Hewlett Packard Enterprise (HPE) has turned into one of the market’s louder AI comeback stories. The latest move came after a strong fiscal second-quarter report for the period ended April 30, 2026, when demand for AI-ready servers and networking gear helped HPE top expectations and lift its outlook. That matters because the AI trade is now rewarding companies that can ship real equipment and turn spending into revenue, not just talk about future demand.

HPE is not a startup story. It is an established enterprise tech company that sells servers, storage, networking gear, and hybrid cloud tools to businesses and governments. That puts it right in the middle of the data center buildout that is supporting the next phase of AI growth.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The Stock Has Already Run Far

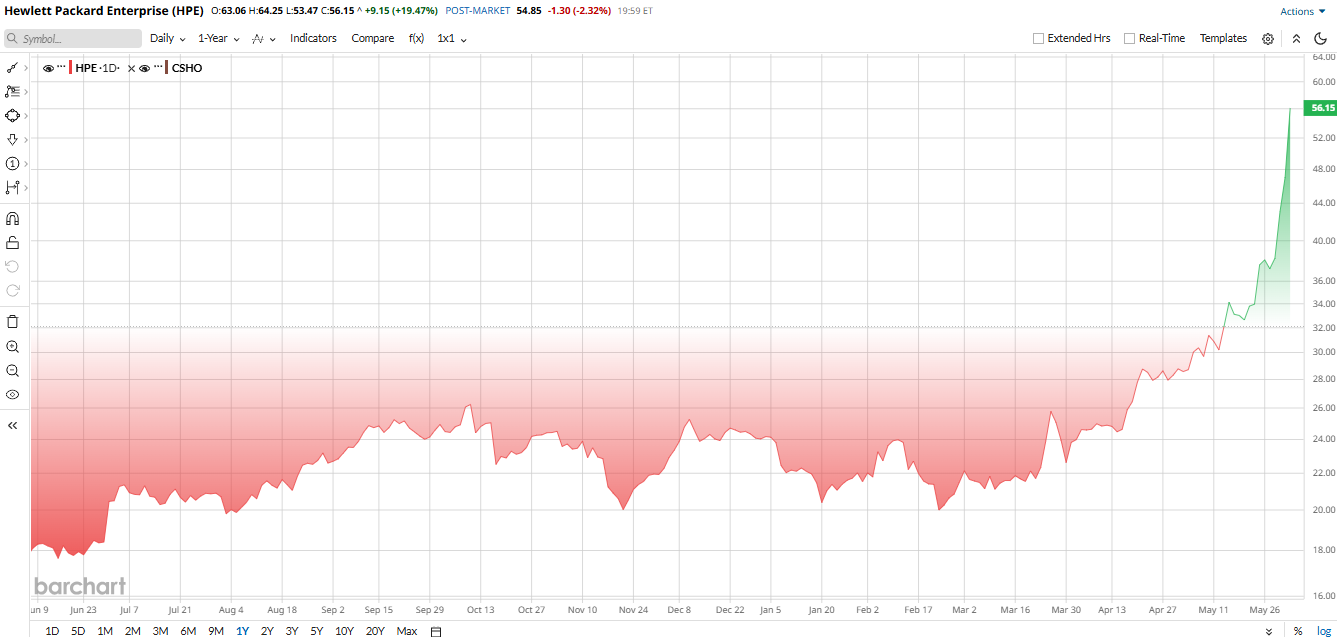

HPE has been one of the year’s strongest large-cap tech names. the stock jumped 19.5% on Tuesday right after earnings, while also noting that it has more than doubled in 2026 and gained about 211% over the past year. The rally has been helped by stronger AI demand, better execution, and the Juniper Networks deal.

Technically, the chart also looks constructive. The shares have stayed well above the 50-day and 200-day moving averages, which usually signals strong momentum. That kind of setup does not guarantee more upside, but it does show investors are still willing to pay for the growth story.

HPE is no longer cheap in the old value-stock sense, but it also does not look extreme for a business with this kind of growth. HPE forward price-to-earnings ratio at 15.66x, below Dell’s 23.92x and only slightly above Supermicro’s 14.49x. That places HPE in a middle zone, where the market is rewarding growth without fully pricing in perfection.

The bigger valuation clue came from Wall Street’s reaction. The HPE median price target jumped to $66 from $26.50 after the earnings. That suggests analysts think the AI story still has legs, even after the stock’s sharp run.

www.barchart.com

www.barchart.comThe Quarter Was Built on AI and Networking

HPE’s latest quarter was the kind of report investors wanted to see. Revenue climbed 40% year-over-year to $10.68 billion, well ahead of expectations. Adjusted earnings came in at $0.79 a share, up from $0.38 a year earlier and above the $0.53 Wall Street had expected. The company also posted net income of $624 million, compared with a loss in the prior-year quarter.

The strength came from more than one corner of the business. Cloud and AI revenue rose 23% to $7.71 billion, server revenue increased 33% to $5.45 billion and networking revenue surged 148% to $2.69 billion, helped by Juniper. HPE also said free cash flow hit a second-quarter record. CEO Antonio Neri said the company’s momentum reflected strong execution and growing demand tied to AI workloads.

The guidance was just as important. HPE raised full-year fiscal 2026 revenue growth guidance to 29% to 33% from 17% to 22%, and lifted its adjusted EPS outlook to $3.35 to $3.45 from $2.30 to $2.50. For the July quarter, it guided to revenue of $11.5 billion to $12.1 billion and adjusted EPS of $0.88 to $0.93, both above the Street’s view. The company also said it expects at least $3.5 billion in free cash flow for the year and raised its fiscal 2027 framework to 8% to 12% growth.

HPE Is Doing More than Just Riding AI

While AI gets most of the headlines, HPE is making several strategic moves elsewhere. The company recently completed the sale of its remaining stake in H3C, generating approximately $1.36 billion in cash.

Management is also focused on integrating Juniper Networks, a deal that expands HPE's networking capabilities and strengthens its position in AI-driven data centers. These efforts should help diversify growth while improving HPE's competitive position across enterprise technology markets.

What Analysts Think of HPE Stock?

Overall, Wall Street continues to have a positive outlook on HPE. The stock's consensus rating is a “Moderate Buy,” as rated by the 20 analysts covering the stock as per Barchart.

There are some companies that are even more positive. Morgan Stanley raised its recommendations to $71 and maintained the "Equal Weight" position due to more robust server pricing and synergy benefits. Focusing on HPE's sound second quarter performance and demand strength, Truist increased its target to $69, Citigroup took the stock to $70, JPMorgan to $68 and Evercore ISI to $70.

All in all, the revisions indicate analysts believe that spending on AI will remain robust in the years ahead, leaving HPE with plenty of runway ahead. The rally in the stock has already coincided with their valuations, but some analysts remain convinced that their scenario is still fair based on the company's growth.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

HPE Is Riding the AI Boom. Wall Street Thinks It’s Just Getting Started. Uber Stock Alert: What to Know As Uber Slashes People Team by 23% Honeywell Stock Is Likely to Reward Shareholders Following Quantinuum IPO, Split Intuitive Machines (LUNR) Stock Is Sinking. The SpaceX IPO Is Only Partly to Blame.