Oracle Corporation (ORCL) has been reporting strong numbers. Recently, the company reported Q4 FY26 numbers, which beat analyst estimates from a top-line and EPS perspective. At the same time, the company’s guidance topped estimates. It's, however, worth noting that ORCL stock corrected sharply and has been largely sideways in the last 52 weeks.

The reason is Oracle’s planned capital expenditure of $95 billion for FY27. To support the big investment plans, Oracle will be raising $40 billion in debt and equity. At the same time, Oracle has guided for gross margin compression as the company ramps up data center projects.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Amidst the spending boom, it might be a good time to consider ORCL stock. There is likely to be some stress on the balance sheet in the near term. However, once the spending cycle is completed, margins will improve, and cash flow is expected to swell. This will translate into improvement in credit metrics.

Citi has maintained a “Buy” rating for Oracle with a price target of $330. According to Citi analyst, the company is “on track to deliver one of the strongest revenue/EPS accelerations in tech as large AI contracts ramp.” Therefore, the current weakness in ORCL stock seems like a good buying opportunity.

About Oracle Stock

Headquartered in Austin, Oracle is a provider of products and services that address enterprise information technology needs. These products and services include enterprise applications and infrastructure offerings, with global delivery, through flexible and interoperable IT deployment models.

Oracle Cloud license and on-premise license deployment offerings include Oracle Applications, Oracle Database, and Oracle Middleware software. Further, Oracle hardware products include Oracle Engineered Systems, servers, storage, and industry-specific products.

For FY26, Oracle reported revenue growth of 17% on a year-on-year (YoY) basis to $67.4 billion. For the same period, the company’s non-GAAP operating income and operating cash flow were $28.9 billion and $32 billion, respectively.

While the company’s growth and cash flows have been healthy, the markets have shown concern related to high capital investments. As a result, ORCL stock has declined by 4% in the last six months and about 7% year-to-date (YTD).

www.barchart.com

www.barchart.com Swelling Order Backlog

At the end of FY25, Oracle had reported a remaining performance obligation of $138 billion. The company’s RPO has swelled significantly in FY26 to $638 billion and provides clear revenue visibility.

The strong growth in RPO is on the back of demand for cloud infrastructure for AI training and inferencing. The robust increase in RPO also justifies the aggressive stance related to capital investments.

It’s also important to mention that the prepaid and customer-supplied hardware portion of the large AI contracts has increased to $75 billion. This reduces the amount Oracle has to invest to build out AI data centers.

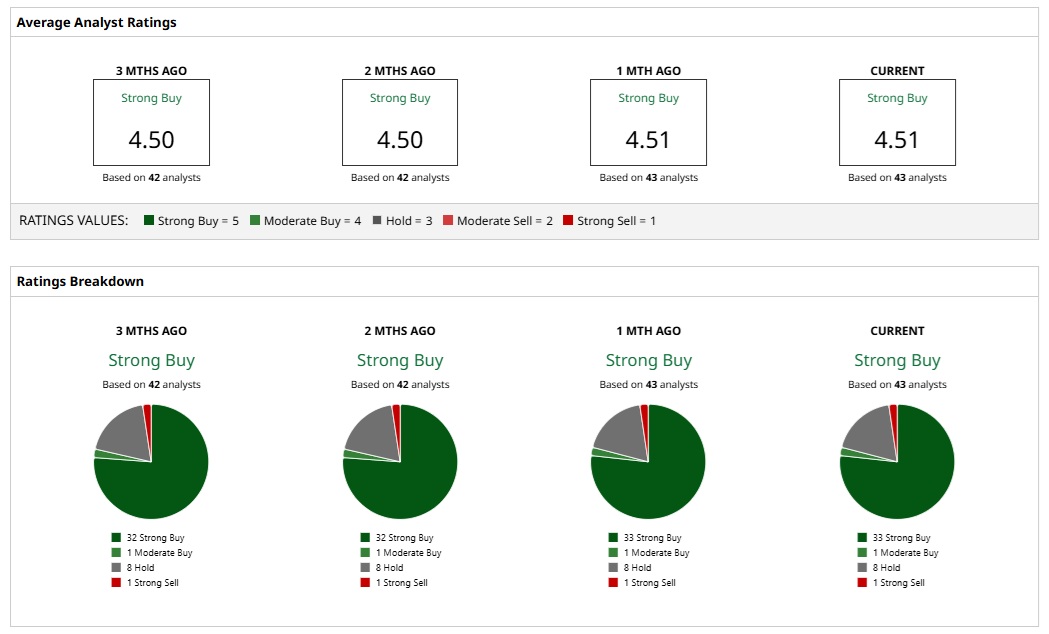

What Do Analysts Say About ORCL Stock?

Based on 43 analysts with coverage, ORCL stock has a consensus “Strong Buy” rating. While 33 analysts have a “Strong Buy” rating for ORCL stock, one has a “Moderate Buy,” eight have a “Hold” rating, and one analyst has a “Strong Sell” rating.

The mean price target of $256.07 represents a potential upside of 40% from current levels. Further, the most bullish price target of $400 suggests that ORCL could climb as much as 119% from here.

www.barchart.com

www.barchart.com Concluding Views

From a valuation perspective, ORCL stock trades at a forward price-earnings ratio of 31.82. While analysts expect FY27 earnings growth to be muted at 0.32%, it’s likely to accelerate to 25.28% in FY28. With some big investments, growth can potentially be robust beyond the next 24 months. The stock therefore seems to be at an appealing price point after the recent correction.

For Q1 FY27, Oracle has guided for revenue growth in the range of 27% to 29%. Further, in constant currency, cloud revenue growth is estimated in the range of 57% and 63%. Therefore, with a positive outlook for the upcoming quarter, swelling RPO, and structural industry tailwinds, ORCL stock is attractive.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

COIN Stock Alert: What to Know as Coinbase Launches AI Trading Tool Oracle vs. IBM: 1 Legacy Tech Giant Is Winning the AI Race As Remaining Performance Obligation Swells, Oracle Stock Is Positioned for Growth Acceleration These 3 Quality Stocks Will Make You Want to LEAP on Their Calls