Innodata Inc. INOD is demonstrating that customer diversification may be emerging as one of its most powerful competitive advantages. The AI data engineering company delivered a record first quarter in 2026, with revenues soaring 54% year over year to $90.1 million, while management raised its full-year growth outlook to approximately 40% or more.

What stands out most is that Innodata's growth is no longer dependent on a single major customer. CEO Jack Abuhoff emphasized that the company has spent several quarters preparing for broader customer diversification and those efforts are now translating into tangible results. Notably, revenues from Innodata’s other large technology customers surged 453% year over year in the first quarter, significantly outpacing growth from its largest account.

A key milestone is a newly announced engagement with a leading global technology company that could generate approximately $51 million in revenues during 2026. Just a year ago, Innodata had no revenues from this customer. Management now expects it to become the company’s second-largest customer, with opportunities for additional projects already under discussion.

The diversification story extends beyond individual customers. Innodata is expanding across multiple AI markets, including frontier AI labs, enterprise AI deployments and government-related projects. The company recently secured a global trust-and-safety partnership with a major hyperscaler, expanded relationships with cloud and commerce companies, and launched an AI agent evaluation platform that has already landed its first $1 million engagement.

This broader customer base reduces concentration risk while creating multiple growth avenues. Importantly, management noted that its largest customer is expected to represent a smaller percentage of total revenues in 2026, even as revenues from that account continue to rise. That combination of growing existing relationships and rapidly adding new ones is a strong indicator of a healthier and more resilient business model.

Given the accelerating adoption of AI and Innodata’s expanding roster of large technology customers, customer diversification appears to be evolving into one of the greatest strengths and a key driver of its long-term growth outlook.

How Do TaskUs and Concentrix Stack Up Against Innodata?

Among Innodata’s closest competitors are TaskUs, Inc. TASK and Concentrix Corporation CNXC, both of which provide AI-related data services, content moderation, trust and safety solutions, and digital operations support for large technology customers.

TaskUs has built a strong presence in AI data annotation, trust and safety, and customer support services. The company benefits from growing demand for AI training and moderation services, particularly from technology clients. However, its growth remains tied largely to expanding existing customer relationships, making customer concentration a key area which investors continue to monitor.

Concentrix offers a broad suite of digital transformation, AI training, data labeling and customer experience solutions. Its diversified client base across multiple industries provides stability, but AI-focused services account for only a portion of the overall business, reducing Concentrix's direct exposure to the rapidly expanding frontier AI market.

In contrast, Innodata is increasingly positioning itself as a specialized AI data engineering partner for hyperscalers and frontier AI labs. The company recently announced a new Big Tech engagement expected to generate approximately $51 million in 2026, while revenues from its other Big Tech customers surged 453% year over year. This expanding customer roster suggests that diversification is becoming a major growth driver and competitive advantage for Innodata.

INOD’s Price Performance, Valuation & Estimates

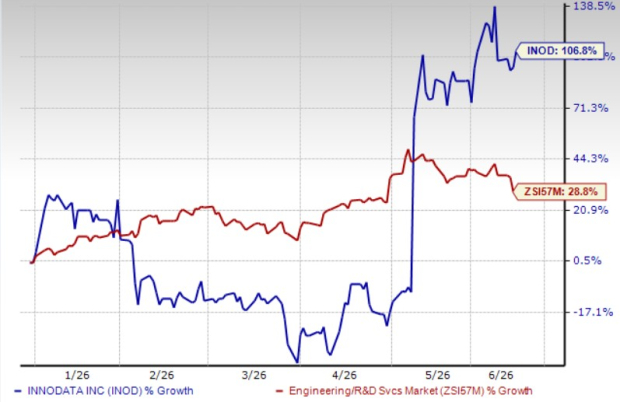

Year to date, INOD stock has surged 106.8%, outperforming the industry’s 28.8% growth.

Price Performance

Image Source: Zacks Investment Research

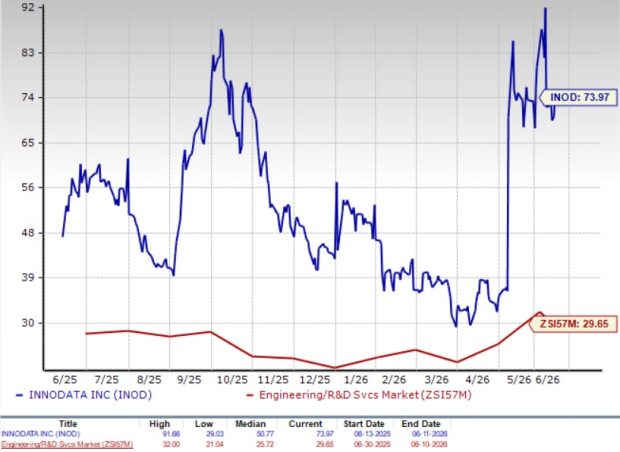

From a valuation standpoint, INOD trades at a forward price-to-earnings ratio of 73.97, much higher than the industry’s average of 29.65.

P/E (F12M)

Image Source: Zacks Investment Research

INOD’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to $1.14 and $1.78 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 23.9% and 55.9%, respectively.

Image Source: Zacks Investment Research

INOD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Innodata Inc (INOD): Free Stock Analysis Report

Concentrix Corporation (CNXC): Free Stock Analysis Report

TaskUs, Inc. (TASK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).