President Donald Trump's administration’s proposed $1.5 trillion defense budget for 2027, which is more than 50% higher than current levels, has put aerospace and defense stocks back in focus as 2026 moves forward. Earlier this year, ongoing tensions from the Ukraine-Russia war and rising pressure in Asia already pushed investors toward the sector for stability and growth.

That demand shows in the numbers. The S&P Aerospace & Defense Select Industry Index ($SIAD) is up 49% over the past year, well ahead of the S&P Total Market Index ($STMI), which has gained almost 30% over the same period.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Right at the center of that trend is Northrop Grumman (NOC). The company brings in over $42 billion in annual revenue and more than $4 billion in net income, while offering a forward dividend yield of about 1.7%. More importantly, the defense firm just raised that payout. Northrop Grumman's board recently approved a new quarterly dividend of $2.47 per share, payable on June 17 to shareholders on record as of June 1, up from $2.31 per share. The dividend hike marks an increase of nearly 7%.

With higher defense spending, steady earnings, and a growing dividend, is Northrop Grumman quietly building a case for being the most compelling income stock in defense right now? Let’s take a closer look.

Northrop Grumman's Financial Strength Supports Returns

Northrop Grumman is one of the biggest defense companies in the United States, with most of its money coming from long-term government contracts across aerospace and military systems.

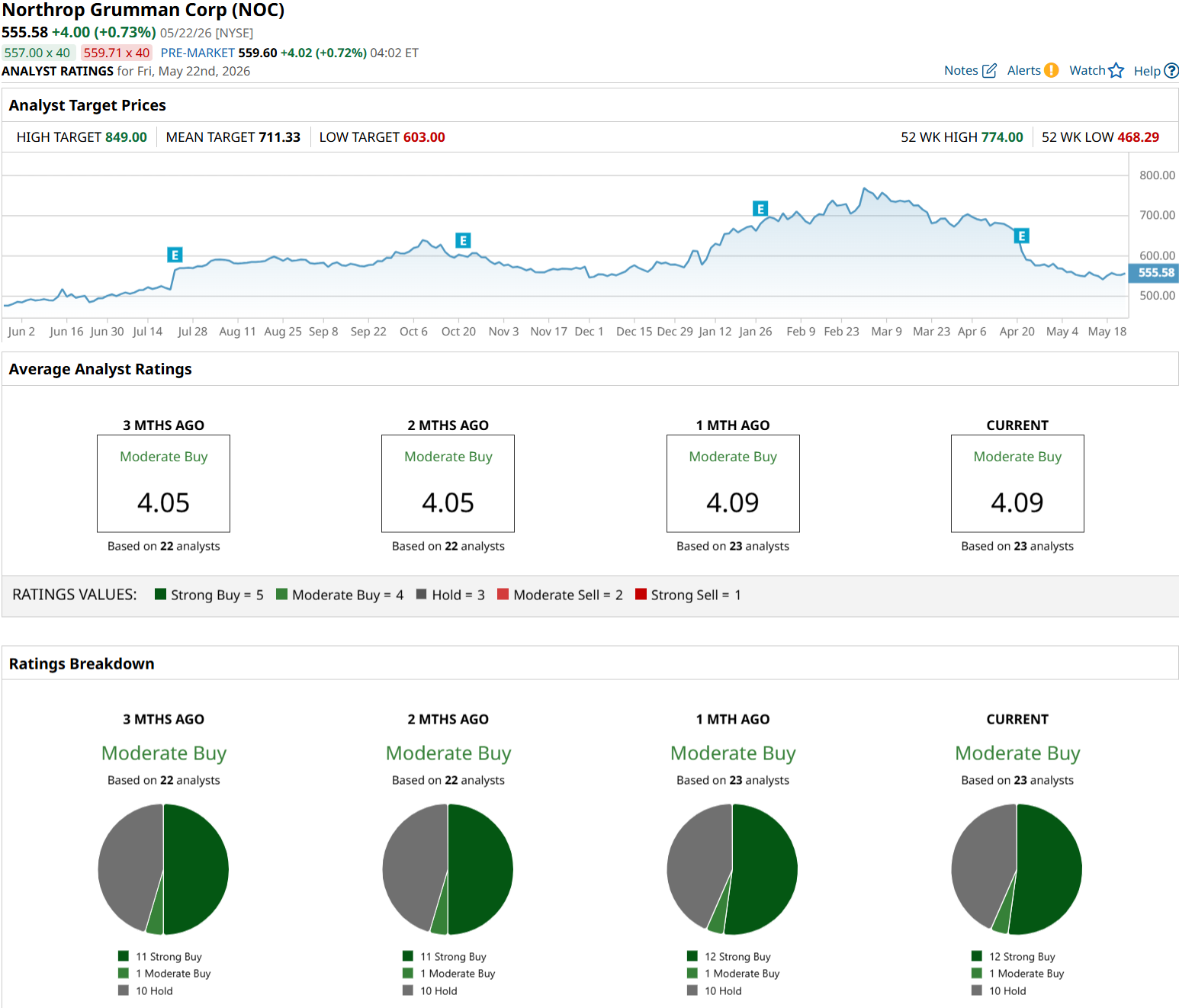

NOC stock has had a solid run in the past 52 weeks, up 18% over the past year. However, shares are down more than 2% so far this year.

www.barchart.com

www.barchart.com The valuation is also pretty reasonable. With a forward price-to-earnings (P/E) ratio of 19.8 times, Northup Grumman is in line with the sector average.

