A year ago, few investors mentioned Dell Technologies (DELL) in the same breath as artificial intelligence (AI) heavyweights. Today, the company sits right in the spotlight, drawing significant attention alongside NVIDIA Corporation (NVDA) and Alphabet (GOOG) (GOOGL). A surge in demand for the hardware powering AI workloads has turned Dell into one of the market’s biggest talking points.

So much so that DELL stock reached a fresh 52 week high of $429.15 on May 29, just a day after the company unveiled a blockbuster Q1 FY2027 earnings report. Dell’s numbers left Wall Street scrambling to update its models. The company sailed past expectations, raised its full year outlook, then reinforced its position as one of the clearest winners from the AI spending wave.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Strong demand throughout the quarter paired with rapid innovation across personal computers, compute platforms, and storage solutions pushed results to record levels. The company secured $24.4 billion in AI orders, recognized $16.1 billion in AI server revenue, then lifted its FY2027 AI server revenue target to a staggering $60 billion, up 144% year-over-year (YOY). The figure alone suggests the AI boom still has plenty of fuel in the tank.

The quarter proved so strong that even seasoned analysts found themselves caught off guard. Morgan Stanley analyst Erik Woodring openly admitted that his team misread the setup and placed its price target under review. He described the performance as one of the most impressive quarters witnessed during his coverage of the hardware sector.

Such praise rarely comes cheap on Wall Street, which makes Dell’s latest achievement all the more noteworthy. With momentum building at full speed, investors now have plenty of reasons to take a closer look at the stock.

About Dell Stock

Headquartered in Round Rock, Texas, Dell Technologies is a global technology company that develops and sells computers, servers, data storage systems, networking products, software, and information technology (IT) services.

The nearly $271.8 billion market cap company helps organizations modernize technology infrastructure, manage data, strengthen digital operations, support AI workloads, and access flexible financing, subscription, leasing, and technology consumption solutions across global markets.

Dell’s shareholders have enjoyed a remarkable ride. Its stock has soared 316.85% over the past 52 weeks and gained 268.47% year-to-date (YTD). The rally gathered even more steam during the last three months, delivering a return of 213.23%. Moreover, investors pocketed another 57.13% gain during the past five trading sessions alone following the company’s latest earnings release.

www.barchart.com

www.barchart.com On the valuation front, DELL stock currently trades at 25.96 times forward adjusted earnings and 1.60 times sales. The figures remain below the broader industry average, although they stand above their own five-year historical multiples.

Dell also rewards shareholders with an annual dividend of $2.52 per share, which translates into a dividend yield of 0.60%. The company paid its most recent quarterly dividend of $0.63 per share on May 1 to shareholders of record as of April 21.

Dell Surpasses Q1 Earnings

Dell’s Q1 FY2027 results, reported on May 28, landed with the force of a thunderclap. Revenue jumped 87.5% YOY to $43.8 billion and comfortably cleared analyst expectations of $36.1 billion. Adjusted EPS climbed 213.5% to $4.86 from the year ago level and raced past Street’s estimates of $2.96.

The company’s Client Solutions Group, which includes desktop personal computers, laptops, monitors, and related equipment sold to both consumers and commercial customers, generated revenue of $14.6 billion. The result represented growth of 16.8% from the previous year.

The real fireworks came from the Infrastructure Solutions Group. Revenue within Dell’s data center focused operations surged 181.2% to $29 billion. AI optimized server sales exploded 757.2% higher and reached $16.1 billion, providing the engine behind the division’s eye-popping performance.

The strength flowed directly to the bottom line. Adjusted operating income climbed 154.2% from the prior year to $4.2 billion. Meanwhile, adjusted net income vaulted 193.7% to $3.2 billion. Adjusted free cash flow also advanced 41.8% and reached $3.2 billion.

Looking ahead, management expects Q2 FY2027 revenue between $44 billion and $45 billion. The midpoint of $44.5 billion implies YOY growth of 49%. Management also expects Q2 adjusted diluted EPS of $4.80 at the midpoint, representing growth of 107%.

They have raised its full year FY2027 outlook as well. Revenue now stands projected between $165 billion and $169 billion. The midpoint of $167 billion represents growth of 47% from the previous year, whereas full year non-GAAP diluted EPS is projected at $17.90 at the midpoint, reflecting growth of 74%.

