After a blowout first-quarter fiscal 2027 earnings report, telecommunications contractor Dycom Industries (DY) saw its stock surge 25.84% intraday on May 27, leading a rally in data center infrastructure stocks.

Dycom has emerged as a beneficiary as the U.S. undergoes a multi-year expansion of its digital infrastructure, with telecom carriers expanding their fiber networks and cloud and AI companies competing to construct and connect new data centers that demand enormous cabling, power, and networking infrastructure.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In other words, big names announcing hyperscaler-focused network buildouts position Dycom for long-term growth through large-fiber projects and work inside data centers. On top of that, the company has the potential to emerge as the beneficiary of the BEAD program.

About Dycom Industries Stock

Dycom Industries is a leading specialty contracting firm that provides infrastructure services to the telecommunications and utility sectors. Based in West Palm Beach, Florida, the company offers a broad range of services, including program management, engineering and design, aerial and underground construction, wireless network deployment for 4G and 5G, maintenance, and fulfillment.

It also provides electrical contracting for data centers and underground facility locating for utilities, supplying the skilled workforce, tools, and equipment essential for building and maintaining America's critical digital and utility infrastructure. The company has a market capitalization of $16.07 billion.

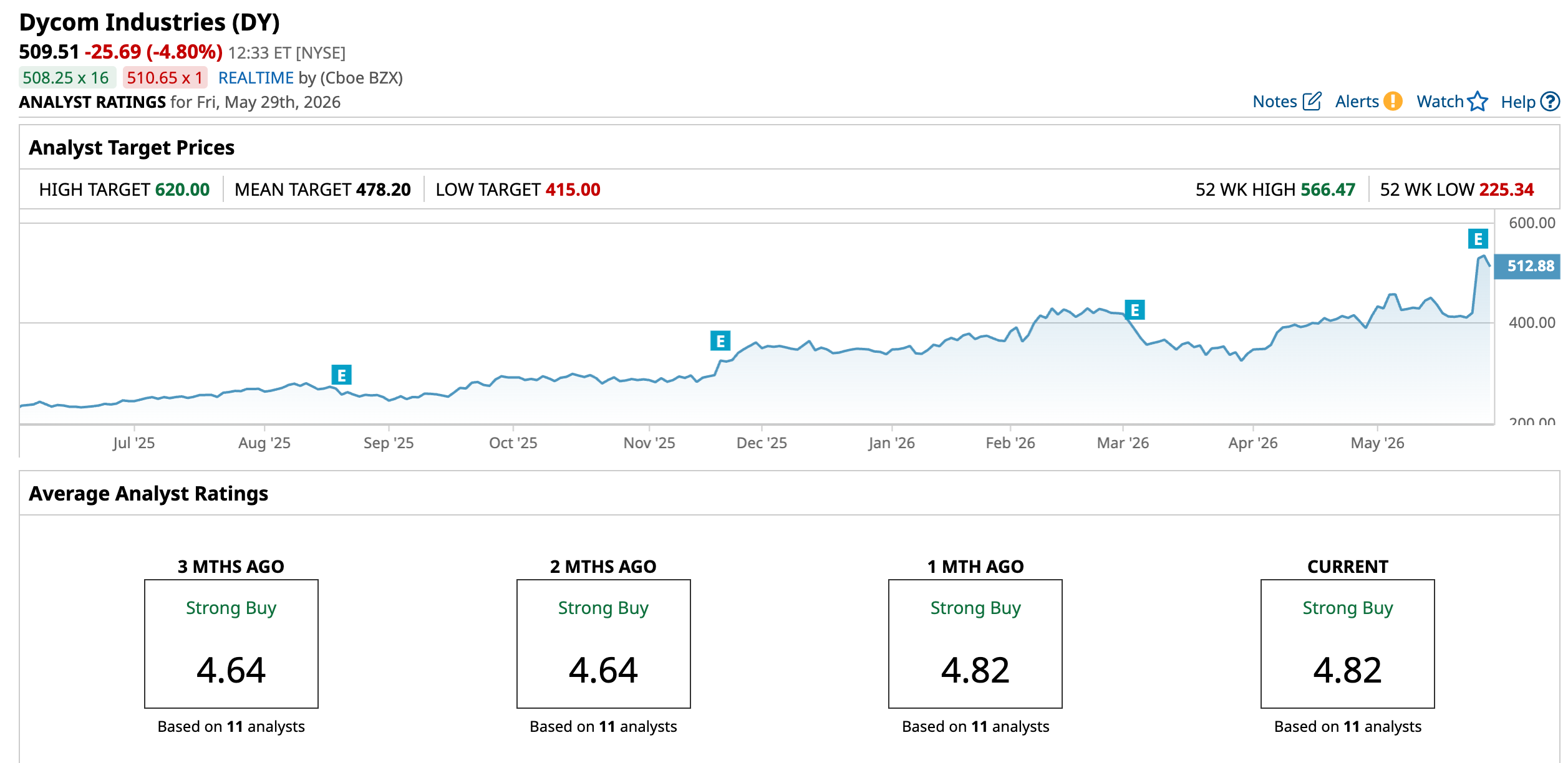

Surging demand for telecom and digital infrastructure services, including a growing demand for fiber and electrical contracting to support AI-powered data centers, has led to a robust upswing in Dycom’s stock. Over the past 52 weeks, the stock has gained 124.38%, and it is up 50.9% year-to-date (YTD). It reached a 52-week high of $566.47 on May 27, but is down 6.6% from that level.

www.barchart.com

www.barchart.com On a forward-adjusted basis, Dycom’s price-to-earnings (non-GAAP) ratio of 33.20 times is higher than the industry average of 20.06 times.

