CLOV Reports MA Membership Growth, Signals GAAP Profitability in 2026

Clover Health InvestmentsCLOV has reported strong results from the 2026 Annual Enrollment Period (AEP), delivering 53% year-over-year growth in Medicare Advantage PPO membership. After a strong enrollment period, the company is starting 2026 with total membership increasing to 153,000, reflecting growth in core markets where Clover Health has broad Clover Assistant (CA) coverage and an integrated Home Care model. As a result, Clover Health believes it will achieve full-year GAAP net income profitability in 2026.

Per management, the company is starting 2026 in a strong financial position to show the robustness of Clover Health’s model, with strong growth in new members, high retention of existing members, improving performance across member groups and continued benefits from the Clover Assistant. This disciplined growth approach, coupled with strong retention, positions the company to achieve GAAP net income profitability for the first time in 2026.

CLOV Stock’s Trend Following the News

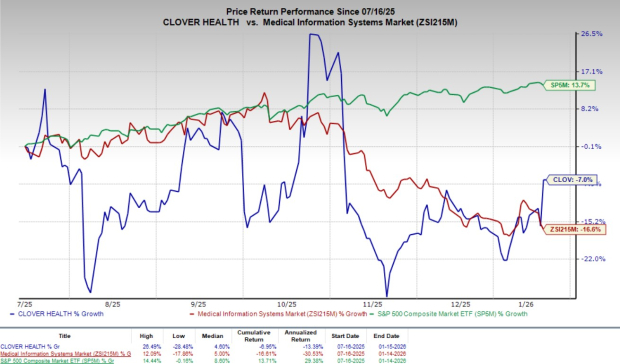

Following the announcement, shares of Clover Health rallied 10.6% at yesterday’s closing. Over the past six months, the stock has lost 7% compared with the industry’s 16.6% decline, However, the S&P 500 has risen 13.7% during the same time frame.

In the long run, achieving full-year GAAP net income profitability would mark an important inflection point for Clover Health Investments. Membership growth and retention, improved cohort performance, operating leverage from SG&A efficiency and the scaling impact of Clover Assistant could drive margins and earnings. These dynamics position Clover Health to demonstrate the scalability of its technology-enabled MA model while laying the foundation for sustainable growth beyond.

CLOV currently has a market capitalization of $1.45 billion.

Image Source: Zacks Investment Research

More on the AEP Performance & Profitability Outlook

Clover Health expects multiple tailwinds to support profitability, including improvement in the performance of new members and continued strong results from returning members, alongside sustained membership growth. This outlook is supported by higher payments from its 4.0-star-rated PPO plans in 2026, a favorable CMS rate update and increased Part D subsidies, strong member retention, expanded use of the Clover Assistant by PCP and improved operating efficiency as SG&A costs decline with scale.

By maintaining stable plan benefits year over year, Clover Health retained more than 95% of its members during the enrollment period and built a stronger presence in local communities. This shows the durability of the company’s membership base and its plans to continue to offer strong value to members. CLOV saw intentional growth in its PPO plans, with new members switching from other Medicare Advantage plans within Clover’s core markets.

Clover Health’s 2026 AEP results underscore the effectiveness of its focused growth strategy. More than 97% of its Medicare Advantage members are enrolled in its main PPO plan. For the second consecutive year, this plan is ranked the number one PPO plan in the country based on HEDIS quality measures. Clover Health’s AI-enabled, industry-leading quality highlights the strong quality of care it provides and the solid financial performance of its model.

Industry Prospects Favoring Market

Going by data provided by Precedence Research, the individual health insurance market is valued at $150.05 billion in 2025 and is expected to witness a CAGR of 6.43% through 2035. Factors like the changing landscape of healthcare and the need for protection against medical expenses, the integration of technology to enhance customer experiences through digital platforms, telehealth services and data-driven insights improving service efficiency and customer satisfaction influence market growth.

Other News

Counterpart Health, a subsidiary of Clover Health, reported strong 2025 results, showing how its AI-powered Counterpart Assistant (CA) improves care quality and lowers costs. Adoption of the platform grew rapidly, with live third-party clinicians increasing by more than 450% year over year across multiple states.

Data showed that returning Clover members whose primary care physicians (PCPs) use CA achieved about a 1,500 basis point improvement in medical cost ratios compared to those without CA. Counterpart’s technology also supported the nation’s top-ranked PPO Medicare Advantage HEDIS quality scores for the second consecutive year.

Clinical studies released in 2025 showed earlier diagnosis of chronic diseases like COPD, fewer hospitalizations and readmissions for conditions such as heart failure and COPD and better outcomes in underserved communities. In addition, Counterpart expanded its platform with ambient scribing, natural-language search, proactive visit summaries and enterprise-level tools, positioning it as a full clinical operating system for value-based care.

Clover Health Investments, Corp. Price

Clover Health Investments, Corp. price | Clover Health Investments, Corp. Quote

CLOV’s Zacks Rank & Stocks to Consider

Currently, CLOV carries a Zacks Rank #3 (Hold).

Some better-ranked stocks from the broader medical space are AtriCure ATRC, Phibro Animal Health PAHC and Omnicell OMCL.

AtriCure, currently flaunting a Zacks Rank #1 (Strong Buy), reported a third-quarter 2025 adjusted loss per share of 1 cent, 90.9% narrower than the Zacks Consensus Estimate. Revenues of $134.3 million beat the Zacks Consensus Estimate by 2.1%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ATRC has an estimated earnings growth rate of 64.2% for 2025 compared with the industry’s 12.2% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 67.06%.

Phibro Animal Health, carrying a Zacks Rank #2 (Buy) at present, reported third-quarter 2025 adjusted earnings per share (EPS) of 73 cents, which surpassed the Zacks Consensus Estimate by 23.7%. Revenues of $363.9 million beat the Zacks Consensus Estimate by 2.6%.

PAHC has an estimated long-term earnings growth rate of 12.8% compared with the industry’s 13.9% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 20.77%.

Omnicell, carrying a Zacks Rank #2 at present, reported third-quarter 2025 adjusted EPS of 51 cents, which surpassed the Zacks Consensus Estimate by 41.7%. Revenues of $311 million beat the Zacks Consensus Estimate by 5.6%.

OMCL has an estimated long-term earnings growth rate of 9.4% compared with the industry’s 27.9% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 38.65%.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL): Free Stock Analysis Report

AtriCure, Inc. (ATRC): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

Clover Health Investments, Corp. (CLOV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).