Alibaba Group (BABA) has evolved from China’s e-commerce giant into one of the country’s largest cloud computing and artificial intelligence (AI) companies. As Alibaba pours billions into expanding its AI and cloud capabilities, investors have increasingly been asking whether those investments can drive future growth without putting too much pressure on profits. That question has become especially important ahead of the company’s fiscal first-quarter earnings report, when investors will get a detailed look at its June-quarter performance.

On Wednesday, the market got an encouraging early signal. Alibaba’s shares surged 11%, marking their biggest one-day gain since September, after reports from an analyst briefing suggested the company’s June-quarter results were shaping up better than expected. Losses in Alibaba’s instant-commerce business narrowed significantly during the quarter, while overall profitability remained intact. That helped ease concerns that the company’s expensive competition with rivals in food delivery and local services was becoming a bigger drag on earnings.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The update also reinforced a broader theme that investors have been hoping to see. Rather than chasing growth at any cost, Alibaba appears to be showing that it can continue investing heavily in AI and cloud infrastructure while still keeping its financials on solid ground. If the company delivers on that when it reports its Q1 results next month, investors may begin focusing less on near-term spending and more on the long-term value those investments could create.

With that in mind, let’s take a closer look at BABA stock now.

About Alibaba Stock

With a market capitalization of $261.6 billion, Alibaba Group has grown from a small online marketplace into one of China’s most influential technology companies. Founded by Jack Ma in 1999, Alibaba now operates a vast ecosystem spanning e-commerce, cloud computing, logistics, digital payments, and artificial intelligence.

Its platforms connect millions of consumers and businesses, while Alibaba Cloud has emerged as a key player in China’s fast-growing AI industry. As the company ramps up investments in AI infrastructure and next-generation cloud services, Alibaba is increasingly positioning itself as a long-term tech leader rather than just an e-commerce giant.

After delivering a stellar run in 2025, BABA stock has had a much tougher journey this year. Shares climbed to a 52-week high of $192.67 last October, and optimism remained strong enough for the stock to rally back to $181.10 in late January 2026. However, persistent concerns over slowing growth, heavy spending on AI infrastructure, and intense competition in China's e-commerce and instant-delivery markets gradually weighed on investor sentiment. As those concerns mounted, Alibaba gave back much of its earlier gains.

Even after Wednesday’s powerful rally, the stock remains 43.3% below its 52-week high and 38% below its 2026 peak. Year-to-date (YTD), Alibaba’s shares are still down 25.7%, while they have slipped 12.87% over the past three months. Nevertheless, the recent rebound has been meaningful, with the stock climbing 13.53% over the past five trading sessions as investors began reassessing the company’s long-term outlook.

Alibaba’s latest rally was not driven by just one headline. Beyond the encouraging profitability update, investors also welcomed reports that Alibaba Cloud’s AI-driven growth continues to accelerate. The company is also bringing its AI models and agent offerings together under the Qwen brand, a move that could simplify its AI strategy and strengthen its competitive position. Ongoing share buybacks further signaled management’s confidence in the business.

On top of that, investor sentiment got another lift after a U.S. federal judge temporarily blocked restrictions tied to the Pentagon’s designation of Alibaba while the company’s legal challenge moves forward, removing a near-term uncertainty for the tech giant.

The improving sentiment is also beginning to show up on the charts. Trading volume has turned noticeably stronger over the past few sessions, with the latest session’s volume more than tripling. Meanwhile, the 14-day RSI has climbed to 54.06, suggesting bullish momentum is gradually building again.

www.barchart.com

www.barchart.com Valuation-wise, BABA is priced at 15.68 times forward adjusted price-to-earnings, sitting below the sector median. With analysts expecting double-digit profit growth next fiscal year, that valuation looks increasingly attractive.

A Snapshot of Alibaba’s Q4 Report

When Alibaba released its fiscal fourth-quarter 2026 earnings report in May, it suggested strong progress in AI and cloud computing, but continued pressure on profitability as the company invests aggressively for future growth. The company fell short of Wall Street’s earnings expectations for the fourth consecutive quarter, sending BABA stock lower as investors focused on weaker earnings and rising costs.

For the quarter, Alibaba generated $35.3 billion in revenue, up 3% year-over-year (YOY). On a like-for-like basis, excluding the impact of disposed assets, revenue growth was a much healthier 11%. However, earnings painted a different picture. Adjusted earnings came in at just $0.09 per share, down 95% from a year earlier.

The company’s core China e-commerce business also delivered mixed results. Customer management revenue, Alibaba’s largest source of sales, increased only 1% YOY. Management noted that growth would have been closer to 8% if not for the revenue impact from a new business development program, suggesting the underlying business remained healthier than the headline numbers implied.

Cloud computing, meanwhile, continued to be the company’s biggest bright spot. Revenue from Alibaba Cloud jumped 38%, while adjusted EBITA surged 57%. Even more encouraging, AI-related cloud revenue posted triple-digit growth for the 11th consecutive quarter, highlighting the strong demand for the company’s AI infrastructure and services.

