Shares of ABM Industries ABM have had a decent run over the past three months. The stock has gained 12.6% against the industry's 1.5% drop. The Zacks S&P 500 composite rose 8.7% during the said time frame.

ABM has a Growth Score of B. This style score condenses key financial metrics to reflect a fair sense of the quality and sustainability of its growth.

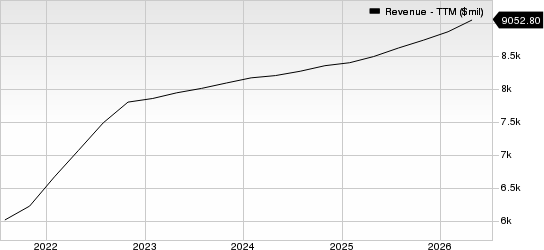

The company’s third-quarter fiscal 2026 earnings are expected to increase 23.2% year over year. Earnings for fiscal 2026 and fiscal 2027 are projected to rise 15.4% and 9.3%, respectively, year over year. Revenues are expected to increase 5.3% in fiscal 2026 and 3% in fiscal 2027.

Factors That Bode Well for ABM

ABM Industries, a leading provider of integrated facility solutions globally, benefits from growing demand across its broad range of services that support infrastructure functionality and operational efficiency. The services include janitorial, energy management, facilities engineering, electrical and lighting, landscape and turf care, heating, ventilation and air conditioning (HVAC) and mechanical, mission-critical and parking solutions across various sectors.

Recently, the company reported that its second-quarter fiscal 2026 revenues increased 8.4% year over year to a record $2.3 billion. It also gained a record $1.2 billion in first-half new sales bookings, highlighting continued success in expanding its customer base across key growth markets.

ABM’s multi-year, comprehensive strategic plan, ELEVATE, launched in 2021, has also significantly boosted its overall revenues by driving client value through transparent and efficient solutions, talent optimization, expanded data utilization and digital modernization. This initiative has enabled the company to generate revenues and net income with a compounded annual growth rate (CAGR) of 7% and 5%, respectively, from fiscal 2021 to fiscal 2025.

ABM Industries Revenues (TTM)

ABM Industries Incorporated revenue-ttm | ABM Industries Incorporated Quote

Strategic expansion into high-demand sectors like data centers through targeted acquisitions and investments has amplified ABM’s mission-critical offerings. The company continues to accelerate investment in energy infrastructure, battery storage, data centers and artificial intelligence infrastructure due to strong demand for data centers, battery energy storage systems and HVAC projects. ABM’s Manufacturing & Distribution segment growth was also driven by semiconductor industry investments and technology-sector contract wins. The recent WGNSTAR acquisition has enhanced ABM's capabilities within semiconductor fabrication environments and contributed meaningfully to financial results.

The company has demonstrated a strong commitment to its shareholders through consistent dividend payments and share repurchases. ABM paid dividends of $57.5 million, $56.5 million and $65.6 million while repurchasing shares worth $138.1 million, $56.1 million and $122.2 million in fiscal 2023, 2024 and 2025, respectively. This consistency underscores its dedication to creating long-term value for investors.

Key Risks to Watch

ABM Industries remains exposed to broad economic risks, with trade tariffs and changing government policies threatening to increase input expenses and delay key infrastructure projects. Shifts in spending allocations and trade uncertainties may reduce contract awards but elevate operational costs, dampening profit margins and growth potential.

Rising operating costs are squeezing profit margins and limiting short-term earnings growth. ABM’s total operating costs increased by 4.2% in fiscal 2023, 4.1% in fiscal 2024 and 4.7% in fiscal 2025. The company reported that its operating expenses rose 9.3% year over year during the second quarter of 2026.

ABM currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

A couple of better-ranked stocks in the broader Zacks Business Services sector are Veralto Corporation VLTO and Corpay, Inc. CPAY.

Veralto carries a Zacks Rank #2 (Buy) at present. It has a long-term earnings growth expectation of 8.4%. VLTO delivered a trailing four-quarter earnings surprise of 4.9%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Corpay also holds a Zacks Rank of 2 at present. It has a long-term earnings growth expectation of 14.3%. CPAY's earnings beat estimates in three of the last four reported quarters and matched once, with the surprise being 2%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ABM Industries Incorporated (ABM): Free Stock Analysis Report

Veralto Corporation (VLTO): Free Stock Analysis Report

Corpay, Inc. (CPAY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).