The demand for mission-critical industrial, government, healthcare and data center projects has ramped up across the United States over the past few years and is currently reaching its peak, given the public funding growth and market trends. Firms like EMCOR Group, Inc. EME and Jacobs Solutions, Inc. J sit at the juncture and are currently gaining from these market tailwinds.

EMCOR offers mechanical and electrical construction, industrial and energy infrastructure services for a diverse range of businesses, serving commercial, industrial, utility and institutional clients in the United States. Meanwhile, Jacobs offers professional, technical and construction services to industrial, commercial and governmental clients.

Let’s closely compare the fundamentals of the two infrastructure stocks to determine which one is a better investment now.

The Case for EMCOR Stock

Federal and state investments in water infrastructure, transportation, healthcare modernization, institutional facilities and energy-related projects are creating a healthy pipeline of opportunities for EMCOR. At the same time, AI-driven data center expansion and broader digital transformation continue to fuel commercial construction demand. Owing to these robust trends, EMCOR’s record remaining performance obligations (RPOs) reached $15.62 billion as of March 31, 2026, up 32.9% year over year and nearly 18% sequentially, providing exceptional visibility into future revenue generation. RPOs in the construction segments highlighted contributions of $8.56 billion in U.S. mechanical construction and $5.61 billion in U.S. electrical construction, with additional contributions from building services.

Management emphasized that it continues to see no signs of slowing demand as customers expand data center capacity and adopt advanced liquid cooling technologies. Reflecting this confidence, EME raised its full-year 2026 revenue guidance to $18.5-$19.25 billion from $17.75-$18.5 billion and increased its EPS guidance to $28.25-$29.75 from $27.25-$29.25 expected earlier. Supported by disciplined project selection, execution capabilities and broad market diversification, the company appears well-positioned to capitalize on multi-year infrastructure investment trends.

Meanwhile, strategic acquisitions remain an important pillar of EMCOR's long-term growth strategy, complementing its strong organic expansion. The company's acquisition of Miller Electric has strengthened its electrical construction capabilities, expanded its geographic presence and increased exposure to attractive end markets. Rather than pursuing scale for its own sake, EMCOR prioritizes disciplined capital deployment and integration, preserving its operational culture while creating cross-selling opportunities across its construction and services platforms.

EME ended the first quarter of 2026 with approximately $916 million in cash and about $1.25 billion in working capital, supporting organic investments, strategic acquisitions and operational needs. Management expects full-year 2026 operating cash flow to remain broadly in line with net income, reflecting the underlying strength of the business despite quarterly working-capital fluctuations.

The Case for Jacobs Stock

Jacobs continues to benefit from long-term structural demand across data centers, semiconductors, water infrastructure, transportation and energy & power, reporting more than 100% year-over-year growth in its data center business, supported by accelerating AI investments and strong hyperscaler demand. PA Consulting acquisition is further enhancing growth through advisory, digital transformation and national security opportunities, creating meaningful cross-selling potential. Management has already increased expected annual cost synergies from the acquisition to more than $20 million within 24 months.

These demand drivers helped Jacobs deliver a record backlog of $27 billion, up 22% year over year, with a strong trailing 12-month book-to-bill ratio of 1.4x, providing excellent revenue visibility and supporting confidence in sustained long-term growth. The company is executing a strategy focused on expanding higher-margin consulting, digital and lifecycle solutions while strengthening its leadership in resilient infrastructure markets. Jacobs continues to invest in AI-enabled engineering solutions, including digital twins developed with NVIDIA Omniverse, reinforcing its competitive positioning in rapidly expanding AI infrastructure, advanced manufacturing and mission-critical facilities.

Besides, Jacobs continues to strengthen its global footprint through expanding operations across North America, Europe and the United Kingdom. Recent project wins with Ofwat, Scottish Hydro Electric Transmission and global hyperscale data center customers further demonstrate growing international opportunities. With diversified end markets, strong bookings, improving margins and an upgraded fiscal 2026 outlook, Jacobs appears well-positioned to capture expanding global infrastructure and digital transformation spending, even though execution risks and macroeconomic uncertainties pose a near-term threat.

Notably, Jacobs maintains a balanced capital allocation strategy that simultaneously funds long-term growth while delivering substantial shareholder returns. It repurchased $472 million of shares during the first half of fiscal 2026 and increased its quarterly dividend by 12.5%, reflecting confidence in future cash generation.