However, total adjusted EBITA plunged 84% YOY to $740 million, with margins shrinking to just 2% from 14% a year ago. Alibaba also reported an operating loss of $123 million and burned $2.5 billion in cash during the March quarter, largely due to spending on quick commerce, expanding cloud infrastructure, and acquiring users for its Qwen AI platform.

While those numbers initially worried investors, recent updates suggesting that quick-commerce losses are narrowing have raised hopes that Alibaba’s heavy AI and cloud investments may finally be moving closer to delivering profitable growth.

Over the past year, the company has steadily strengthened its AI ecosystem, and those investments are beginning to show results. According to Frost & Sullivan, Alibaba Cloud now holds a 40.1% share of China’s full-stack AI cloud market, larger than the combined share of its biggest domestic competitors.

During the June quarter, Alibaba also unified its AI products under the flagship Qwen brand while continuing to expand its global cloud network to 105 availability zones across 32 regions. With AI-driven cloud growth accelerating, investors viewed the company’s latest update on profitability as evidence that Alibaba’s AI strategy is becoming financially sustainable.

Analysts tracking Alibaba expect its earnings path to look resilient. Q1 EPS is expected to rise 29.1% YOY to $2.44. Looking ahead to fiscal 2027, profit is expected to be somewhere around $6.26 per share, up 93.8% annually, and then climb by 43.3% YOY to $8.97 per share in fiscal 2028.

What Do Analysts Expect for Alibaba Stock?

Wall Street is becoming increasingly optimistic about Alibaba ahead of its fiscal first-quarter results. UBS analyst Kenneth Fong believes the company likely delivered margin expansion alongside healthy revenue growth in the June quarter, supported by an estimated 45% growth in Alibaba Cloud.

Meanwhile, Jefferies analyst Thomas Chong expects Alibaba to execute well despite a softer consumer environment, with AI demand driving stronger-than-expected cloud performance. Plus, Jefferies continues to view Alibaba as its top pick in China’s internet sector.

The brokerage expects Alibaba to generate RMB270 billion in June-quarter revenue, up 9% YOY, broadly in line with Wall Street’s estimates. While China e-commerce customer management revenue is projected to decline 6.5%, Jefferies forecasts 45% growth for Alibaba Cloud, ahead of the consensus, driven by robust AI demand. The brokerage firm also believes Alibaba’s core e-commerce business remains a powerful cash generator, while continued AI monetization and market share gains at Tmall could provide meaningful long-term upside.

