Royal Caribbean Cruises Ltd. RCL is working to protect 2026 earnings as higher fuel prices create a meaningful cost headwind. The company expects fuel rates to reduce adjusted earnings per share (EPS) by 62 cents for the remainder of the year, while lower expected earnings contribution from TUI Cruises adds another 12-cent drag. Full-year fuel expense is projected to be approximately $1.35 billion, with about 59% of the remaining 2026 fuel consumption hedged at rates meaningfully below market levels.

The earnings outlook is supported by continued cost discipline. RCL expects net cruise costs, excluding fuel, to be approximately flat for the full year, or 50 basis points better than its prior guidance. The company continues to focus on efficiency improvements, prudent expense management, technology, supply-chain initiatives and operating processes while maintaining the quality of the guest experience.

The second-quarter outlook provides an important checkpoint for the cost-control case. RCL expects net cruise costs, excluding fuel, to rise 4.6% to 5.1% in constant currency. The increase includes nearly 400 basis points of headwinds tied to additional dry dock days, year-over-year comparisons and higher crew travel costs caused by air travel disruptions and reduced airline capacity.

RCL’s ability to protect 2026 earnings will likely depend on whether it can sustain efficiency gains while delivering moderate capacity growth, yield growth and disciplined expense management. Cost controls may not fully neutralize the 62-cent fuel hit, but they can help limit the earnings impact and support the company’s ability to deliver double-digit adjusted EPS growth in 2026. For 2026, Royal Caribbean expects adjusted EPS of $17.10-$17.50.

How RCL Stacks Up to Competitors

Carnival Corporation & plc CCL is also facing fuel-related earnings pressure in 2026. Its guidance includes a 38-cent EPS headwind from higher fuel prices, which more than offsets an 11-cent operational improvement versus prior guidance. CCL expects full-year EPS of $2.21, with fuel assumptions based on Brent averaging $90 per barrel for the remainder of April and May, $85 per barrel in the third quarter and $80 per barrel in the fourth quarter. A 10% change in fuel cost per metric ton for the rest of the year would affect CCL’s bottom line by about $160 million, or 11 cents per share.

Norwegian Cruise Line Holdings Ltd. NCLH is facing fuel pressure alongside a weaker earnings outlook. The company expects fuel expense of approximately $800 million based on current spot prices, although fuel expense would be about 6% lower if rates were based on the forward curve. Reflecting softer-than-expected top-line performance and higher fuel costs, NCLH reduced its full-year adjusted EBITDA guidance to $2.48-$2.64 billion and adjusted EPS guidance to $1.45-$1.79.

RCL’s Price Performance, Valuation & Estimates

Shares of Royal Caribbean have gained 16.7% in the past year compared with the industry’s 8.8% growth.

RCL Stock’s One-Year Price Performance

Image Source: Zacks Investment Research

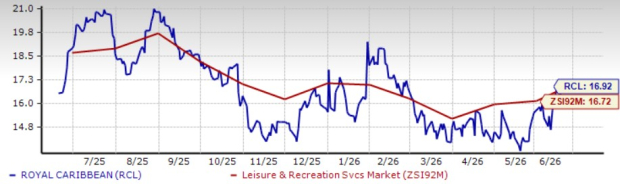

From a valuation standpoint, RCL trades at a forward price-to-earnings ratio of 16.92, above the industry’s average of 16.72.

RCL’s P/E Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

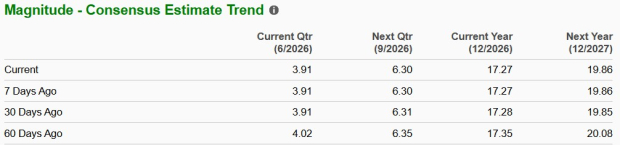

The Zacks Consensus Estimate for RCL’s 2026 earnings implies a year-over-year uptick of 10.4%. The EPS estimates for 2026 have declined in the past 60 days.

EPS Trend of RCL Stock

Image Source: Zacks Investment Research

RCL’s Zacks Rank

RCL stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Carnival Corporation (CCL): Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL): Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).