Bank of America’s BAC deposit franchise remains a key competitive advantage and earnings driver. The bank holds $1.3 trillion in consumer deposits across its Consumer Banking and Wealth Management businesses, and average deposits worth more than $2 trillion, which makes it one of the largest deposit-gathering institutions in the United States. This vast deposit base provides a stable, diversified and low-cost source of funding that supports lending growth and balance-sheet strength.

A major benefit of the franchise is its large pool of low-cost deposits. In 2025, Bank of America maintained $515 billion in non-interest-bearing deposits, accounting for 26% of average deposits. This helps keep funding costs below those of many peers and supports net interest income (NII) growth. As interest rates stabilize/decline, deposit costs are likely to fall faster than asset yields, creating additional tailwinds for net interest margin (NIM) expansion and profitability.

The bank is already benefiting from the rate cuts last year. In first-quarter 2026, NII on a fully taxable-equivalent basis rose 9% year over year to $15.9 billion, while NIM expanded 8 basis points to 2.07%, aided by growth in earning assets funded largely through deposits. Management expects NII (FTE) to grow 6-8% year over year in 2026.

Bank of America’s sizable deposit base also provides ample liquidity and lending capacity. In 2025, the company funded an average loan portfolio of $1.14 trillion while maintaining a conservative loan-to-deposit profile. This allows the bank to expand loans and deepen customer relationships without relying heavily on more expensive wholesale funding markets.

With its scale, stability and low funding costs, Bank of America’s deposit franchise is well positioned to continue to support earnings growth, margin expansion and shareholder returns across interest-rate and economic cycles.

BAC’s Competitive Position

If we compare Bank of America's deposit franchise with two of its close peers, JPMorgan JPM and Wells Fargo WFC, it appears that BAC sits between the two firms in scale. BAC trails JPMorgan but significantly exceeds Wells Fargo.

JPMorgan possesses the largest deposit franchise in the United States. The bank ended first-quarter 2026 with $2.5 trillion in deposits, supported by a broad consumer, commercial and wealth-management customer base. Like Bank of America, JPM benefits from a substantial level of operational and consumer deposits, which helps keep funding costs relatively low and supports industry-leading NII.

Despite years of regulatory challenges, Wells Fargo's deposit franchise also remains one of its core strengths. The bank held $1.3-$1.4 trillion in average deposits in recent quarters. Its deposits are heavily weighted toward consumer checking and savings accounts, which historically have been a relatively low-cost funding source. WFC’s extensive branch footprint and strong presence in retail and small-business banking continue to underpin deposit stability.

Bank of America’s Price Performance, Valuation & Estimates

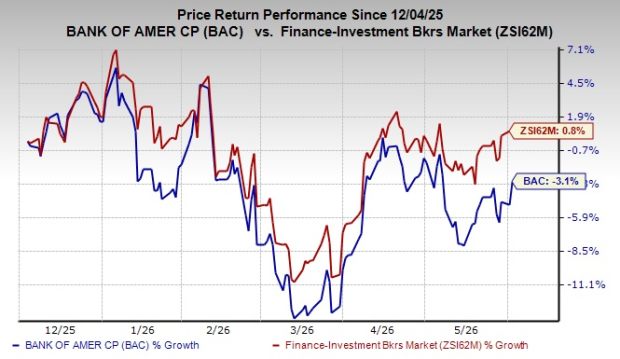

In the past six months, BAC shares have lost 3.1% against the industry’s 0.8% growth.

Image Source: Zacks Investment Research

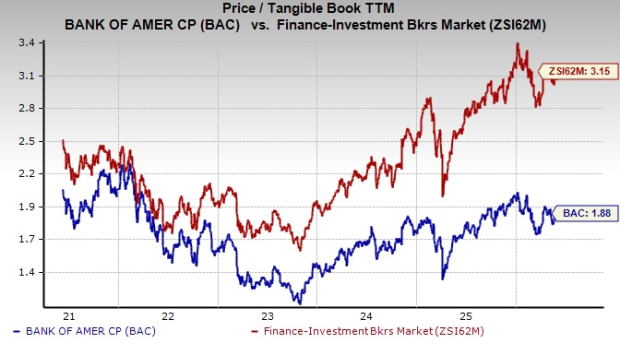

From a valuation standpoint, Bank of America trades at a 12-month trailing price-to-tangible book (P/TB) of 1.88X, below the industry average of 3.15.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for BAC’s 2026 and 2027 earnings implies year-over-year growth of 16.8% and 14.2%, respectively. In the past week, earnings estimates for both years have been unchanged.

Image Source: Zacks Investment Research

Bank of America currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

Wells Fargo & Company (WFC): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).