When it comes to absolutely mindboggling returns, you’d be hard-pressed to beat Micron Technology (MU). Since the start of the year, MU stock has gained nearly 214%, easily triggering a 100% Strong Buy ranking from Barchart’s Technical Opinion indicator. And why not? Over the past 52 weeks, the security has skyrocketed to the tune of roughly 830%. It’s a life-changing investment for many but that’s also where the math problem lies.

That MU stock is a massively superior investment is a factual observation. Further, the thesis risk is relatively low (and some might argue nonexistent). For as much criticism and controversy that artificial intelligence generates, the harsh reality is that AI has radically altered technological and societal paradigms. If you’re not knee-deep into machine intelligence, you are inextricably falling behind — and at an exponential rate.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

But thesis risk isn’t what should concern prospective shareholders of MU stock; it’s equity risk. These categories are not the same thing. Suppose that Micron’s core catalyst — that memory shortages extend well beyond 2026 — turns out correct. Let’s also suppose that high-bandwidth memory sells out and that AI demand remains enormous.

MU stock can still disappoint investors. How? You’re looking at a situation where UBS analysts have raised their price target to an astronomical $1,625. At some point, you’re no longer asking if Micron stock will do well. That’s already baked into the valuation. Instead, you’re asking whether the security will do better than what the market already expects.

That’s a much larger hurdle. Again, it’s no longer about people believing in the broader AI narrative — everybody does. But ironically, that’s the biggest risk. You have too many people willing to pay a premium for pie-in-the-sky valuations.

Thus, there can’t just be pie in the sky. There has to be multiple, Michelin-star-quality pies, the best pies you’ve ever had in your life to justify those premiums.