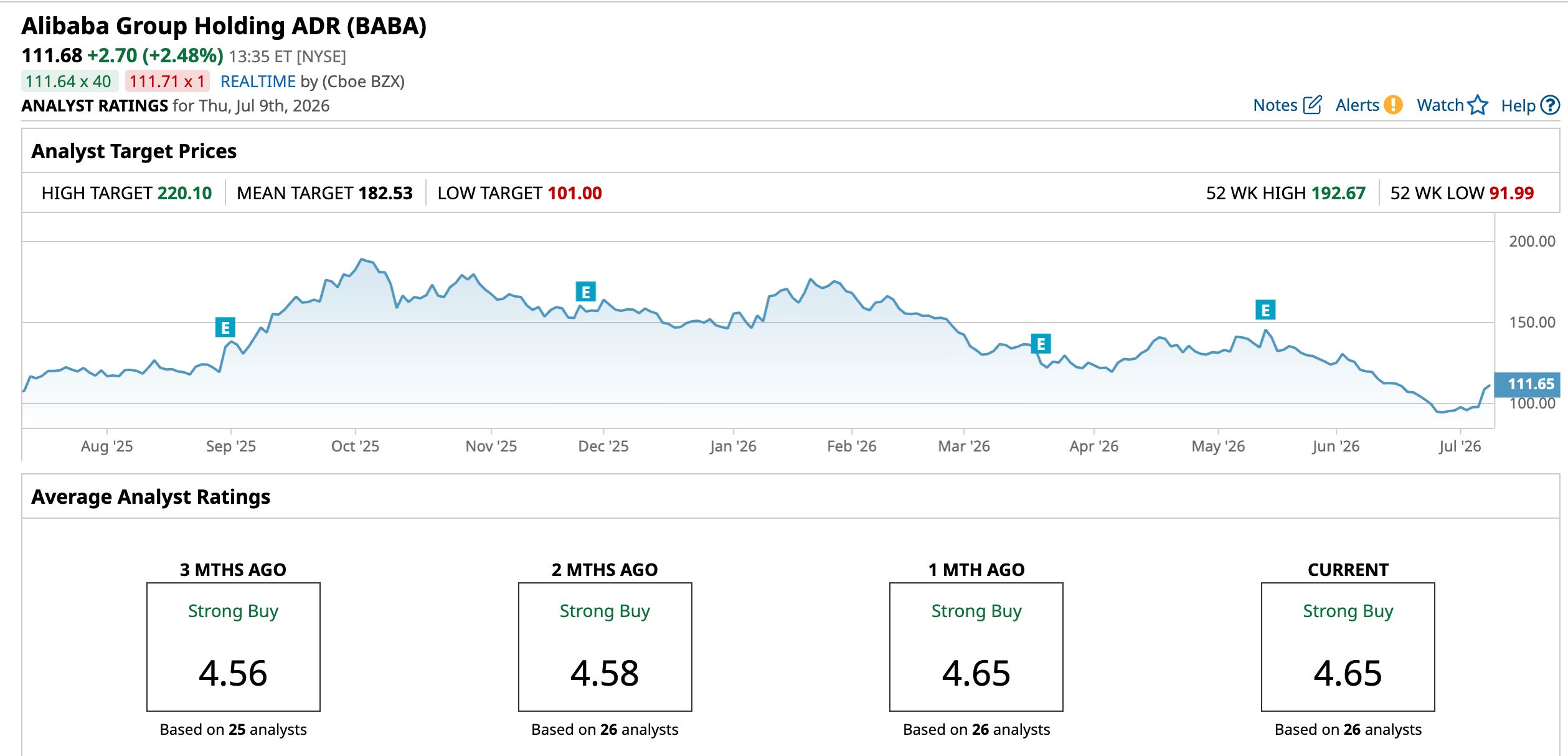

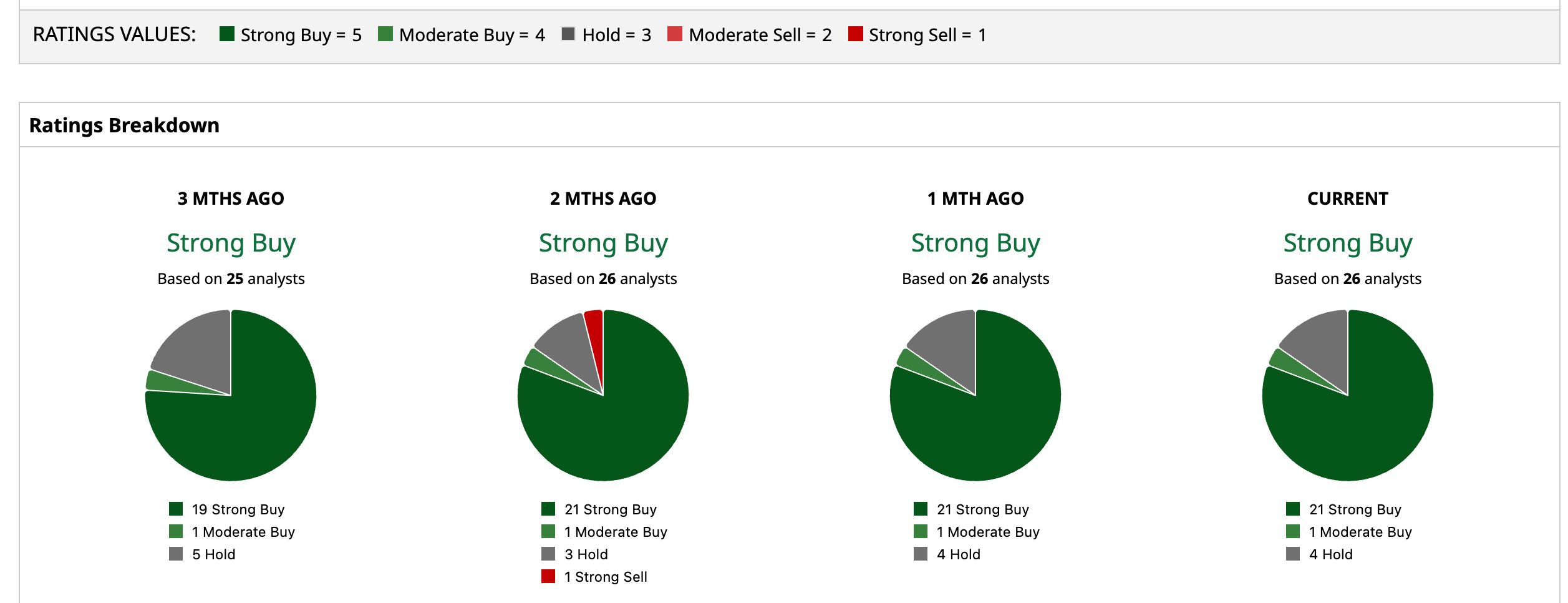

Overall, analysts are upbeat, with BABA currently rated a “Strong Buy.” Of the 26 analysts covering the stock, 21 suggest a “Strong Buy,” one advises a “Moderate Buy,” and four recommend a “Hold” rating.

The mean price target of $182.53 suggests the stock could surge by 63.4% from the current price levels. The Street-high target of $220.10 represents a potential upside of 97%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Alibaba Stock Just Got a Major Boost as Financials Justify Its CapEx Occidental Petroleum Stock’s Unusual Options Activity Signals Bullish Bets Amid Oil Rally Broadcom Sends Massive Market Signal with $30 Billion Apple Pact Here’s Why TSMC Investors Are Counting Down to July 16