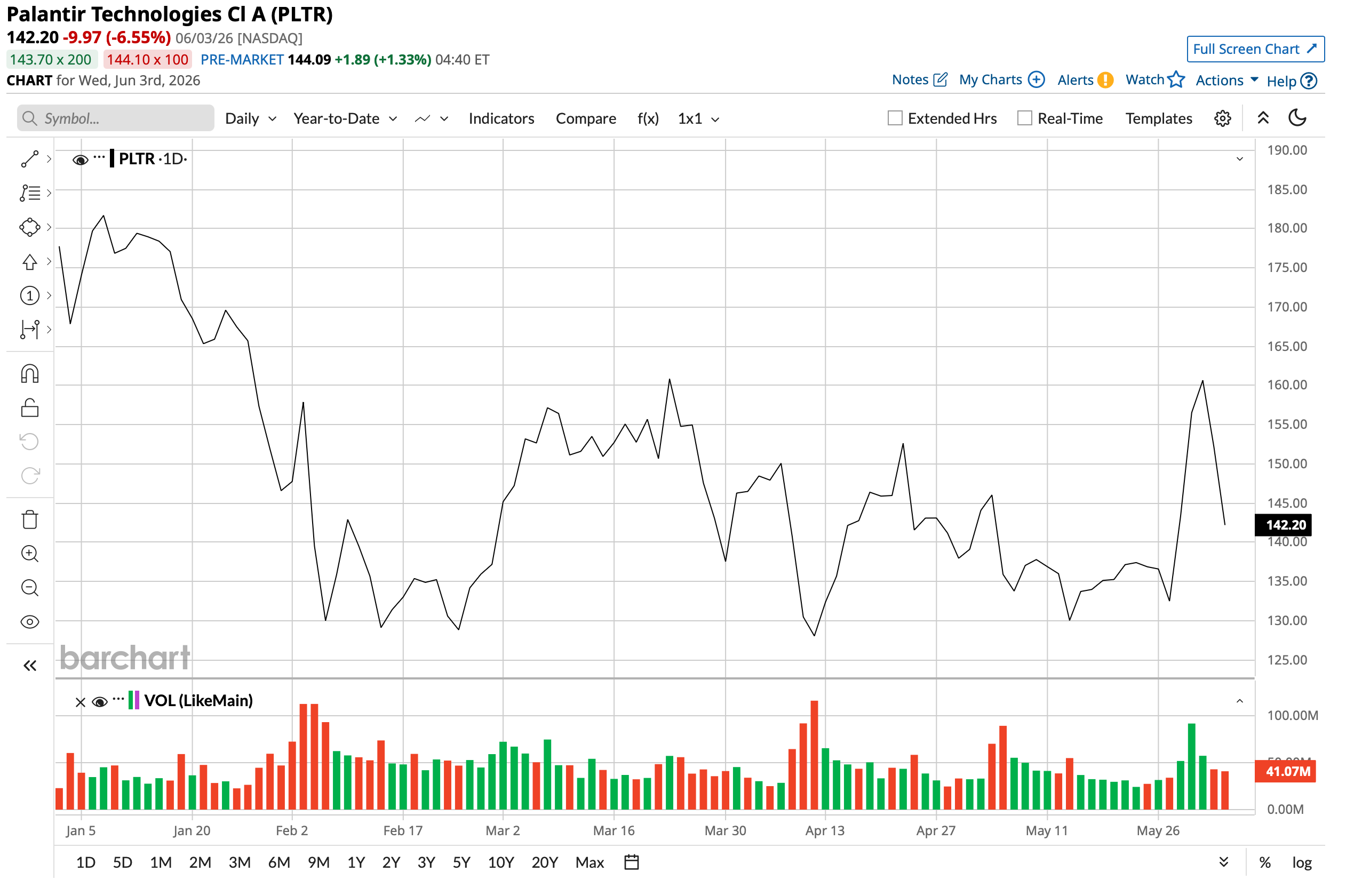

Michael Burry has struck Palantir (PLTR) again with his bearish thesis. This time it's technical. Questioning the stock's bullish momentum, Burry reckons it is at a “crossroads”, due to a head-and-shoulders pattern. The pattern is a technical formation of a stock's price movement that indicates a potential future downward movement.

And based upon this, Burry again took aim at the company, stating, “Palantir trades at ~16X its IV15 according to my assumptions. It is a sand castle, supported for now by the AI applications narrative, a short in my book.” 2026's price movement of a decline of 20% would make some believe that Burry is indeed correct. However, that would be missing the wider point: Palantir's significance for the Western World in an increasingly hostile geopolitical environment.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Undeniably Strong Financials

Before delving into Palantir's significance as a company, it must be pointed out that all of it is reflected in the exceptional growth of its financials.

Notably, Palantir delivered another set of strong financial results in Q1 of 2026 that largely followed the pattern seen in previous periods. The company once again comfortably surpassed the Rule of 40 benchmark along with consensus estimates for both revenue and earnings.

