After a strong rally, Micron (MU) stock has pulled back about 31% from its high. Several factors have contributed to the selloff. Investors have locked in profits following the stock's impressive run, while concerns over intensifying competition and fear of softer memory chip pricing have weighed on sentiment. In addition, the broader pullback in AI hardware and semiconductor stocks has added pressure on Micron shares.

However, the recent decline could be the best time to buy. Despite near-term market concerns, the underlying fundamentals of the memory industry remain healthy. Demand for DRAM and NAND memory continues to be robust, supported by AI infrastructure investments, data center expansion, and growing memory requirements across multiple end markets, including PC and mobile, and automotive and robotics. Memory pricing has also remained strong, providing a favorable backdrop for Micron's earnings.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Micron’s valuation has become more attractive following the correction, offering investors the chance to buy shares at a more favorable price. Moreover, Micron's strategic customer agreements (SCAs), which provide greater visibility into future demand and pricing, help reduce earnings volatility and strengthen the company's long-term growth prospects.

Let's take a closer look at what could drive MU stock higher.

www.barchart.com

www.barchart.com Micron’s Growth Isn’t Slowing Down

Micron continues to deliver exceptional results, with solid AI-driven demand, favorable pricing, and tight industry supply. After a record-breaking fiscal third quarter, the company's momentum shows little sign of slowing.

Micron reported fiscal third-quarter revenue of $41.5 billion, a 346% year-over-year (YoY) increase. The company also delivered its largest sequential revenue increase in history, with sales rising by $17.6 billion from the previous quarter.

The significant growth reflects strong customer demand for both DRAM and NAND memory products. However, the biggest catalyst remained pricing. Tight industry supply and an improved product mix enabled Micron to command significantly higher prices across its portfolio, resulting in substantial revenue and margin expansion.

During the third quarter, DRAM average selling prices increased in the low-60% range, reflecting tight supply conditions and a favorable product mix. NAND prices rose in the mid-80% range. The favorable environment appears likely to persist. Demand for high-bandwidth memory (HBM) remains solid, and supply remains tight, which is likely to keep the pricing higher in the quarters ahead.

Looking ahead, Micron expects fiscal fourth-quarter revenue of approximately $50 billion at the midpoint of its guidance, representing 342% YoY growth and another strong sequential increase. Profitability is also expected to improve, with gross margin projected to reach approximately 86%, up from 84.9% in the third quarter and 45.7% in the same period last year.

Micron’s earnings are on track to hit $31 per share, a massive increase from $3.03 in the prior-year quarter and $25.11 in the third quarter.

With AI adoption accelerating, supply remaining constrained, and pricing expected to stay favorable, Micron appears well-positioned to deliver strong growth, which will likely lead to a solid recovery in its share price.

Micron’s SCAs Strengthen the Bull Case

Micron's long-term supply agreements (SCAs) make its earnings more predictable and reduce the cyclical swings that have historically weighed on the stock. The company has signed 16 multi-year contracts covering roughly 20% of DRAM and one-third of NAND production through 2030. Management expects similar agreements to eventually account for more than half of total revenue.

Most of these are take-or-pay contracts with pricing floors and ceilings, securing customer demand while protecting margins during downturns. Fourteen agreements alone represent about $100 billion in minimum contracted revenue.

Beyond improving revenue visibility, the SCAs strengthen customer supply assurance, stabilize cash flow, and support structurally higher profitability. Overall, these agreements position Micron to deliver stronger earnings and strengthen its bull case.

MU Stock Trades at an Attractive Multiple

Micron is poised for explosive earnings growth over the next two fiscal years, yet its valuation remains surprisingly low. The stock trades at 12.9 times forward earnings, which is compelling given its ability to deliver outsized EPS growth.

Wall Street expects Micron's earnings to surge 85% YoY in fiscal 2026, followed by another 112.9% increase in fiscal 2027, even against challenging comparisons.