On the income front, NOC stock yields about 1.66%. That is backed by a low payout ratio of 32.65% and 23-straight years of dividend increases. The latest quarterly dividend of $2.31 shows that consistency, supported by trailing EPS of $28.15.

The latest earnings back that up. In the first quarter of 2026, revenue came in at $9.88 billion, up 4% year-over-year (YOY) or 5% on an organic basis. Net income jumped 82% to $875 million, while EPS rose 85% to $6.14, helped slightly by a 2% drop in share count. Operating income climbed 73% to $989 million, with margins improving to 10% from 6.1%. Free cash flow was still negative at -$1.82 billion, mainly due to timing and ongoing investments, but full-year guidance points to a recovery. The company expects $3.1 billion to $3.5 billion in full-year free cash flow alongside revenue of up to $44 billion and EPS near $28.

The Long-Term Drivers Powering NOC Stock

Northrop Grumman’s growth story is tied to a few major U.S. defense programs, starting with the B-21 Raider. The aircraft is already moving through flight testing and has shown it can handle aerial refueling, which means it can operate globally with more flexibility. It is also built to be more fuel-efficient than older bombers, helping reduce costs and logistics pressure. Northrop Grumman has already put more than $5 billion into the program, and production is picking up, with the first delivery expected in 2027 and room to increase output over time.

That carries over to the Sentinel program, where Northrop Grumman is working with the U.S. Air Force to replace the current ground-based nuclear system. The program is moving toward a 2027 first flight and is expected to become operational in the early 2030s. Development is being conducted in phases to speed things up, with testing and deployment happening earlier in the process. It is a large effort, supported by more than 500 suppliers and over 10,000 workers, backed by $13.5 billion in investment over the past five years, including $2 billion focused on rocket motor capabilities.

Growth is also spreading into space and munitions. Northrop Grumman is increasing production of GEM 63 rocket motors for Amazon’s (AMZN) Project Kuiper and winning new satellite contracts. It also doubled tactical rocket motor output in 2025 and plans to raise that by another 50%.

Finally, demand is rising outside of the U.S., with international sales up 20% as of Q4 2025 and more than 20 countries showing interest in Northop Grumman's defense systems.

Market Sentiment and Outlook

For the current June quarter, analysts expect EPS of $6.81, down 4% from $7.11 a year ago. That softer trend is expected to continue into the September quarter, with estimates at $7.05 compared to $7.67 last year, marking a roughly 8% drop. Look beyond the near term, however, and things start to improve. Full-year 2026 earnings are projected at $27.93, up 6% YOY from $26.34, pointing to a return to steady growth.

Analysts are adjusting their views around that setup. Citi analyst John Godyn lowered his price target to $628 on May 18 but kept a “Buy” rating, showing confidence despite the short-term pressure. Wells Fargo came in more bullish, starting coverage with an “Overweight” rating and an $800 target, tied to long-term upside from the B-21 bomber and the Sentinel program. That call stands out because it came while the stock was underperforming, suggesting a focus on the bigger picture. Finally, Jefferies also nudged its target higher to $710 while keeping a “Hold” rating, pointing to expected margin improvement.

Overall, sentiment remains positive. NOC stock has a consensus “Moderate Buy" rating based on 23 analysts with coverage. The average price target of $711.33 suggests potential upside of about 28% from current levels.

www.barchart.com

www.barchart.com Conclusion

Northrop Grumman looks like it is making a strong case as one of the more compelling income names in defense right now. The nearly 7% dividend hike adds to an already durable shareholder return profile, while solid earnings, major long-cycle programs, and broad analyst support give the story real backing beyond the payout itself. Even with some near-term earnings pressure, the bigger picture still points to steady growth as programs like the B-21 and Sentinel ramp further. From here, the most likely direction for NOC stock looks higher over time, especially if execution stays on track and defense spending remains a clear policy priority.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This High-Yield Defense Stock Just Hiked Its Dividend Nearly 7% AutoZone Stock Is Plummeting Despite Strong Earnings. Here's Why. From ‘Clusters’ to ‘Factories,’ An AI Networking Supercycle Will Lift Marvell Stock Higher American Airlines Stock Pops on New Starlink Contract