Crescent Energy Company CRGY presents a clearer value case after stronger operating execution and a firmer free cash flow outlook.

The stock is not without risk, especially given its debt profile and commodity exposure. Still, valuation, earnings momentum and shareholder-return capacity make the setup more constructive for investors willing to accept energy-sector volatility.

CRGY’s Valuation Looks Hard to Ignore

CRGY’s valuation remains one of the strongest parts of the investment case. The stock trades at 6.1 times trailing earnings and 4.4 times forward earnings, suggesting investors are not paying much for the company’s current earnings base.

The forward PEG ratio of 0.2 and price-to-sales ratio of 1 also point to an inexpensive profile. That combination may appeal more to value-focused investors than those looking for a pure growth story.

Crescent’s Earnings Picture Is Improving

Crescent’s earnings setup has improved as operating results have come in ahead of expectations. The company posted first-quarter 2026 EPS of 53 cents, representing a 35.9% surprise versus the consensus mark.

Crescent Energy Company Price and EPS Surprise

Crescent Energy Company price-eps-surprise | Crescent Energy Company Quote

Estimate momentum is also moving in the right direction. The fiscal-year earnings estimate has risen 0.6% over the past four weeks, while the stock carries an Earnings ESP of +4.70%, suggesting expectations may still have room to edge higher.

CRGY’s Free Cash Flow Supports Returns

The free cash flow outlook gives the stock a more tangible shareholder-return angle. Crescent expects roughly $1 billion of 2026 levered free cash flow at current commodity prices.

That cash flow supports the company’s quarterly dividend, share repurchases and selective acquisitions. It also gives investors a reason to look beyond near-term oil, natural gas and NGL price swings.

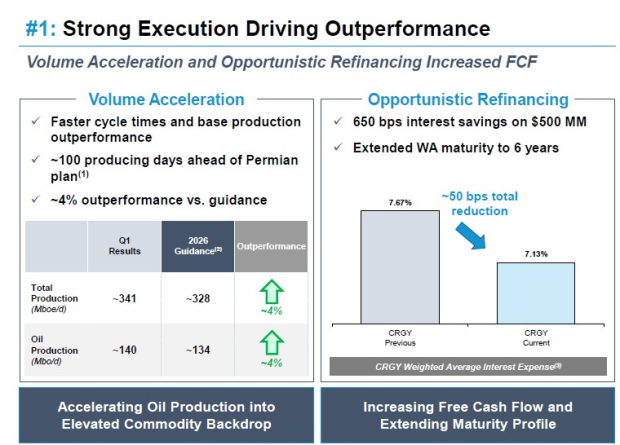

Crescent Has Execution Momentum

The investment case is not based only on cheap multiples. Crescent delivered record first-quarter production of 341 MBoe/d, supported by stronger operational execution and improved cycle times.

The Vital Energy integration is also progressing ahead of plan. Crescent has captured approximately $120 million in synergies, added lateral footage to its 2026 development plan and reduced well costs by more than $500,000 per well compared with the prior operator.

CRGY’s Debt Keeps the Call From Being Easy

Debt remains the main reason the bullish case is not straightforward. Crescent has a sizable debt load, and weaker oil, natural gas or NGL prices could pressure cash flow and limit financial flexibility.

That risk matters in a cyclical industry. Investors comparing CRGY with EOG Resources EOG or Diamondback Energy FANG may view those larger exploration and production names as cleaner ways to play U.S. shale, even if CRGY’s valuation screens more compelling.

Crescent’s Ratings Back a Value Thesis

The bottom line is that CRGY looks attractive for investors focused on valuation, free cash flow and improving execution, but it is not a low-risk, all-weather energy holding. The stock’s appeal rests on the market recognizing better cash generation while Crescent continues to manage leverage.

CRGY currently carries a Zacks Rank #1 (Strong Buy). It also has a Value Score of A, VGM Score of A, Momentum Score of B and Growth Score of D.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Those scores fit the investment setup. The Value Score of A and VGM Score of A reinforce the undervaluation argument, while the Momentum Score of B adds support to the near-term case. The Growth Score of D, however, underscores that the stock’s appeal is more about cash flow, valuation and execution than high-growth expansion.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EOG Resources, Inc. (EOG): Free Stock Analysis Report

Diamondback Energy, Inc. (FANG): Free Stock Analysis Report

Crescent Energy Company (CRGY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).