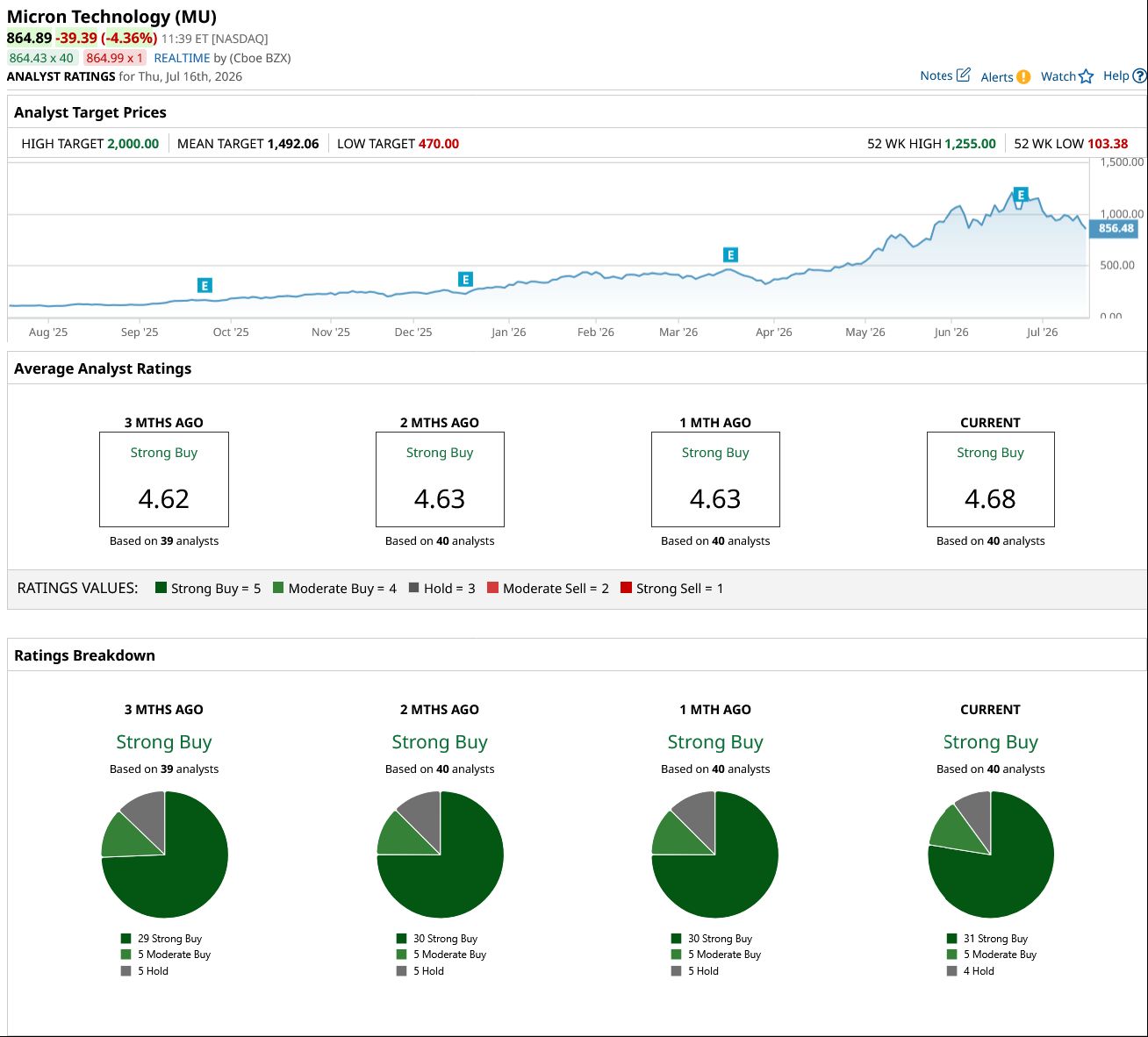

As MU appears undervalued, analysts maintain a “Strong Buy” consensus rating on the stock.

The Bottom Line

Micron continues to benefit from robust AI-driven memory demand, favorable pricing, and greater earnings visibility through its long-term supply agreements. At the same time, its valuation has become attractive relative to its growth outlook. Together, these factors indicate that now could be the best time to buy MU stock.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

You May Not Know ASE Technology, But the Chip Stock Has Nearly Quadrupled Michael Saylor’s Bitcoin Treasury Company Strategy Is Falling Apart RDW Stock Alert: What to Know as Redwire Scores $21.5 Million Follow-On Contract GME Stock Alert: What to Know as GameStop Teams Up With Uber Eats