Wall Street remains somewhat more conservative. Analysts currently forecast Q2 FY2027 EPS of $2.94, marking a growth of 40% YOY. For full FY2027, analysts expect the bottom line to increase 32% to $12.21. FY2028 projections call for another 12.2% increase to $13.70.

What Do Analysts Expect for Dell Stock?

Argus analyst Jim Kelleher has raised his price target on Dell to $460 from $200 while maintaining a “Buy” rating. He pointed to substantial beats on both revenue and earnings along with a dramatic increase in FY2027 guidance.

Raymond James analyst Simon Leopold took an even bolder stance. He raised his price target to $500 from $182 and maintained an “Outperform” rating on the stock. Strong pricing, accelerated personal computer orders, robust demand for AI platforms, stronger server growth forecasts, relatively stable storage expectations, and disciplined execution all contributed to his more optimistic outlook.

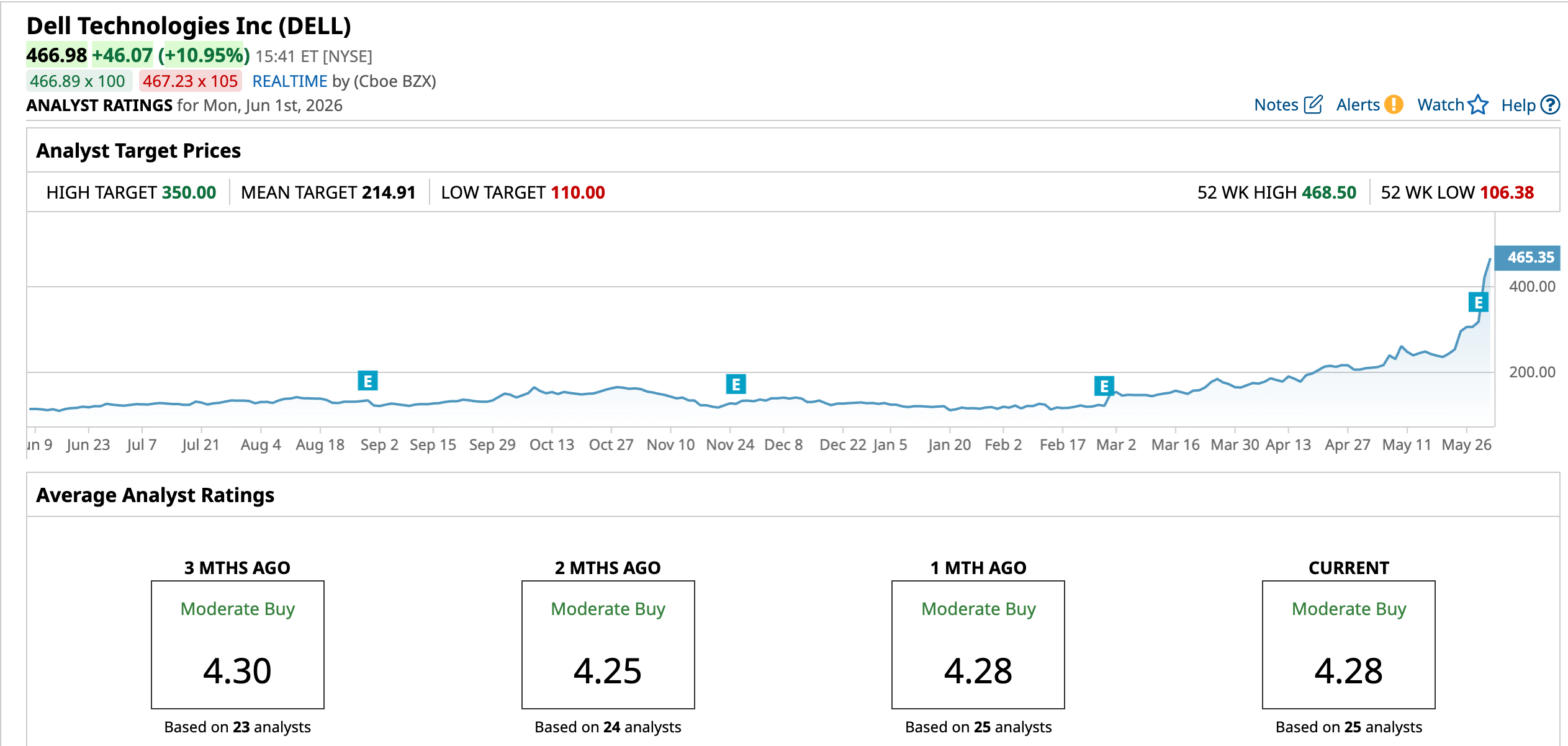

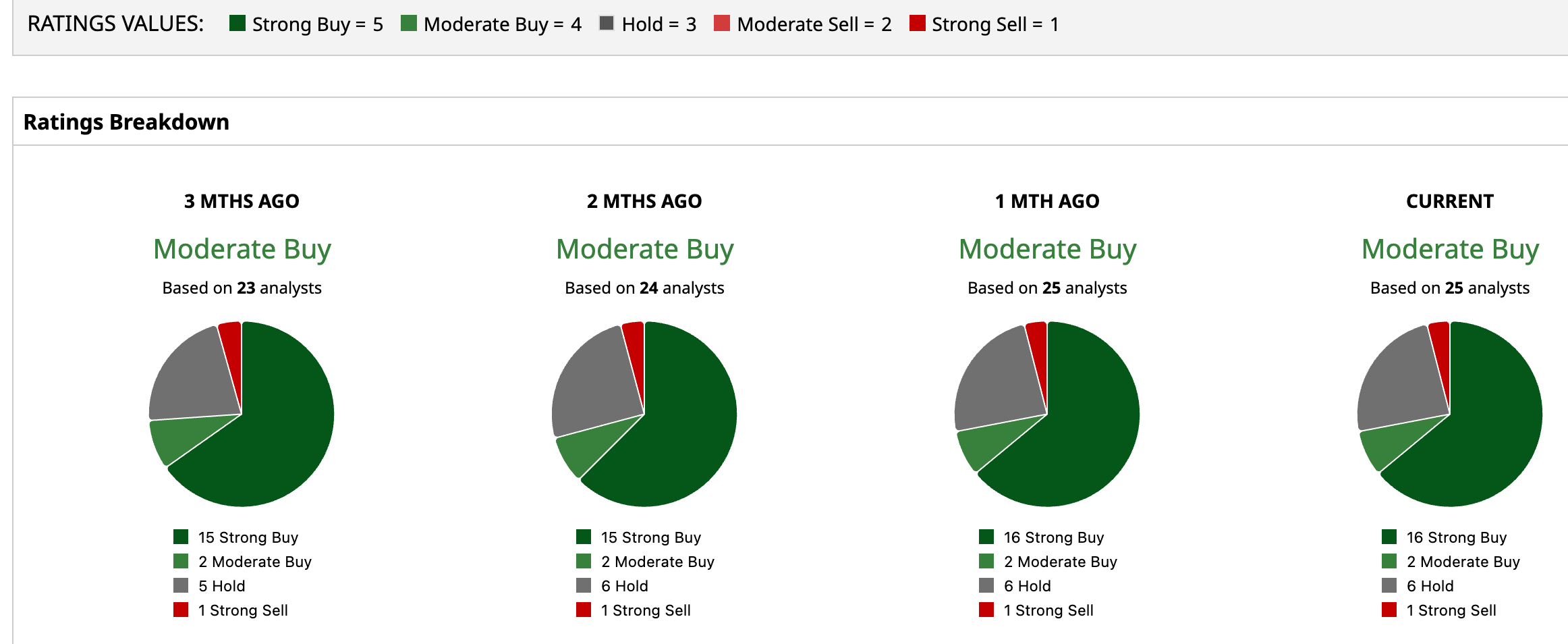

Wall Street has currently assigned DELL stock an overall “Moderate Buy” rating. Among 25 analysts covering the company, 16 recommend “Strong Buy,” two recommend “Moderate Buy,” six suggest “Hold,” and one maintains a “Strong Sell” rating.

Even after its spectacular run, Dell continues to outrun analyst expectations. Its shares already trade above the average analyst price target of $214.91 and above the Street-High target of $350.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $60 Billion Reason to Buy Dell Stock Now Why Warren Buffett Hasn’t Sold Coca-Cola Stock for Over 30 Years Nvidia Stock Has Been Muted After Excellent Earnings. Investors Are Ready for the Next Big Thing. Visa vs. Mastercard Stock: Using Barchart Data to Pick the Best Payments Giant Now