Michael Burry — the man who famously predicted and bet on the 2008 housing market crash — recently expressed his opinion on the SpaceX (SPCX) initial public offering (IPO). Rather unsurprisingly, Burry isn’t impressed by SpaceX's high valuation, saying that the market has become too caught up in artificial intelligence (AI) and related industries.

Even though he is unimpressed by the high valuation, Burry also refuses to short SPCX stock, saying that none of the put options looked attractive considering the risk he would have to take. Without a doubt, one component of this risk is Elon Musk, who made short sellers pay dearly when raising Tesla (TSLA) to become an electric vehicle (EV) giant. Burry called SpaceX a number of things — including a “bedeviled social media company,” referring to the company’s ownership of X (formerly Twitter) — and is appalled that a company generating less than $20 billion in revenue is worth more than a company like Berkshire Hathaway (BRK.A).

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In a June 12 post on his Substack, which is now how he declares his recent buys, Burry pointed out the three stocks he is buying instead.

Michael Burry Stock # 1: Adobe (ADBE)

Adobe (ADBE) is a technology company that provides multimedia and digital marketing software. The company operates through three segments: Digital Media, Digital Experience, and Publishing and Advertising. Its product portfolio includes widely used applications such as Illustrator, Photoshop, and InDesign. Moreover, the company offers AI products such as Firefly and Sensei. Founded in 1982, Adobe is headquartered in San Jose, California.

Although the software sector delivered weak performance over the past year, Adobe’s decline was even steeper. ADBE stock has lost 48% of its value over the last 12 months, while the iShares Expanded Tech-Software Sector ETF (IGV) has fallen by approximately 17% during the same period. Much of the stock’s decline has stemmed from a sharp selloff that began in January and has persisted to date.

