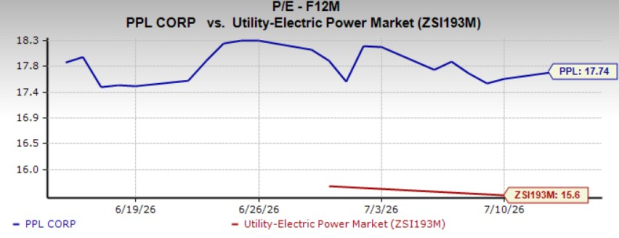

PPL Corporation’s PPL shares are trading at a premium to the Zacks Utility -Electric Power industry. Its 12-month forward price-to-earnings of 17.74X is higher than the industry average of 15.6X and the broader Zacks Utility sector’s 15.45X.

PPL Corporation is well-positioned to capitalize on increasing electricity demand from data centers, particularly in Pennsylvania and Kentucky, where the rapid expansion of these energy-intensive facilities is driving long-term load growth.

However, PPL faces rising competition in the transmission business, which could pressure operations, while unforeseen operational disruptions may adversely affect its financial performance.

PPL Trading at a Premium Valuation

Image Source: Zacks Investment Research

Other operators in this space, Duke Energy DUK and Ameren Corporation AEE, are trading at P/EF12M of 18.28 and 20.3, respectively, a premium to the industry.

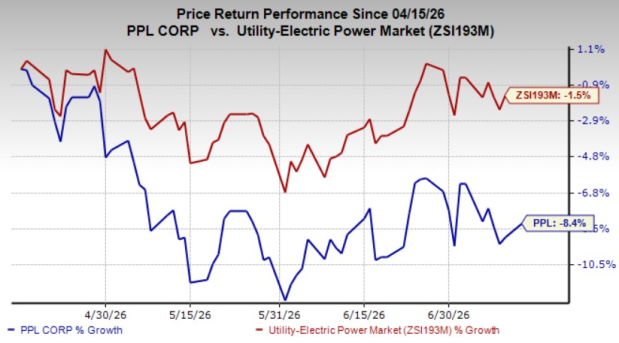

PPL’s shares have lost 8.4% in the past three months, wider than the Zacks Utility-Electric Power industry’s decrease of 1.5%.

Price Performance (Three Months)

Image Source: Zacks Investment Research

Despite trading at a premium valuation, PPL Corporation's recent share price weakness may have investors wondering whether now is an opportune time to buy. Let’s explore the key factors that will help determine if the stock merits consideration at current levels.

Factors Supporting PPL’s Earnings Growth

PPL continues to benefit from economic expansion and robust data center demand across its service territories. In Pennsylvania, advanced-stage data center demand has increased to nearly 28.3 gigawatts (“GW”) from 25.2 GW, while Kentucky's economic development pipeline now indicates potential load growth of 12.9 GW through 2032, up from the earlier estimate of 8.5 GW.

To capitalize on these opportunities, PPL plans to invest approximately $23 billion between 2026 and 2029, supporting an average annual rate base growth of about 10.3% through 2029. The company's investments in generation, transmission and distribution infrastructure, coupled with ongoing grid modernization initiatives, are enhancing system reliability and reducing customer outages.

A key advantage is that more than 60% of PPL's capital investment program qualifies for contemporaneous recovery, mitigating the effects of regulatory lag on earnings. This framework enables the company to recover capital investments more quickly, strengthening cash flows and supporting the timely execution of its long-term growth strategy.

Additionally, it remains committed to disciplined cost management, creating value for both the company and customers. Since 2021, PPL has reduced total operating expenses by $170 million as of 2025. Continued focus on cost-control initiatives is expected to support margin expansion, improve profitability and reinforce the company's long-term financial performance.

Headwinds for PPL Stock

PPL continues to encounter competition in Pennsylvania's transmission market. Moreover, adverse weather conditions, cybersecurity incidents, equipment outages and fuel supply interruptions could disrupt operations and pressure the company's earnings and profitability.

