Burlington Stores, Inc. BURL reported impressive first-quarter fiscal 2026 results, wherein revenues and earnings grew year over year. Also, the top and bottom lines surpassed the Zacks Consensus Estimate. The off-price retailer benefited from broad-based comparable sales growth, merchandise margin expansion and continued supply-chain productivity improvements, enabling the company to post its 14th consecutive quarter of double-digit earnings growth.

Management highlighted strong execution across merchandising, inventory management and store operations, with particular strength in ladies apparel, beauty and accessories. Burlington Stores also benefited from improved allocation and localization capabilities, which helped the company capitalize on warm-weather demand trends during the quarter.

Despite the strong performance and an increase in the fiscal 2026 guidance, investors reacted negatively to the results, sending shares down 7.9% following the announcement. The decline likely reflected elevated investor expectations heading into the release, as well as caution surrounding the company's modest fiscal second-quarter comparable sales guidance and broader consumer spending uncertainties.

Burlington Stores, Inc. Price, Consensus and EPS Surprise

Burlington Stores, Inc. price-consensus-eps-surprise-chart | Burlington Stores, Inc. Quote

More on Burlington Stores’ Q1 Financial Results

Burlington Stores reported adjusted earnings of $2.01 per share, comfortably beating the Zacks Consensus Estimate of $1.77. Adjusted EPS increased 25.6% from $1.60 in the year-ago quarter.

Total revenues increased 14.1% year over year to $2.86 billion and exceeded the Zacks Consensus Estimate of $2.81 billion. Net sales rose 14% to $2.85 billion from $2.50 billion in the prior-year period.

Comparable store sales increased 6%, significantly ahead of management’s guidance of 2-4%. According to management, comps growth was broad-based across merchandise categories and geographic regions, reflecting healthy consumer demand and effective execution of Burlington Stores’ off-price model. Our model anticipated a 3.5% year-over year rise in comparable store sales for the fiscal first quarter.

Insight Into BURL’s Margins

The gross margin expanded 30 basis points year over year to 44.1% in the first quarter of fiscal 2026. This also surpassed our estimate for gross margin of 43.5%. The improvement was driven by a 20-basis-point increase in the merchandise margin and a 10-basis-point reduction in freight expenses as a percentage of net sales.

Adjusted selling, general and administrative (SG&A) expenses increased 15.2% year over year to $771.3 million from $669.5 million in the first quarter of fiscal 2025. Adjusted SG&A, excluding expenses related to bankruptcy-acquired leases, represented 26.8% of net sales, up 20 basis points year over year. Notably, adjusted SG&A surpassed our estimate of 26.3% of net sales.

Product sourcing costs increased to $216 million from $197 million in the first quarter of fiscal 2025. However, as a percentage of sales, product sourcing costs declined by 30 basis points year over year, reflecting continued progress on supply-chain productivity initiatives and cost-saving programs across the distribution network. Such costs comprise the processing goods costs via the supply chain and buying expenses.

Adjusted EBIT increased to $179 million from $152 million in the first quarter of fiscal 2025. The adjusted EBIT margin expanded 20 basis points year over year to 6.3%, significantly exceeding management's original expectation for a margin decline of 60-100 basis points. According to management, the margin outperformance was primarily driven by higher merchandise margins, stronger sales leverage and continued supply-chain productivity gains.

Adjusted EBITDA increased to $284 million from $244 million in the prior-year quarter. The adjusted EBITDA margin also improved 20 basis points year over year.

BURL’s Financial Snapshot: Cash, Debt & Equity

Burlington Stores ended the first quarter of fiscal 2026 with total liquidity of $1.69 billion, consisting of $747 million in unrestricted cash and $942 million of availability under its asset-based lending (“ABL”) facility.

Total outstanding debt at the quarter-end was $1.92 billion, including $1.72 billion under the Term Loan facility, $186 million in convertible notes and no borrowings under the ABL facility.

Burlington Stores repurchased $111 million of its outstanding 1.25% convertible notes in the fiscal first quarter. The transaction, valued at $173 million, was settled through a combination of $129 million in cash and the issuance of 150,831 shares of common stock.

The company also repurchased 257,906 shares of its common stock for approximately $81 million under its share repurchase program. At the end of the fiscal first quarter, $304 million remained available under the current share repurchase authorization.

BURL’s Store Update

In the first quarter of fiscal 2026, Burlington Stores opened 40 stores, relocated six and closed four stores, resulting in a net increase of 30 stores during the period. The company ended the quarter with 1,242 stores across 47 states, Washington DC and Puerto Rico.