Total revenue reached $1.63 billion, reflecting an 85% increase from the same quarter a year earlier. Within this, the U.S. government revenue grew 84% to $687 million, while the U.S. commercial revenue maintained robust momentum with a 133% advance to $595 million. Notably, the remaining deal value in the commercial segment, a critical measure of future demand, more than doubled year-over-year (YOY) to $4.92 billion. Total contract value for the period came in at $2.41 billion, up 61% from the prior year.

On the profitability side, earnings per share rose to $0.33, exceeding the consensus forecast of $0.28 and marking the ninth straight quarter of beating analyst expectations. Cash generation remained impressive as net cash from operating activities nearly tripled to $899.2 million compared with the previous year. Palantir closed the quarter with $2.32 billion in cash and carried no short-term debt on its balance sheet.

Nevertheless, despite the recent drop in share price, PLTR stock still commands uncomfortably high valuations. Its forward price-to-earnings GAAP ratio of 104.96 times, price-to-sales multiple of 44.16 times, and price-to-cash flow of 78.66 times all stand significantly above their respective industry medians, implying almost no margin of error when it comes to growth.

Dynamism Added To Searing Growth

Not resting on its laurels, Palantir is not staying static. It is shifting away from a conventional SaaS approach toward becoming a core AI infrastructure platform supported by robust operational strength and powerful compounding growth dynamics.

The go-to-market mechanism accelerating adoption is the AIP Boot Camp, a five-day intensive workshop where enterprise customers go from zero to a working AI use case inside their own data environment, which earlier used to take quarters. This was reflected in the company's latest Q1 numbers, where revenue grew 85% YOY, the highest growth rate in the company's history. U.S. commercial revenue grew 133%, and management raised the full-year 2026 revenue guidance to 71% growth, citing accelerating U.S. market conditions.

Further, on the commercial side, Palantir is looking to carry on the Boot Camp momentum by converting participants into long-term platform contracts and fixing the one part of the business that has not kept pace. International commercial revenue grew only 8% YOY in Q4 2025, a jarring contrast to the triple-digit U.S. growth rates. CEO Alex Karp has been candid about the challenges in Europe, citing slow AI adoption and a preference among some enterprises for domestic vendors. The Airbus partnership extension in February 2026, a multi-year renewal of the Skywise aviation data platform now serving over 50,000 daily users, is one signal that Palantir is working on the problem rather than ignoring it, but Europe remains an open question. Domestically, the commercial growth engine is being fueled by expansion at existing customers rather than purely new logos.

Analyst Opinion On PLTR Stock?