Dycom Industries' Q1 Earnings and Revenue Surge on Record Backlog and Strong Infrastructure Demand

Based on solid demand for fiber infrastructure and data center builds, Dycom reported robust first-quarter results for fiscal 2027 (quarter ended May 2). The company’s contract revenue increased 56.1% year-over-year (YOY) to $1.96 billion, which is higher than the $1.66 billion that Wall Street analysts had expected. Contract revenues grew organically by 24.7%.

Dycom is expanding its capabilities, both organically and through acquisitions. In May, the company entered into a definitive agreement to acquire National Technology Integrators, a tenured and fast-growing low-voltage engineering and construction firm, for $275 million. The plant specializes in inside-plant structured cabling, including within data centers.

Dycom’s non-GAAP adjusted EPS grew 84.9% YOY to $4.42, surpassing the $2.73 figure that Street analysts had expected. Notably, the company’s backlog reached a quarterly record of $11.91 billion, up 46.5% YOY. It raised its fiscal 2027 contract revenue outlook to a range of $7.38 billion to $7.65 billion.

Wall Street analysts are robustly optimistic about Dycom’s future earnings. For the current fiscal year, EPS is projected to surge 7.7% annually to $12.89, followed by a 19.3% growth to $15.38 in the next fiscal year. Moreover, analysts expect the company’s EPS to grow by 12.6% YOY to $3.75 for the second quarter of fiscal 2027.

What Do Analysts Think about Dycom Industries Stock?

In March, analysts at Cantor Fitzgerald initiated coverage on Dycom’s stock with a bullish “Overweight” rating and a $436 price target. The firm cited potential benefit from multi-year U.S. digital infrastructure investments across fiber-to-the-home, long-haul and middle-mile fiber, wireless initiatives, and hyperscaler-related work, with Dycom’s acquisition of Power Solutions adding a second growth driver.

JP Morgan analyst Richard Choe reaffirmed his “Overweight” rating on Dycom while raising the price target from $395 to $415, reflecting confidence in the company’s market position and growth potential. Analysts at B.Riley also raised the price target from $420 to $485, while keeping a “Buy” rating, citing the company’s strong margin expansion during this cyclical growth period despite serving a concentrated telecom market.

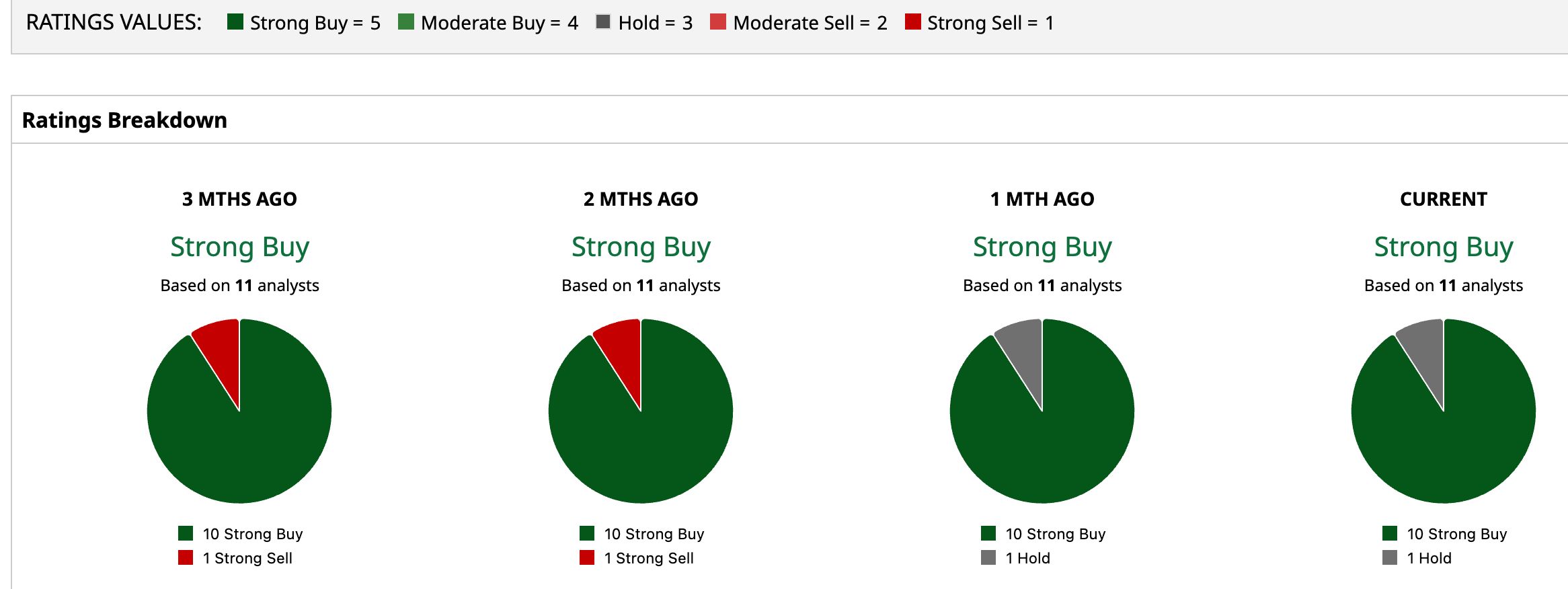

Dycom Industries has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 11 analysts rating the stock, a majority of 10 analysts have given it a “Strong Buy” rating, while only one analyst is taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $478.20 represents a 6.15% downside from current levels. However, the Street-high price target of $620 indicates an 21.7% upside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Snowflake Stock Rallies on Blockbuster Q1 Results. It Turns Out That Gen AI Isn’t Eating Its Lunch. Dycom Industries Stock Just Skyrocketed. It's the Latest Winner from Data Center Demand. The 180-Day Lease Holding Up SpaceX's $2 Trillion IPO