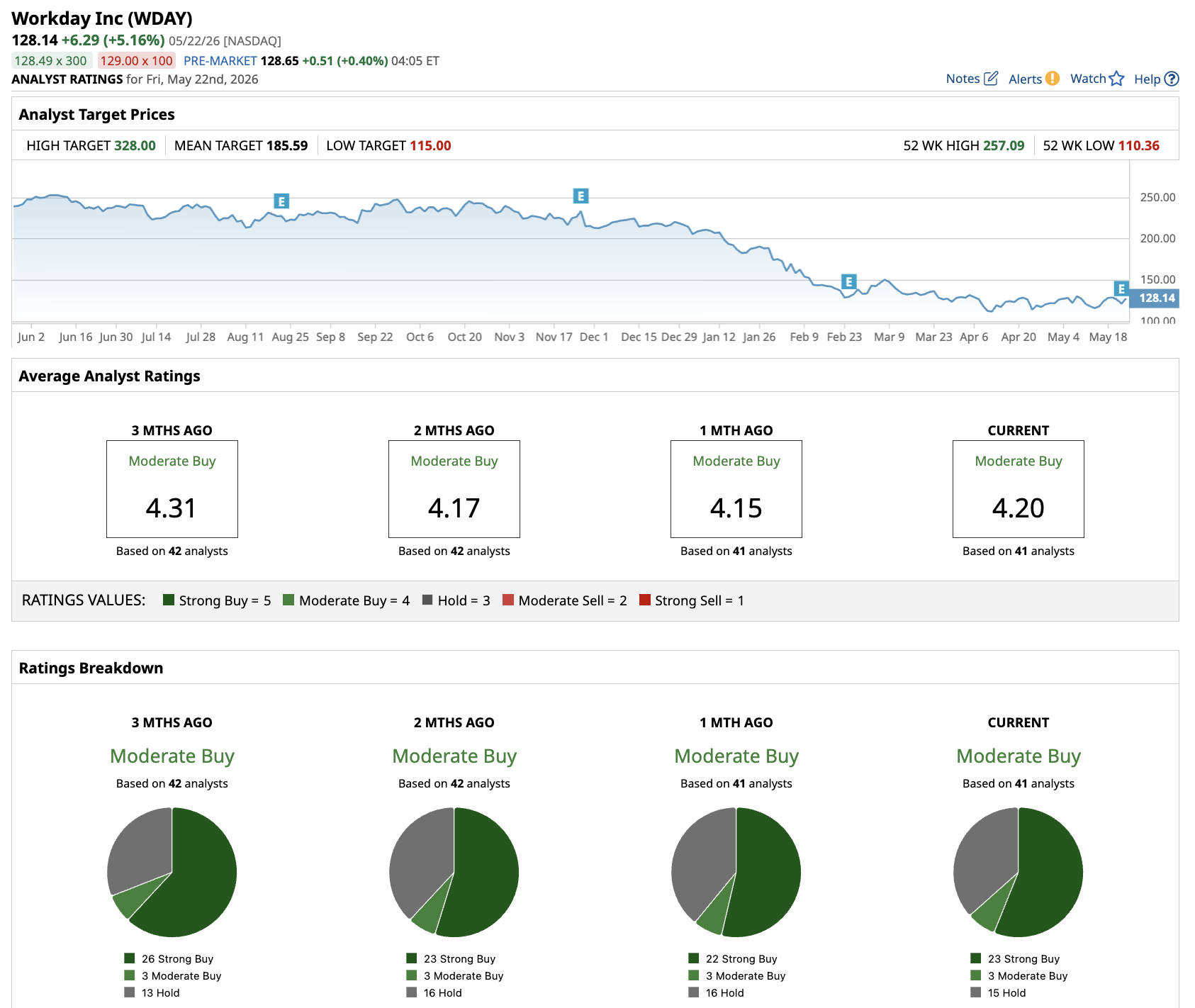

Out of the 41 analysts covering Workday stock, 23 recommend “Strong Buy,” three recommend “Moderate Buy,” and 15 recommend “Hold.” The average Workday stock price target is $186, above the current price of $128.

Workday is not a turnaround story. It is a leading enterprise platform that, after a rough stretch, is showing it can grow with AI rather than be disrupted by it. Investors who have been sitting on the sidelines should take notice.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.