Flex Ltd.’s FLEX growth is being driven by expanding business from hyperscalers and AI infrastructure customers, supported by multiyear engagements spanning power infrastructure, thermal systems and complex hardware manufacturing. The company recently secured substantial incremental business from several hyperscaler and data center customers, including Google, with these projects already moving into the capital deployment phase. To support this demand, Flex is increasing investments throughout fiscal 2027 to expand manufacturing capacity across its global footprint, while expecting capital spending to normalize in fiscal 2028.

The company stated that the new awards extend beyond a single customer and include multiple hyperscalers, neocloud providers, colocation operators and utility customers. These contracts cover a broad range of offerings, including power infrastructure, cooling, compute integration and distributed power solutions. Flex noted that it is expanding factory capacity to fulfill these multiyear commitments and expects Cloud and Power Infrastructure (CPI) revenue to grow 65-75% in fiscal 2027, followed by growth of more than 80% in fiscal 2028. It also indicated that several of these programs are expected to continue expanding into fiscal 2029.

Flex further highlighted that its integrated portfolio across power, thermal management and compute integration supports customers seeking end-to-end infrastructure solutions. The company also strengthened its power portfolio with the acquisition of Electrical Power Products (EP2), enhancing its capabilities in grid modernization and electrification.

Flex expects its momentum to continue with fiscal 2027 revenue projected between $32.3 billion and $33.8 billion, representing 18% growth at the midpoint, while adjusted EPS is expected to increase 32% at the midpoint. The CPI business alone is forecast to deliver revenue growth of 65% to 75% for fiscal 2027, followed by more than 80% growth in fiscal 2028, supported by multiyear contracts, expanding AI infrastructure demand and investments that are expected to drive further margin expansion. Management also expects capital expenditures to normalize after fiscal 2027 while maintaining strong growth and cash generation.

Taking a Look at FLEX’s Competitors

Jabil Inc. JBL continues to benefit from sustained demand across AI data center infrastructure, capital equipment and warehouse automation, while improving trends in the automotive and select consumer markets are broadening its growth profile. The company's diversified end-market strategy, global manufacturing footprint and expanding AI capabilities support long-term scalability and operating efficiency. For the fourth quarter of fiscal 2026, management projects revenues between $9.2 billion and $10 billion. For fiscal 2026, the company expects revenues of approximately $35 billion, a core operating margin of about 5.8%, core earnings per share of roughly $12.70 and adjusted free cash flow exceeding $1.4 billion.

Sanmina Corporation SANM is benefiting from rising demand for cloud and AI infrastructure programs, supported by its vertically integrated manufacturing model and broad global footprint. The company continues to deepen customer relationships through end-to-end design, production and supply chain capabilities, while the ZT Systems acquisition expands its exposure to higher-growth accelerated compute markets. Its strong cash flow strengthens financial flexibility, supporting debt reduction, strategic investments and capital returns. A diversified presence across industrial, medical, defense and automotive markets provides stability against weaker areas of demand. For the third quarter of fiscal 2026, the company guided revenues of $3.2-$3.5 billion. For fiscal 2026, Sanmina expects revenues of $13.7-$14.3 billion.

Flex Price Performance, Valuation and Estimates

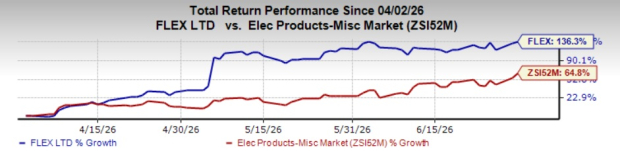

Shares of FLEX have surged 136.3% in the past three months against the Electronics - Miscellaneous Products industry’s growth of 64.8%.

Image Source: Zacks Investment Research

FLEX trades at a forward 12-month price-to-earnings (P/E) ratio of 35.2, below the industry’s 42.43.

Image Source: Zacks Investment Research

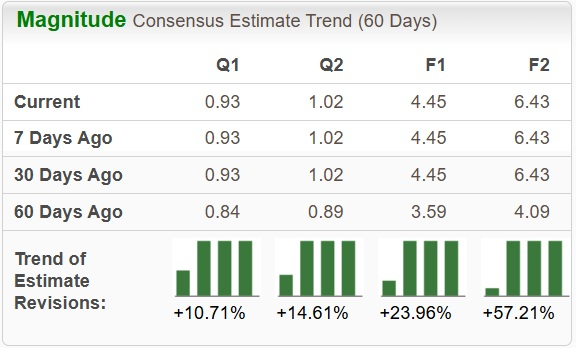

The Zacks Consensus Estimate for FLEX earnings for fiscal 2026 has been revised upward over the past 60 days.

Image Source: Zacks Investment Research

FLEX currently has a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Jabil, Inc. (JBL): Free Stock Analysis Report

Flex Ltd. (FLEX): Free Stock Analysis Report

Sanmina Corporation (SANM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).