BURL’s Q2 Guidance

For the second quarter of fiscal 2026, Burlington Stores expects total sales to increase 10-12%, including comparable store sales growth of 1-3%. The company expects the adjusted EBIT margin to increase 30-60 basis points year over year, excluding $3 million of anticipated expenses associated with bankruptcy-acquired leases in the second quarter of fiscal 2026, whereas it registered $11 million in the prior-year period.

Management expects the margin improvement to be driven by higher merchandise margins, supported by markdown favorability, modestly faster inventory turns and a favorable shortage accrual rate versus last year. These benefits are expected to be partially offset by modest freight expense pressure related to higher fuel rates.

Burlington Stores also expects leverage in product sourcing costs as it continues to realize benefits from supply-chain productivity initiatives across its distribution center network. However, these savings will be partially offset by ongoing start-up costs related to the company's new distribution center in Savannah, GA, which became operational late in the fiscal first quarter. Management also expects SG&A expenses to provide modest leverage during the quarter.

The company anticipates an adjusted effective tax rate of 23% and adjusted earnings per share of $2.05-$2.20, whereas it reported an adjusted EPS of $1.72 in the second quarter of fiscal 2025. Management noted that sales trends in May were tracking at the high end of its comparable sales guidance range, although monthly comparisons are expected to become more challenging as the quarter progresses.

FY26 View for BURL

For fiscal 2026, Burlington Stores expects total sales to increase 9-11%, following a 9% increase in fiscal 2025. This compares with the prior guidance of 8-10%. The outlook assumes comparable store sales growth of 2-4%, on top of a 2% comparable sales increase in fiscal 2025. Previous estimation of comparable store sales growth was 1-3%.

The company expects to open 115 net new stores during the year, up from the prior mentioned 110 net new stores, with the majority of store openings anticipated to occur in the first half of the year.

Burlington Stores expects the adjusted EBIT margin to increase 10-30 basis points from that reported in fiscal 2025, excluding $10 million of anticipated expenses associated with bankruptcy-acquired leases in fiscal 2026 versus the $35 million registered in fiscal 2025.

Adjusted earnings per share are projected to be $11.45-$11.80, whereas it reported an adjusted EPS of $10.17 in fiscal 2025. The updated outlook implies year-over-year earnings growth of 13-16%. Previously, the adjusted EPS was projected between $10.95 and $11.45. The outlook assumes a share count of 64 million. Capital expenditure, net of landlord allowances, is expected to be $875 million.

Management noted that its outlook for the back half of fiscal 2026 remains unchanged. For the second half of the year, the company expects comparable store sales growth of 1-3%, total sales growth of 8-10%, the adjusted EBIT margin expansion of 10-30 basis points and earnings per share of $7.30-$7.50. Management also expects comparable sales upside in the fiscal third quarter and possibly the fourth quarter as Burlington Stores laps easier comparisons and prior-year tariff-related assortment gaps.

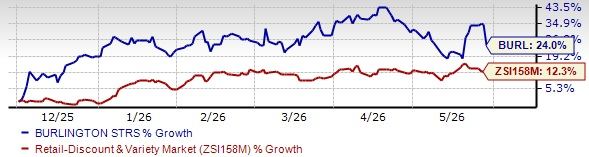

BURL Stock Past 6-Month Performance

Image Source: Zacks Investment Research

In the past six months, this Zacks Rank #3 (Hold) company has gained 24% compared with the industry’s 12.3% growth.

Key Picks

We have highlighted three better-ranked stocks, namely, Ross Stores Inc. ROST, Victoria's Secret & Co. VSCO and Levi Strauss & Co. LEVI.

Ross Stores operates as an off-price retailer of apparel and home accessories, primarily in the United States. It carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Ross Stores’ current fiscal-year earnings and sales indicates growth of 15.6% and 8.2%, respectively, from the year-ago actuals. ROST delivered a trailing four-quarter average earnings surprise of 10.2%.

Victoria's Secret is a specialty retailer of women's intimates, sleepwear, apparel, sport and swimwear, and prestige fragrances and body care. It currently has a Zacks Rank of 2. The company delivered a trailing four-quarter earnings surprise of 55.1%, on average.

The Zacks Consensus Estimate for VSCO’s current fiscal-year sales and earnings indicates growth of 6.2% and 16.3%, respectively, from the year-ago reported numbers.

Levi Strauss designs and markets jeans, casual wear and related accessories for men, women and children. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for Levi Strauss’ current fiscal-year earnings and sales suggests growth of 11.9% and 5.2%, respectively, from the year-ago actuals. LEVI delivered a trailing four-quarter average earnings surprise of 21.4%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

Burlington Stores, Inc. (BURL): Free Stock Analysis Report

Levi Strauss & Co. (LEVI): Free Stock Analysis Report

Victoria's Secret & Co. (VSCO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).