www.barchart.com

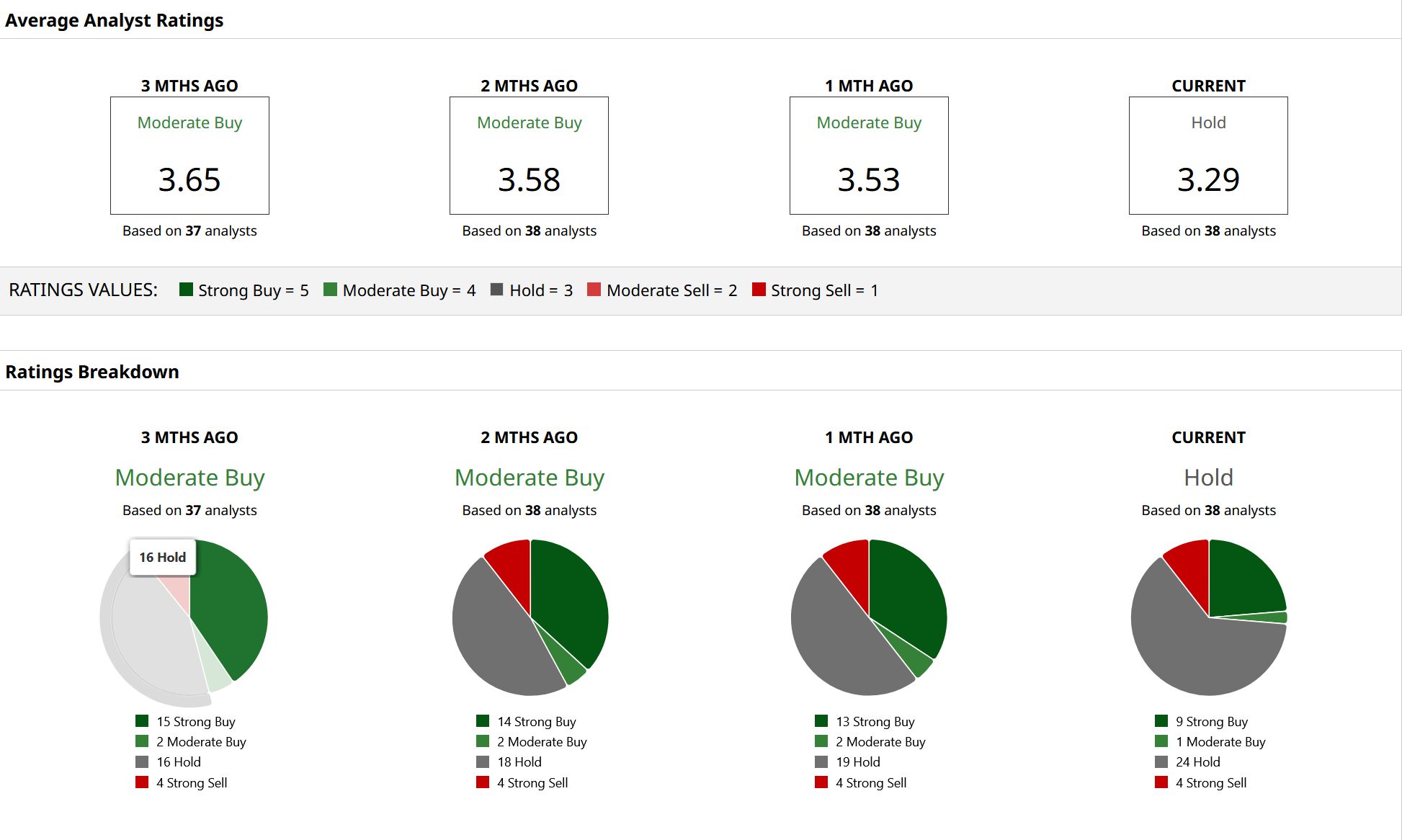

www.barchart.com Michael Burry believes margins near all-time highs and a shrinking valuation make Adobe a deep value stock. ADBE stock’s forward price-to-earnings (P/E) ratio has now fallen to 9.8 times, which is roughly one-third of the IT sector median of about 33 times. This is also well below the stock’s five-year average forward P/E.

Read more: AI is “one of the largest industries ever” ...and it’s already disrupting this $1T market

Adobe posted second-quarter fiscal 2026 results on June 11, reporting total annual recurring revenue (ARR) of $27.1 billion. This figure included approximately $480 million contributed by the Semrush acquisition. Customer Group subscription revenue came in at $6.39 billion, with Semrush contributing around $40 million. The company also reported remaining performance obligations (RPO) of $22.27 billion and generated $2.17 billion in operating cash flow during the quarter.

Analysts have become more cautious on Adobe after the earnings report. On June 12, Citi lowered its price target on ADBE stock from $264 to $228 while keeping a “Neutral” rating. According to the firm, Adobe’s Q2 earnings were relatively solid but pointed to increasing signs of disruption in the business. On the same day, other analysts also cut their price targets, reflecting a more cautious overall outlook.

www.barchart.com

www.barchart.com Michael Burry Stock # 2: PayPal (PYPL)

Based in San Jose, California, PayPal (PYPL) is a global digital payments company that allows businesses and customers around the world to receive and make payments in person and online. PayPal offers payment solutions under the PayPal Credit, Hyperwallet, Venmo, PayPal, Xoom, Honey, Braintree, and Paidy names.

Over the past year, PYPL stock has lost approximately 40% of its value. In comparison, the Global X FinTech ETF (FINX) has declined roughly 24% during the same period. This suggests that the company has underperformed the broader fintech sector, which has experienced a less severe downturn. A similar pattern is evident on a year-to-date (YTD) basis, with PYPL stock down around 27% compared to a decline of about 17% for the exchange-traded fund (ETF).

