Merit Medical Systems, Inc. MMSI is well-poised for growth in the coming quarters, courtesy of its strong product portfolio. The optimism, led by a solid product performance and its continued spending on research and development, is expected to contribute further. However, tariffs and trade policy headwinds, and China macro pressure persist.

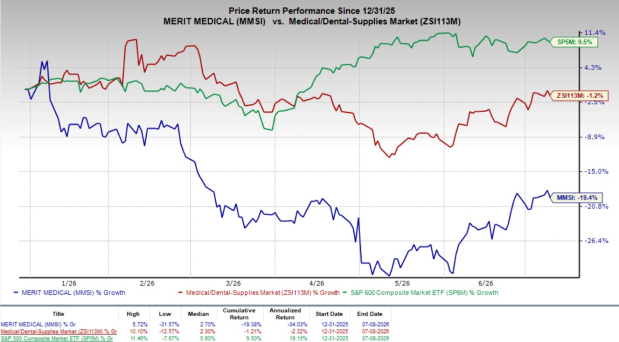

This Zacks Rank #2 (Buy) company’s shares have declined 19.4% in the year-to-date period compared with the industry’s 1.2% drop. However, the S&P 500 has risen 9.5% during the same time frame.

The renowned medical device provider has a market capitalization of $4.30 billion. The company projects 8.9% growth for the next five years and expects to maintain its strong performance going forward. It delivered an average earnings surprise of 12.5% for the past four quarters.

Image Source: Zacks Investment Research

Let’s delve deeper.

MMSI’s Growth Drivers

Strong Product Portfolio and Strategic Acquisitions: Merit Medical continues to expand its presence across interventional cardiology, radiology, oncology, endoscopy and other minimally invasive procedure markets through a diversified product portfolio and disciplined acquisitions. During the first quarter of 2026, the company launched the Resilience Through-the-Scope Esophageal Stent, which management expects to support long-term growth in its endoscopy business. Merit Medical also acquired View Point Medical, adding the OneMark Detection Imaging System and Tissue Markers to complement its SCOUT platform. Management believes the acquisition expands the addressable procedure opportunity for its oncology business by roughly threefold while providing physicians with additional localization options. Earlier acquisitions, including Biolife and the C2 CryoBalloon technology, continue to strengthen the company's therapeutic portfolio and support long-term growth.

Innovation-Driven R&D: Merit Medical continues to invest in research and development to expand its product pipeline and strengthen its competitive position. The company has reorganized its R&D, marketing and commercial teams around eight product platforms, enabling faster product development and closer alignment with physician needs. Supported by approximately 2,200 patents and patent applications, Merit Medical follows a disciplined innovation strategy that prioritizes products with strong commercial potential and attractive returns, positioning the company for sustained long-term growth.

WRAPSODY Offers Long-Term Upside: Merit Medical's WRAPSODY Cell-Impermeable Endoprosthesis remains an important long-term growth opportunity within renal therapies. Clinical data continue to demonstrate superior long-term vessel patency compared with conventional angioplasty, supporting broader physician adoption. Management reaffirmed its commercial strategy and expects the product to generate approximately $7 million in revenues in the United States in 2026. While adoption remains in the early stages, continued physician education and expanding clinical evidence position WRAPSODY as a meaningful multi-year growth catalyst.

Key Challenges for MMSI Stock

Tariffs and Macroeconomic Uncertainty: Merit Medical continues to operate in an uncertain macroeconomic environment marked by evolving trade policies and geopolitical risks. During the first quarter earnings call, management highlighted tariffs as a significant headwind and expects them to remain a drag on profitability in 2026. While the company has implemented operational initiatives to offset part of the cost pressure, the ultimate impact remains uncertain as it depends on future tariff policies, retaliatory actions and legal developments. Geopolitical disruptions, including those affecting the Middle East, have created temporary shipping delays and higher freight-related costs. Although management described these challenges as manageable, prolonged macroeconomic uncertainty could pressure margins and weigh on earnings growth.

OEM and Pricing Headwinds: Merit Medical continues to face near-term pressure in its OEM business, which has experienced demand fluctuations due to inventory destocking, product line transfers and softer international demand, particularly in the Asia-Pacific region. Management expects these issues to be temporary and continues to view the OEM business as a mid- to high-single-digit grower over the long term. However, broader pricing pressure remains a challenge. The company continues to navigate China's volume-based procurement program, which has reduced pricing in recent years and is expected to remain a headwind in 2026. As Merit Medical expands its therapeutic portfolio through acquisitions and new product launches, sustaining growth will require continued innovation and disciplined execution.

Merit Medical Systems, Inc. Price

Merit Medical Systems, Inc. price | Merit Medical Systems, Inc. Quote

Estimate Trend

MMSI is witnessing a stable estimate revision trend for 2026. In the past 30 days, the Zacks Consensus Estimate for earnings per share (EPS) has remained stable at $4.07.

The Zacks Consensus Estimate for the company’s second-quarter 2026 revenues is pegged at $404.7 million, suggesting a 5.81% rise from the year-ago reported number. The consensus mark for EPS is pegged at 96 cents, implying a 4.9% decline from the prior-year reported figure.

Other Stocks to Consider

Some other top-ranked stocks from the broader medical space are Veracyte VCYT, West Pharmaceutical WST and Pacific Biosciences of California PACB.

Veracyte, currently sporting a Zacks Rank #1 (Strong Buy), has an estimated earnings growth rate of 5.1% for 2026. VCYT’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 45.9%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Veracyte’s shares have gained 33.3% against the industry’s 14.2% decline in the year-to-date period.

West Pharmaceutical, currently carrying a Zacks Rank #2, has an estimated long-term earnings growth rate of 13.9%. WST’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 19.4%.

West Pharmaceutical’s shares have gained 28.5% against the industry’s 1.2% decline in the year-to-date period.

Pacific Biosciences of California, currently carrying a Zacks Rank #2, has an estimated earnings growth rate of 22.6% for 2026. PACB’s earnings beat estimates in each of the trailing four quarters, the average surprise being 29.8%.

Pacific Biosciences’ shares have lost 19.8% compared with the industry’s 14.2% decline in the year-to-date period.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Merit Medical Systems, Inc. (MMSI): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

Pacific Biosciences of California, Inc. (PACB): Free Stock Analysis Report

Veracyte, Inc. (VCYT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).