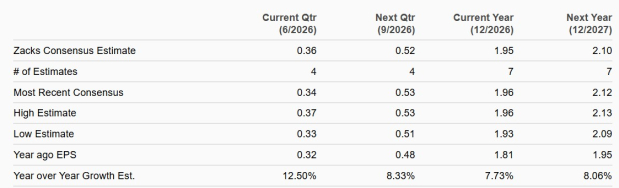

PPL Stock’s Earnings Estimate Moving Up

PPL expects 2026 earnings to be in the range of $1.90-$1.98 per share. The Zacks Consensus Estimate for PPL’s 2026 and 2027 earnings per share indicates year-over-year growth of 7.73% and 8.06%, respectively.

Image Source: Zacks Investment Research

The same for DUK’s 2026 and 2027 earnings per share indicates year-over-year growth of 6.34% and 6.41%, respectively.

PPL Raises Shareholders' Value

PPL has a long history of returning value to shareholders through regular dividend payments and expects to increase its annual dividend by 4-6% over the long term, subject to board approval. The company currently pays a quarterly dividend of 28.5 cents per share, translating to an annualized dividend of $1.14. With a dividend yield of 3.19%, PPL offers a more attractive income stream than the S&P 500's average yield of 1.35%.

PPL has raised dividends for its shareholders four times in the past five years. Check PPL’s dividend history here.

Ameren also distributes dividends to its shareholders. The current annual dividend rate of Ameren is $3 per share, reflecting a dividend yield of 2.66%.

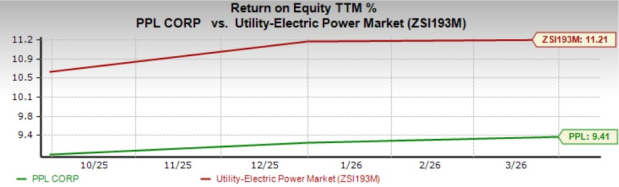

PPL’s Return Is Lower Than the Industry

Return on equity (“ROE”) is a financial ratio that measures how well a company uses its shareholders’ equity to generate profits. The current ROE of the company indicates that it is using shareholders’ funds more efficiently than peers.

PPL’s trailing 12-month ROE is 9.41%, lower than the industry average of 11.21%.

Image Source: Zacks Investment Research

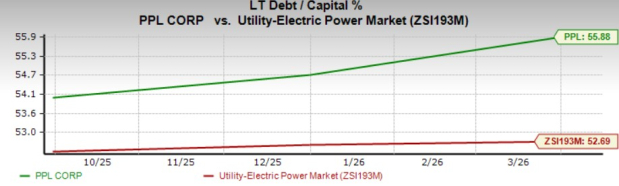

PPL’s Debt to Capital

Utility operations are capital-intensive and companies in this sector often need to borrow to fund long-term projects when internal resources are insufficient. The company is also borrowing funds to meet its capital requirements.

PPL’s current debt to capital is 55.88% compared with its industry average of 52.69%. This shows the company is utilizing lower debts than peers to run its operations.

Image Source: Zacks Investment Research

Summing Up

PPL is benefiting from accelerating data center-driven electricity demand and timely rate recovery mechanisms, which enable it to efficiently finance the long-term growth initiatives. The company is also enhancing grid reliability through significant investments in infrastructure, IT modernization and an expanded $23 billion capital investment plan, positioning it to meet rising electricity demand across the service territories.

However, PPL is currently trading at a premium valuation, generates returns below the industry average and carries a higher debt burden than many of its peers. Given these factors, existing investors may continue holding this Zacks Rank #3 (Hold) stock, while prospective investors should wait for a more attractive entry point before initiating a position in PPL.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PPL Corporation (PPL): Free Stock Analysis Report

Ameren Corporation (AEE): Free Stock Analysis Report

Duke Energy Corporation (DUK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).