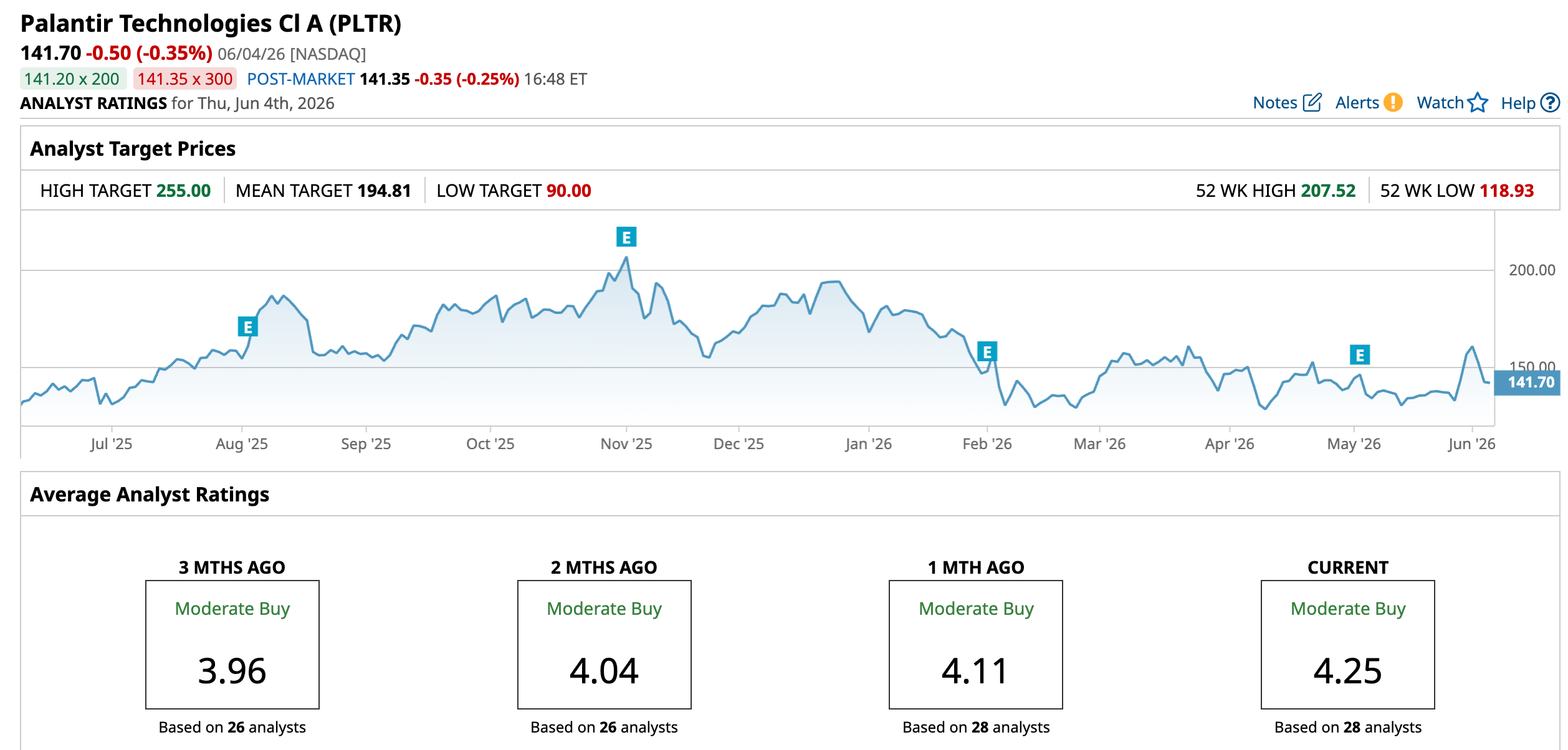

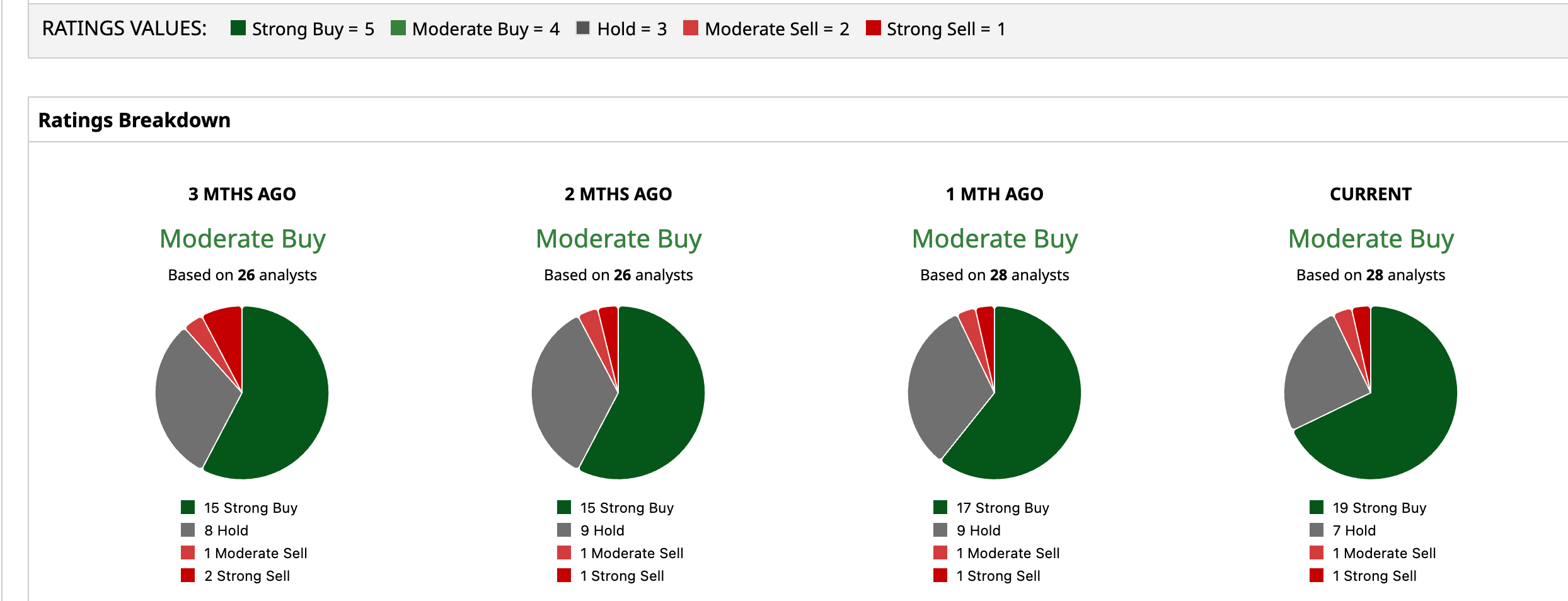

Overall, analysts have a consensus rating of “Moderate Buy” for PLTR stock. The mean target price of $194.81 implies a potential upside of 37.5% from current levels. Out of 28 analysts covering the stock, 19 have a “Strong Buy” rating, seven have a “Hold” rating, one has a “Moderate Sell” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Michael Burry Takes Aim at Palantir Stock Again, But He’s Missing the Bigger Picture AVGO Stock Alert: Why Broadcom Is Leading Chip Stocks Lower Today Why 1 Analyst Is Betting DRAM Strength Can Supercharge Sandisk Stock to $3,250 Snowflake Stock Jumps Over 40% on Strong Earnings and Amazon Deal. Its AI Strategy Is at an Inflection Point.