www.barchart.com

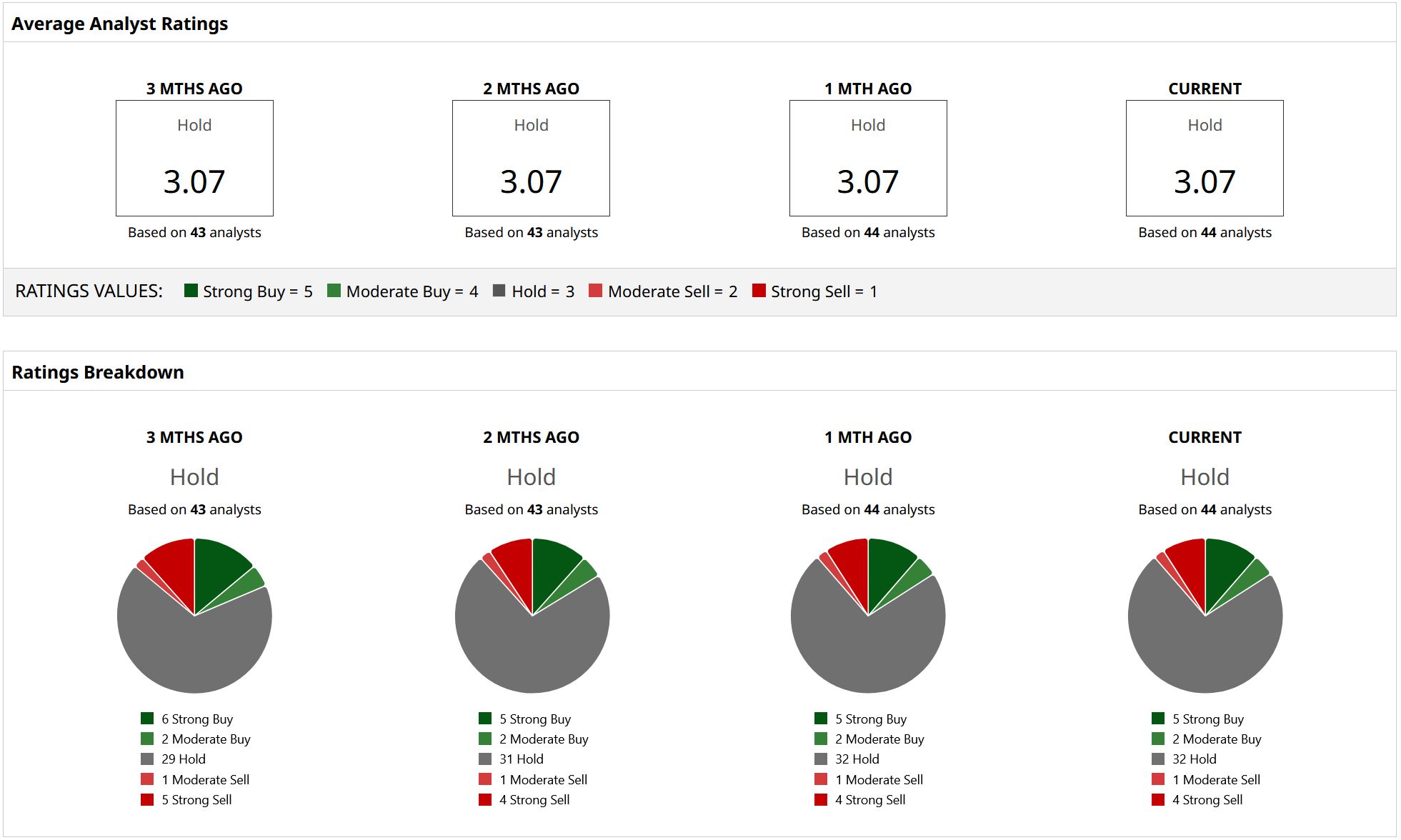

www.barchart.com Burry believes PayPal's forward P/E of 8 times is as attractive as it can get for a leading payments firm. Like Adobe, PayPal is also trading at a discount to its five-year average forward P/E.

The company posted Q1 fiscal 2026 results on May 5, reporting 7% year-over-year (YOY) revenue growth to $8.4 billion. Transaction revenue came in at $7.5 billion, rising 7% YOY, while revenue from other value-added services rose 10% to $852 million. The company repurchased $1.5 billion worth of shares during the quarter. At the end of Q1, PayPal had $13.5 billion in cash, cash equivalents, and investments as well as $11.6 billion in debt. For Q2, the company expects low single-digit revenue growth on a currency-neutral basis.

Read more: This Pre-IPO stock is up 4,000% already

The latest updates suggest that analysts have mixed views on PYPL stock. In May, Canaccord Genuity reaffirmed a “Hold” rating on PayPal with a price target of $42. Following Q1 earnings, Truist lowered its price target from $45 to $44 while reiterating a “Sell” rating. The firm also lowered its revenue forecast due to increased spending on loyalty and rewards programs and weaker international total payment volumes.

www.barchart.com

www.barchart.com Michael Burry Stock # 3: Alibaba (BABA)

Founded in 1999 and based in Hangzhou, China, Alibaba (BABA) operates as a technology infrastructure and marketing solutions provider. The company operates through its Alibaba International Digital Commerce Group (AIDC), Alibaba China E-Commerce Group, Cloud Intelligence Group, and other segments. Its product portfolio includes platforms such as Tmall, Taobao, AliExpress, Alibaba.com, and Lazada as well as services like Amap navigation, Alibaba Cloud, Cainiao logistics solutions, and more.

Over the last 12 months, BABA stock has clearly underperformed the broader technology sector, down around 7%. In contrast, the iShares U.S. Technology ETF (IYW) has delivered gains of about 54% during the same period. The performance has widened further on a YTD basis, as the stock continues to lag behind the ETF.

