Kohl’s Corporation KSS used its first-quarter fiscal 2026 call to argue that operational fixes are starting to show up in the numbers. Management pointed to the best comparable sales performance in more than four years and a more stable core card customer.

The call mattered less for the headline loss and more for what executives said about assortment, value, inventory and digital execution as they try to rebuild consistency

Kohl’s Sees Early Benefits From Reset

Chief executive officer Michael Bender said the quarter showed progressive improvement after a year spent resetting the business. Comparable sales fell 1.1%, but he framed that as a meaningful step forward given the backdrop and the company’s recent trend.

Bender said Kohl’s card customers stabilized to a flat comp, a sharp improvement from the mid-single-digit decline in the fourth quarter. He also highlighted a 6% comparable-sales increase in proprietary brands as evidence that opening price points and product quality are resonating.

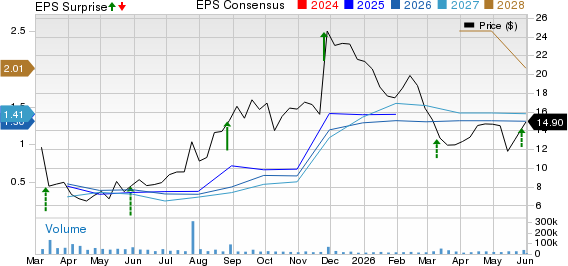

The financial release supported that steadier tone. Net sales declined 1.7% to $3.17 billion, while the loss per share was $0.13, matching the prior year. That result was better than the Zacks Consensus Estimate for a loss of $0.18, producing a 27.78% surprise, while revenue came in just above the $3.16 billion consensus.

Kohl's Corporation Price, Consensus and EPS Surprise

Kohl's Corporation price-consensus-eps-surprise-chart | Kohl's Corporation Quote

KSS Leans Harder Into Value and Private Brand

Bender returned repeatedly to value as Kohl’s central message for a pressured low- to middle-income customer. He said the company is expanding coupon eligibility, increasing proprietary-brand inventory and using marketing to reinforce its By Kohl’s labels.

Management tied some of the strongest category commentary to that strategy. Women’s, kids, accessories and home were flat to slightly positive, while juniors rose 10%, helped by the SO brand. Executives also cited strength in LC Lauren Conrad, Sonoma and Flex.

Chief financial officer Jill Timm said private brands are serving both loyal and newer shoppers because they fill a gap at more affordable opening price points. In Q&A, she said those brands are now being used more deliberately to restore relevance with Kohl’s charge customers and improve traffic.

Kohl’s Says Inventory Work is Paying Off

Inventory discipline was one of the clearest areas of management confidence. Timm said inventory fell 8% from a year ago, yet receipts rose 1%, which she described as evidence of cleaner and fresher goods rather than a pullback in investment.

She said apparel depth is being planned in the high single digits, while choice counts are planned down by a similar amount. That shift is meant to improve what management called trip assurance or the ability for customers to find the right item, size and color in stock.

Bender said spring seasonal sales rose in the mid-teens after the company corrected earlier planning and allocation mistakes. Timm added that cleaner inventory is giving Kohl’s room to chase demand and preserve regular-price selling, even as it invests part of that flexibility back into sharper value.

KSS Points to Digital Momentum and Store Gaps

Timm said stores underperformed in the quarter, declining in the low single digits as transactions weakened. Digital sales, by contrast, grew 4%, helped by higher traffic and continued expansion of the marketplace business.

Management argued that digital improvements are becoming more tangible. Bender highlighted a newly launched AI-powered gift finder through Google Gemini, while executives also pointed to better navigation, curated online experiences, clearer delivery information and easier returns.

That digital momentum is not without a tradeoff. Timm said stronger e-commerce penetration is pressuring margins through higher shipping costs, which largely offset the gross-margin benefit from proprietary brands in the quarter. Gross margin still improved by 4 basis points to 39.9%.

Kohl’s Reaffirms Outlook but Flags Consumer Pressure

Kohl’s reaffirmed its fiscal 2026 outlook for comparable sales ranging from down 2% to flat, adjusted operating margin of 2.8% to 3.4% and adjusted earnings per share of $1.00 to $1.60.

Timm said the company was pleased with both the first quarter and the start of the second quarter, but she stressed that guidance still reflects a cautious view of discretionary spending. She said the core consumer remains financially pressured and selective.

She also noted that guidance excludes any benefit from potential tariff refunds. Kohl’s submitted $140 million of claims in the first quarter and said total eligible refunds are $190 million, but none were received during the period.

KSS Q&A Focused on What Must Improve Next

Analyst questions centered on durability, margins, stores, Sephora and capital allocation. In response to Baird, management sounded more explicit that private brands, spring execution and earlier seasonal transitions are driving the recent improvement.

Questions from TD Cowen pushed on store traffic and Sephora. Executives said men’s and footwear should improve as assortment changes and back-to-school newness arrives, while Sephora is expected to track closer to company performance as MAC rolls out chainwide and skincare adds new brands.

The balance-sheet discussion also drew attention. Timm said Kohl’s ended the quarter with $429 million in cash and no borrowings on its asset-based lending facility, repurchased $50 million of debt at a discount and still sees free cash flow of roughly $500 million to $600 million this year.

What the Zacks Signals Indicate

KSS carries a Zacks Rank #3 (Hold), along with a Value Score of A, a Growth Score of B, a Momentum Score of C and a VGM Score of A. In Zacks terms, the Value and VGM grades point to relatively stronger value and combined style characteristics, while the Hold rank signals more balanced near-term expectations. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That mix does not point to a decisive directional call on its own. A Zacks Rank #3 can still be held, and the stronger style grades improve the stock’s profile within that rank, but estimate revisions remain the key driver in the system and the rank can change after analysts fully digest the quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Kohl's Corporation (KSS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).