Serve Robotics SERV delivered a strong first-quarter performance, suggesting that its bet on Physical AI is beginning to gain commercial traction. The autonomous robotics company reported first-quarter 2026 fleet services revenues of $1.96 million, a nearly tenfold increase from $211,000 reported in the year-ago quarter. Total revenues climbed 578% year over year to $3 million, driven by growth across both fleet services and software offerings.

The sharp increase in fleet revenues reflects the rapid scaling of Serve Robotics’ autonomous platform. Following its acquisition of Diligent Robotics earlier this year, SERV now operates across 44 cities in 14 states, broadening its reach beyond sidewalk delivery into healthcare robotics and other autonomous service applications. Operational metrics highlighted the pace of expansion, with average daily active robots increasing to 812 from 73 a year ago, while daily supply hours surged to 10,295 from 648, reflecting significantly higher utilization of the company's autonomous fleet.

Management noted that with approximately 2,000 robots deployed, its focus is shifting from simply increasing fleet size to boosting revenue generated per robot and per operating hour. This transition could become increasingly important as investors look for evidence of operating leverage and sustainable unit economics.

Profitability, however, remains a key area of focus. Serve Robotics reported a net loss of $49 million, compared with $13.2 million in the prior-year quarter, as the company continued investing heavily in research and development, operational infrastructure and integration initiatives. Despite these investments, management reaffirmed its full-year 2026 revenue outlook of approximately $26 million, signaling confidence in continued demand growth across both delivery and healthcare robotics.

Taken together, the results suggest that Physical AI is beginning to move beyond the pilot stage and into broader commercial deployment. Strong growth in fleet services revenues, expanding software contributions and rising robot utilization demonstrate growing economic value from autonomous systems. The key challenge now is sustaining rapid growth while improving margins and reducing losses. If management can increase revenue per robot and scale its multi-domain platform, Physical AI could evolve into a durable, scalable business model.

Serve Robotics’ Competitor Landscape

Serve Robotics operates in the fast-growing Physical AI market, where autonomous robots are being used for real-world tasks such as food delivery, logistics and healthcare support. Two notable players in this space are Uber Technologies, Inc. UBER and DoorDash, Inc. DASH.

Uber is a key player in the broader autonomous mobility and delivery ecosystem. The company said it now has more than 30 autonomous partners across Mobility and Delivery, with AV Mobility trips growing more than 10x year over year. Uber also expects to operate in up to 15 autonomous markets by the end of 2026, giving it significant scale and commercialization reach. This large network, deep demand base and partner-led AV strategy give Uber a strong position in scaling autonomous transportation and delivery services.

DoorDash is also building an autonomous delivery platform, including its Dot program. Management noted that different delivery formats will be needed for different types of orders, across both land and air, to create a more efficient delivery network. DoorDash’s large merchant base, strong local commerce platform and focus on building end-to-end autonomous delivery capabilities could create competitive pressure for smaller robotics players over time.

SERV’s Price Performance & Valuation

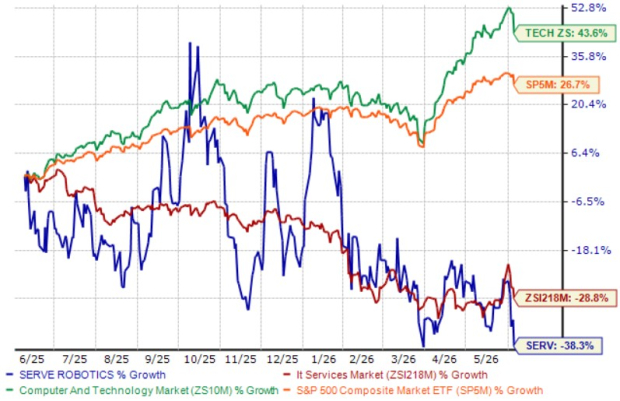

Shares of Serve Robotics have declined 38.3% in the past year, underperforming the Zacks Computers - IT Services industry, the broader Computer and Technology sector and the S&P 500 index.

SERV Stock's 12-Month Price Performance

Image Source: Zacks Investment Research

SERV stock is currently trading at a premium. It is currently trading at a forward 12-month price-to-sales (P/S) multiple of 12.39, above the industry average of 12.2.

SERV’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

SERV’s EPS Trend

The Zacks Consensus Estimate for SERV’s 2026 loss per share has widened to $2.64 in the past 30 days. Also, the estimated figure indicates a wider loss than the year-ago estimated loss of $1.63 per share.

EPS Trend of SERV Stock

Image Source: Zacks Investment Research

Serve Robotics currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Serve Robotics Inc. (SERV): Free Stock Analysis Report

Uber Technologies, Inc. (UBER): Free Stock Analysis Report

DoorDash, Inc. (DASH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).