Perimeter Solutions, Inc. PRM has become a tougher call after a sharp rerating. The business case has improved, but the stock is no longer priced like an overlooked specialty name.

The question now is whether better earnings visibility, contract wins and operating momentum are enough to justify paying a richer valuation after the rally.

PRM’s Rally Has Reset the Valuation Debate

PRM shares have surged 46.6% over the past three months and 158.6% over the past year. That compares with gains of 6.5% and 5.5%, respectively, for the Zacks sub-industry over the same periods.

The valuation now reflects that move. PRM trades at 4.84X trailing 12-month book value, above the sub-industry’s 3.97X and the Zacks Basic Materials sector’s 4.03X, though below the S&P 500’s 7.94X.

The stock also sits near the upper end of its own five-year range of 0.39X to 5.12X, with a five-year median of 1.29X. Investors are no longer buying a deeply discounted recovery story.

Why Perimeter Still Has a Bull Case

The premium has support. Perimeter’s new five-year Defense Logistics Agency (DLA) suppressants framework carries a maximum value of $500 million, with the financial impact expected to begin late in 2026, ramp in 2027 and reach steady state in 2028 and beyond.

The renewed five-year CAL FIRE contract adds another layer of visibility, including a year-one price step-up and annual escalators. Service revenues of $108.3 million in 2025, mostly fixed each year, also help reduce dependence on wildfire-driven product volumes.

Liquidity remains another point in PRM’s favor. The company ended the first quarter with about $92 million in cash, a $200 million undrawn revolver and no near-term debt maturities, giving it room to fund capacity projects and acquisitions.

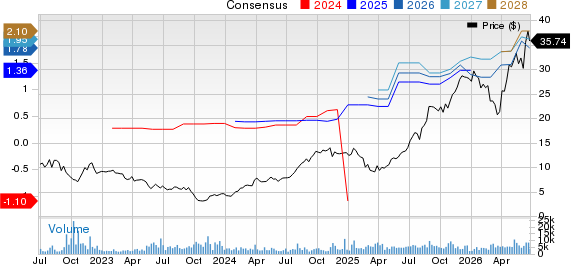

Perimeter Solutions, SA Price and Consensus

Perimeter Solutions, SA price-consensus-chart | Perimeter Solutions, SA Quote

What Could Limit PRM’s Upside From Here

The caution case starts with Sauget. Operational instability at the Flexsys-operated Sauget, IL facility caused substantial unplanned downtime in the first quarter and remains a near-term risk to Specialty Products revenue conversion and margins.

The DLA contract is also more of a multi-year story than an immediate 2026 catalyst. Management is investing in Green Bay capacity, staffing and supply-chain capabilities before the revenue contribution fully layers in.

Wildfire volatility has not disappeared either. North American retardant volumes were lower year over year in the first quarter due to difficult comparisons with major Southern California fires in the prior-year period.

Fixed obligations matter as well. PRM’s long-term framework assumes about $75 million in annual interest expense, and the Founders Advisory Agreement creates additional cash-flow and dilution considerations.

Perimeter’s Latest Quarter Strengthens the Case

The latest results explain why the market has rewarded PRM. First-quarter 2026 revenues rose 74% year over year to $125.1 million, while adjusted EBITDA jumped 128% to $41.2 million.

Margins improved as adjusted EBITDA margin expanded to 33% from 25% a year earlier. Fire Safety adjusted EBITDA rose 85%, while Specialty Products adjusted EBITDA climbed 181%.

Adjusted earnings came in at 6 cents per share, beating the Zacks Consensus Estimate of 2 cents. Revenues also topped the consensus mark of $110 million.

RPM International Inc. RPM and Element Solutions Inc. ESI offer useful specialty-chemicals reference points. PRM’s debate, however, is more directly tied to contract visibility, wildfire-service revenue and execution in newer Specialty Products assets.

How PRM’s Signals Fit a Buy-or-Wait Decision

The bottom line is that PRM has a better business setup than it did before the rally, but the stock price already reflects a lot of that improvement. Contract wins, fixed service revenues and acquisitions support the bull case, while valuation and execution risks argue for selectivity.

PRM currently carries a Zacks Rank #1 (Strong Buy), which points to a favorable near-term earnings estimate backdrop. That is a meaningful positive for investors focused on the next one to three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Style Scores are less supportive. PRM has a VGM Score of F, Value Score of F, Growth Score of C and Momentum Score of F. Since stronger Style Scores are generally preferred when paired with top-ranked stocks, PRM’s weak value and momentum signals suggest investors may want to be disciplined on entry price after the stock’s steep advance.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Perimeter Solutions, SA (PRM): Free Stock Analysis Report

Element Solutions Inc. (ESI): Free Stock Analysis Report

RPM International Inc. (RPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).