www.barchart.com

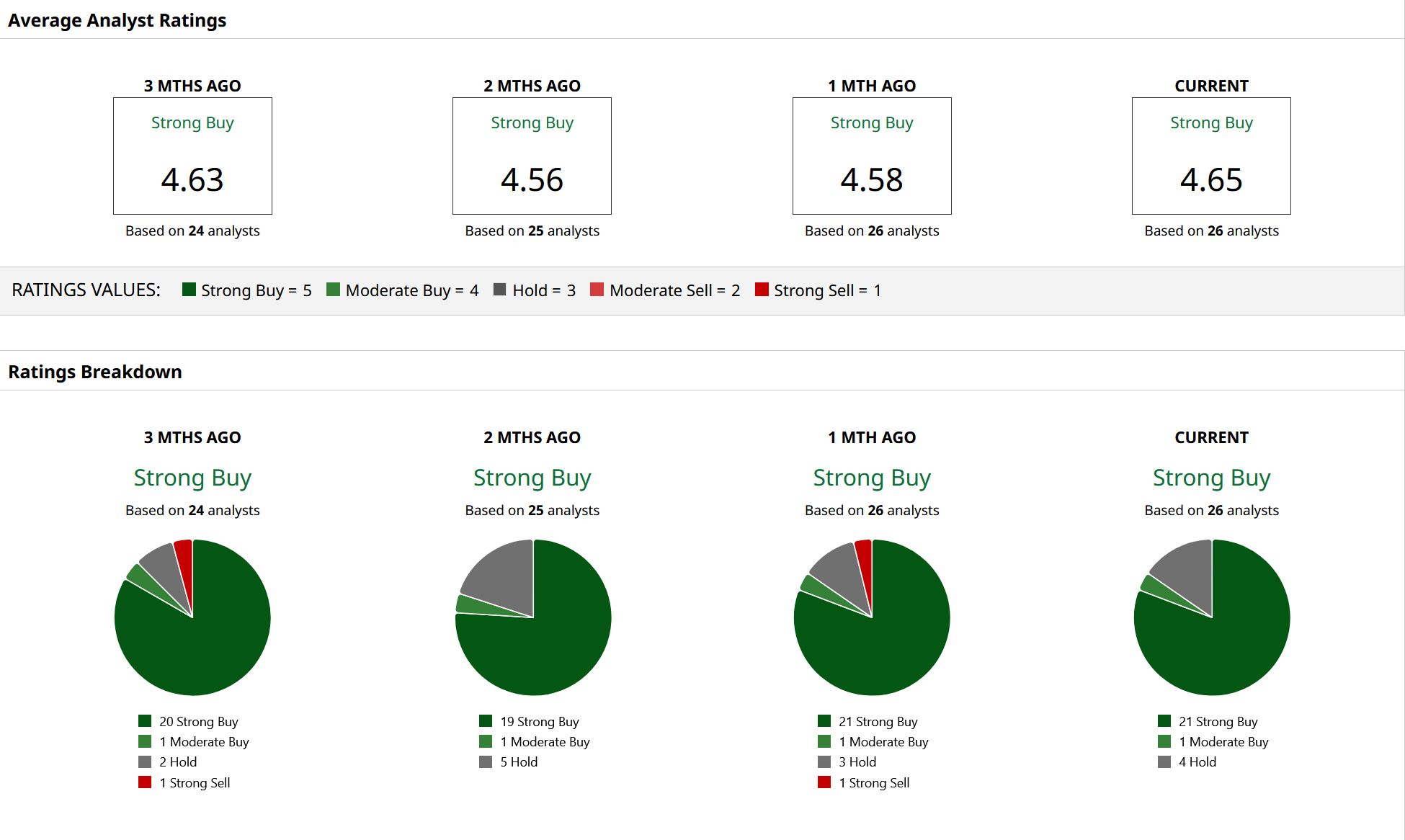

www.barchart.com Michael Burry believes Alibaba is the most advanced AI company in China. BABA stock has dropped around 40% from its peak last year, and the company is aggressively buying back its own stock. Burry has compared Alibaba to Amazon (AMZN) and believes the value is accreting to shareholders even if the market price doesn’t reflect that yet. While this comparison may not be entirely fair, considering how U.S. investors have viewed Chinese companies in the past, it does give an idea of the value he sees in the company.

Alibaba reported Q4 fiscal 2026 earnings on May 13, posting 3% YOY revenue growth to $35.28 billion, missing market expectations slightly. On the earnings side, non-GAAP earnings came in at $0.01 per share. Adjusted EBITA fell significantly by 84% YOY to $740 million. This decline was mainly due to higher investments in quick commerce, technology businesses, and user experience improvements.

Bernstein has reiterated an “Outperform” rating on Alibaba stock along with a $180 price target. Overall, BABA stock enjoys a consensus “Strong Buy” rating from 26 Wall Street analysts with coverage. The average price target of $187.55 implies potential upside of 79% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Mark Cuban Says OpenAI Is ‘Sh*tting Away’ Its Money on AI Infrastructure: Says ‘They’ll Never Get’ a Return on Their Trillion-Dollar Spending Spree Marvell Just Got a New Street-High Price Target. Wall Street Thinks Networking Is a Huge Growth Opportunity. Michael Burry Just Refused to Buy the SpaceX IPO. Here Are 3 Companies He Is Buying Instead. Intel Will Design and Manufacture Chips for Apple. What This Really Means for INTC Stock Investors.