The Boston Beer Company SAM narrowed its 2026 volume outlook after reporting weaker-than-expected first-quarter results, reflecting persistent softness across parts of its brand portfolio and an uncertain consumer environment. While management highlighted encouraging signs of stabilization in the broader beer and ready-to-drink (RTD) categories, the company acknowledged that demand recovery has been slower than anticipated for some of its largest brands. The revised guidance underscores Boston Beer’s cautious stance as it heads into the critical summer selling season.

Boston Beer now expects 2026 shipment and depletion volumes to decline in the low-single-digit to mid-single-digit range compared with its earlier forecast of flat to down mid-single digits. The revision follows a 4% decline in first-quarter depletions and a 6.9% drop in shipments, as the company continued to reduce distributor inventory levels and cycled last year's innovation-driven inventory build. Management noted that although industry trends have improved modestly, SAM's own portfolio has yet to fully participate in that recovery, primarily because Truly continues to lose market share and Samuel Adams and Hard Mountain Dew remain under pressure.

Management also pointed to several macroeconomic challenges that influenced its more conservative outlook. Consumers continue to face tighter household budgets, while spending among Hispanic consumers — a key demographic for several of Boston Beer’s brands — remains pressured. In addition, evolving geopolitical developments, commodity inflation and tariff-related costs are creating an uncertain operating backdrop. Although the broader beer and RTD market has shown signs of stabilization, management believes these external factors could continue to weigh on consumer demand throughout the remainder of 2026.

Despite trimming its volume guidance, Boston Beer remains optimistic about improving execution during the peak summer season. The company expects stronger contributions from fast-growing Sun Cruiser, sequential improvement in Twisted Tea, continued growth in Angry Orchard and Dogfish Head, and expanded marketing initiatives tied to the FIFA World Cup and America's 250th anniversary celebrations. Coupled with ongoing productivity initiatives and gross-margin expansion efforts, these strategic investments could help offset volume headwinds. Investors will likely monitor whether stronger seasonal demand and innovation can translate into improved shipment trends and restore confidence in Boston Beer's long-term growth trajectory.

SAM’s Zacks Rank & Share Price Performance

Shares of this Zacks Rank #4 (Sell) company have lost 7.3% in the past six months, underperforming the Zacks Beverages - Alcohol industry’s 5.4% gain and the broader Consumer Staples sector's 17.4% rise.

SAM Stock's Six-Month Performance

Image Source: Zacks Investment Research

Is SAM Stock a Value Play?

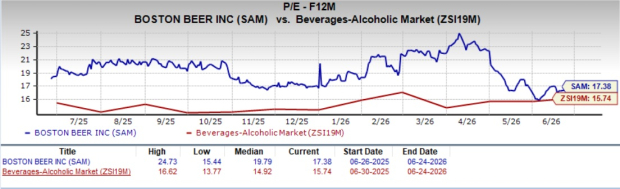

Boston Beer’s shares are currently trading at a forward 12-month price-to-earnings (P/E) multiple of 17.38X, which represents a meaningful premium to the industry average of 15.74X, reflecting investor confidence in the company’s margin expansion, brand portfolio strength and long-term growth potential despite near-term volume pressures.

SAM P/E Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Stocks to Consider

Fomento Economico Mexicano FMX, alias FEMSA, operates across retail, beverages, digital, health, fuel, logistics and distribution, anchored by OXXO and Coca-Cola FEMSA. FEMSA currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FEMSA’s 2026 sales and earnings indicates growth of 17.5% and 115.3%, respectively. The company has delivered a trailing four-quarter negative earnings surprise of 16.99%, on average.

The Vita Coco Company Inc. COCO is a beverage company that develops, markets and distributes coconut water, plant-based drinks, protein beverages and private-label products across global retail and foodservice channels. COCO currently flaunts a Zacks Rank #1.

The Zacks Consensus Estimate for Vita Coco's current fiscal-year sales and earnings indicates growth of 21.4% and 47.9%, respectively. The company has delivered a trailing four-quarter earnings surprise of 11.7%, on average.

Ambev S.A. ABEV engages in the production, distribution and sale of beer, draft beer, soft drinks, malt and food, and other beverages. ABEV currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for ABEV’s current fiscal-year sales and earnings indicates growth of 19.2% and 16.7%, respectively.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Boston Beer Company, Inc. (SAM): Free Stock Analysis Report

Vita Coco Company, Inc. (COCO): Free Stock Analysis Report

Fomento Economico Mexicano S.A.B. de C.V. (FMX): Free Stock Analysis Report

Ambev S.A. (ABEV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).