Commercial Metals Company CMC used its third-quarter fiscal 2026 call to argue that reported strength still understated the business. Management pointed to temporary outages, weather disruptions and scrap-cost pressure that held back an even better quarter.

The more important message for investors was forward-looking. Executives said those issues have started to reverse, while backlog, pricing and integration trends support a stronger fiscal fourth quarter.

CMC Says the Quarter Did Not Show Full Potential

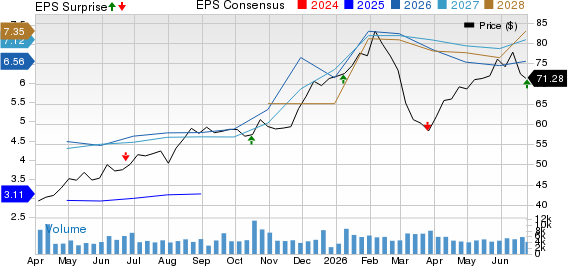

Commercial Metals reported adjusted earnings per share of $1.73, which beat the Zacks Consensus Estimate of $1.60, delivering a surprise of 8.1%. Third-quarter revenues were $2.48 billion, which also surpassed the Zacks Consensus Estimate of $2.37 billion by 4.9%.

Commercial Metals Company Price, Consensus and EPS Surprise

Commercial Metals Company price-consensus-eps-surprise-chart | Commercial Metals Company Quote

President and CEO Peter Matt said the quarter reflected solid execution against the company’s strategic plan, but he stressed that results were dampened by temporary issues rather than a change in underlying demand. He tied the longer-term story to structurally higher margins, lower earnings volatility and a broader construction solutions footprint.

That framing mattered because management was not pitching the quarter as a peak. Instead, it positioned third-quarter performance as a transition point, with improving steel margins, better operating reliability and acquired precast assets beginning to add meaningfully to the earnings mix.

Commercial Metals Sees a Rebound in North America

The North America Steel Group remained the central talking point. Adjusted EBITDA in the segment rose 41% year over year to $253.5 million, but it slipped sequentially as planned maintenance outages at seven of 10 mills, poor weather, and a lag between rising scrap costs and price increases weighed on results.

In the Q&A, a Goldman Sachs analyst pressed management on the bridge to a better fourth quarter. CFO Paul Lawrence said outages cost about $20 million and volume-related effects from weather, inventory tightness and commercial discipline cost roughly another $10 million. He added that those issues should reverse in the current quarter.

Matt also sounded firm on pricing. He said the recently announced steel price increases are taking hold and that CMC is not chasing discounting in the market. The company expects higher realized prices and improved metal margins in the fourth quarter, supported by healthy demand and major project activity.

CMC’s Precast Bet Is Moving to Center Stage

Commercial Metals’ Construction Solutions Group delivered one of the clearest strategic signals on the call. Net sales nearly doubled year over year to $394.6 million, and adjusted EBITDA increased 138% to $97.4 million, helped by $175.7 million of revenues and $52.9 million of EBITDA from the recently acquired precast businesses.

Management acknowledged that precast volumes were light in the quarter because shipment timing slipped by about two weeks and wet weather in the Southeast delayed deliveries. Still, Matt said the backlog reached a record level, and project releases have started to normalize heading into the fiscal fourth quarter.

That explains why CMC maintained its fiscal 2026 precast EBITDA outlook of $165 million to $175 million despite the third-quarter shortfall. Management also reiterated that the acquisitions are on plan operationally and commercially, with early lead sharing and network benefits already emerging.

Commercial Metals Finds More Than One Tailwind

CMC’s other margin lever remains its Transform, Advance, Grow program. Matt said the initiative is tracking well ahead of its targeted $150 million run-rate annualized benefit for fiscal 2026, with most gains so far coming from operational improvements such as scrap optimization, yield and logistics.

He used the Q&A to highlight a second phase of opportunity in commercial excellence. That includes cutting pricing leakage, deploying better tools and using the broader steel and precast platform to get involved earlier on large projects where CMC can influence design and capture more value.

Europe added another support point. The Europe Steel Group posted adjusted EBITDA of $34.7 million, aided by a $20.4 million CO2 credit and better market conditions. Management said CBAM, tighter EU safeguards and improving pricing are creating a more constructive supply-demand setup there.

CMC Nears a Cash Flow Inflection Point

Capital allocation also drew scrutiny. Net leverage adjusted for acquisitions ended the quarter at 2.1x, and management said it remains confident in reaching below 2x by mid-2027 or sooner. Liquidity stood near $1.8 billion.

Matt said 2x leverage is the threshold that would reopen both larger shareholder returns and new growth opportunities. At the same time, he made clear that CMC wants more progress in integrating the two precast acquisitions before considering another sizable deal.

Lawrence added that fiscal 2027 capital spending should drop sharply as the West Virginia micro mill nears completion, setting up a stronger free cash flow profile. Management does not expect more mill investments, with future organic spending aimed at smaller, higher-return projects.

Commercial Metals Leaves With an Assertive Tone

The clearest read-through from the call was management’s confidence in the near-term setup. CMC expects a meaningful sequential increase in fourth-quarter core EBITDA, including about a $40 million benefit in North America from the end of outage impacts and from better volume and margins, plus mid-teens EBITDA growth in Construction Solutions.

Analyst questions focused on supply additions in rebar, imports, precast execution and Europe. Matt’s answers were notably direct, especially on market discipline, where he said CMC will prioritize value over volume and use trade remedies to defend the domestic market.

Taken together, management presented a company leaning into a more diversified earnings model. The tone was not built around a single quarter’s beat, but around improving margins, more stable end markets and a portfolio that management believes can generate stronger cash and lower volatility over time.

Zacks Signals Still Call for Balance

CMC carries a Zacks Rank #3 (Hold), alongside a Value Score of B, Growth Score of A, Momentum Score of A and VGM Score of A. In Zacks terms, the strongest combinations generally pair a Zacks Rank #1 (Strong Buy) or 2 (Buy) with Style Scores of A or B, while a Zacks Rank #3 can still be held when the score profile remains favorable. You can see the complete list of today’s Zacks #1 Rank stocks here.

The current mix points to attractive style characteristics across value, growth and momentum, but the Zacks Rank remains the primary signal in the framework. That rank can change as earnings estimate revisions move after the quarter, so the post-report revision trend remains the key factor to watch.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Commercial Metals Company (CMC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).