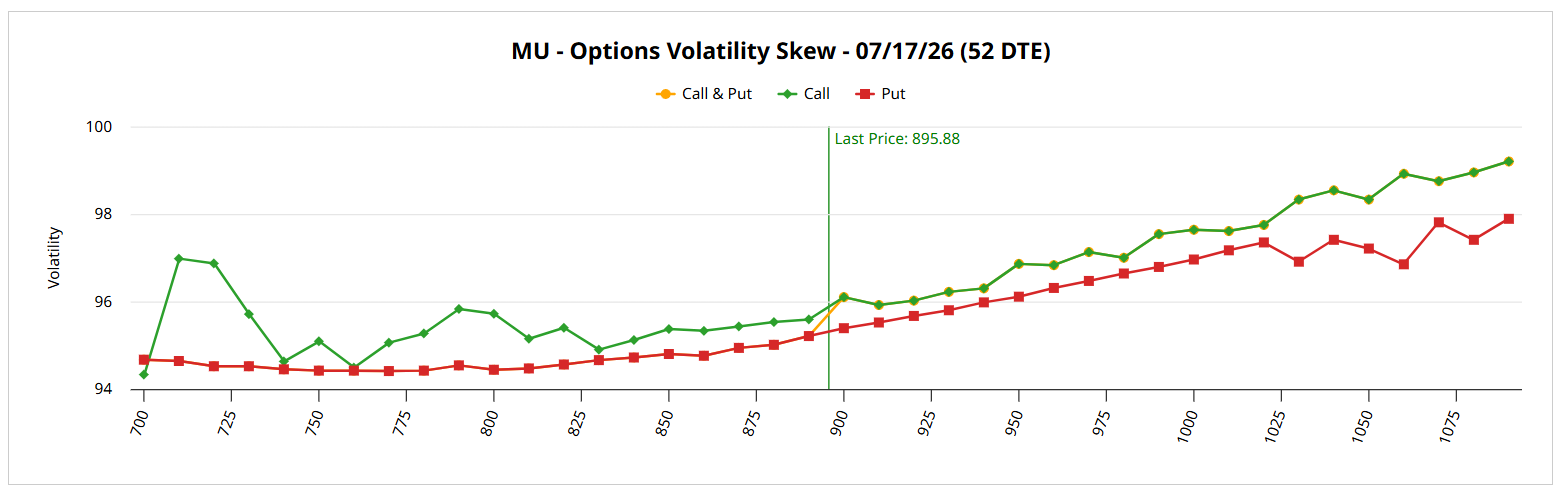

Scorching Enthusiasm for MU Stock Represents a Risky Environment

If you want empirical evidence for the above concerns related to Micron stock, look no further than the volatility skew (especially for the further out July 17 expiration date). By definition, the skew identifies implied volatility (IV) across the strike price spectrum of a given options chain. Since IV represents a security’s pricing potential at the selected strike, options traders effectively bid up coverage of the implied move.

In colloquial terms, the skew is an insurance market. On any given day, a popular security is going to march up or it’s going to fall down. Sophisticated traders must weigh the perceived probability of the potential trajectory and hedge accordingly. This hedging activity is what creates the fluctuating dynamics of the volatility skew.

Typically, the skew leans toward put dominance — that is, downside protection — on the left-side tail (south of the current spot price). For high-quality blue chips, you’ll also see call dominance on the right side, which equates to traders positioning for upside convexity. In other words, they want to protect against downside risk but lever up for any possible rallies.

In the case of MU stock, relative call dominance is the order of the day. What’s even more prominent is that, past the current spot, call dominance continues to rise for further out-the-money (OTM) calls. Basically, traders are minimizing protection against corrective moves and prioritizing upside convexity. And this ties in perfectly to the concerns that I expressed earlier.

Let me repeat: no one denies the power of the AI narrative. That’s clearly baked into the expectational sentiment of the volatility skew. The risk is whether MU stock can offer a big enough differential between actual outcomes and expected outcomes.

Right now, there’s a heavy premium for OTM calls — OTM! There’s no intrinsic value in these options, which means that there’s a lot of expectational premium embedded in MU stock. Subsequently, it’s not enough to meet expectations: there likely must be a robust, positive spread between expectation and eventual reality.

The probing question, then, is whether there is enough reward to justify the risk?

Historical Data for Micron Stock Points to a Dilemma

Looking at MU stock’s weekly price data since 1990, a random 10-week long position would be expected to generate an exceedance ratio of 52.8%. In other words, if you were to buy MU a hundred times simultaneously across parallel universes, you would expect to be profitable about 53 times. Under this random scenario, the expected forward 10-week median distribution would likely land between $892.50 and $915.

However, we’re not interested in trading Micron stock randomly. Instead, let’s consider the current quantitative setup. Over the past 10 weeks, MU printed eight up weeks, leading to an overall upward slope across the period (I’ll just abbreviate this sequence as 8-2-U).

Under this specific condition, the exceedance ratio only marginally improves to 55%. Moreover, the forward 10-week distribution expands on both tails, from $880 to $930. When you drill into these numbers, the risk-reward profile is unfavorable.

On the risk side, you’re comparing the aggregate sequence’s median downside risk of a 0.38% loss versus a 1.8% loss for the conditional sequence. This comes out to a magnitude difference of roughly 4.74x. On the reward side, you’re comparing an aggregate reward of 2.5% versus a conditional reward of 5.7%. That’s a magnitude difference of 2.28x.

Considering that the exceedance ratio only marginally improves under 8-2-U conditions relative to the random baseline, the higher magnitude risk differential clouds the lower reward differential.

Of course, that’s not to say that Micron stock can’t continue rising because it obviously can. However, you will be paying a higher premium for a narrower opportunity window. That’s the long-term math that’s unavoidable.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Micron Stock Might Have a Math Problem Why Traders Are Watching Bull Call Spreads on GOOGL Institutional Investors Love Ford Stock - Buying Huge, Unusual Volume of Long-Term Call Options How to Trade Lockheed Martin Stock Now Amid Escalating U.S.-Iran Tensions