Stock Performance & Valuation

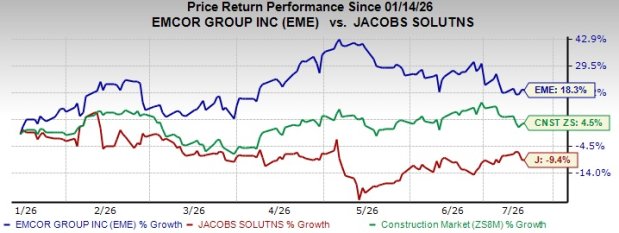

As witnessed from the chart below, in the past six months, EMCOR’s share price performance has been above Jacobs’ and the broader Construction sector.

Image Source: Zacks Investment Research

Considering valuation, over the last five years, EMCOR has been trading above Jacobs on a forward 12-month price-to-earnings (P/E) ratio basis.

Image Source: Zacks Investment Research

Overall, from these technical indicators, it can be deduced that EME stock offers an increasing growth trend but with a premium valuation, while J stock offers a declining growth trend with a discounted valuation.

Comparing EPS Estimate Trends: EME vs. J

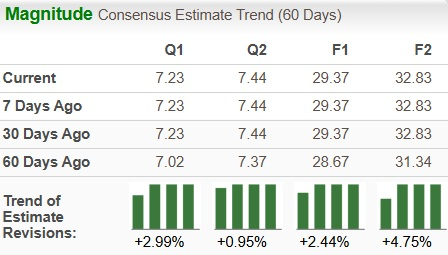

The Zacks Consensus Estimate for EME’s 2026 and 2027 earnings has moved upward in the past 60 days. The revised estimates for 2026 and 2027 imply year-over-year growth of 13.5% and 11.8%, respectively.

EME's EPS Trend

Image Source: Zacks Investment Research

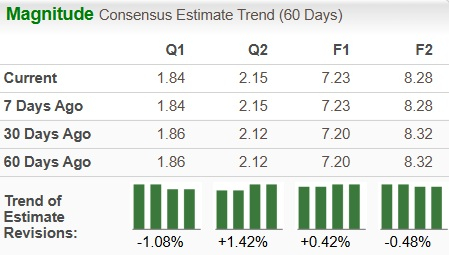

The Zacks Consensus Estimate for J’s fiscal 2026 earnings has increased in the past 30 days, while the same for fiscal 2027 has edged down during the same time frame. The revised estimates for fiscal 2026 and fiscal 2027 imply year-over-year growth of 18.1% and 14.5%, respectively.

J's EPS Trend

Image Source: Zacks Investment Research

Return on Equity (ROE) of EME & J Stocks

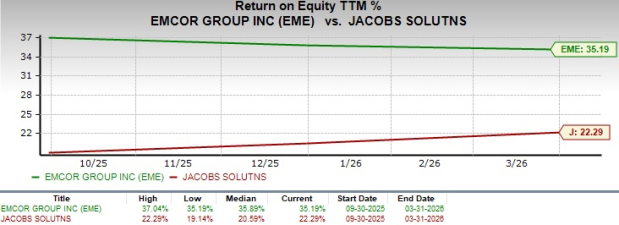

EMCOR’s trailing 12-month ROE of 35.19% significantly exceeds Jacobs’ average, underscoring its efficiency in generating shareholder returns.

Image Source: Zacks Investment Research

Investment Decision: Should Investors Choose EME Stock or J Stock?

EMCOR combines record remaining performance obligations, raised 2026 revenue and earnings guidance, disciplined acquisitions and broad exposure across mechanical, electrical, healthcare, institutional and industrial construction, providing exceptional earnings visibility. Its superior execution and industry-leading 35.2% ROE further strengthen the investment case. Although the stock trades at a premium, its recent price momentum, upward earnings estimate revisions and improving fundamentals justify the higher valuation.

Jacobs remains an attractive long-term infrastructure play, supported by record backlog, rapid data center growth, AI-enabled engineering capabilities and expanding consulting opportunities through PA Consulting. However, mixed earnings estimate revisions, greater exposure to consulting execution and slower share price momentum make its near-term outlook comparatively less compelling.

With a current Zacks Rank #1 (Strong Buy) compared with J stock’s Zacks Rank #2 (Buy), stronger technical indicators and more consistent operational momentum, EME stock stands out as the better investment choice for investors looking to capitalize on the current infrastructure and AI-driven construction cycle. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Jacobs Solutions Inc. (J): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).