The boom in artificial intelligence (AI) has led to persistent demand for NVIDIA Corporation’s NVDA state-of-the-art AI hardware, including graphics processing units and Blackwell chips. That demand propelled NVIDIA to become the world’s most valuable company, with a market capitalization of over $4 trillion, and its stock has delivered strong returns over the past few years.

However, NVIDIA’s growth has led to the company trading at a premium in comparison to most of the other semiconductor players, leaving little room for disappointment if growth derails. A slowdown in AI infrastructure spending by hyperscale cloud providers could impact NVIDIA’s revenue and earnings growth, while competition from rivals like Advanced Micro Devices, Inc. AMD continues to increase.

At the same time, U.S. export curbs on cutting-edge AI chips to China have constrained NVIDIA’s entry to a key market, potentially pressuring its margins. Additionally, NVIDIA remains exposed to supply-chain disruptions due to its dependency on Taiwan Semiconductor Manufacturing Company Limited TSM for advanced chip production amid ongoing geopolitical tensions.

Given these challenges, it’s becoming increasingly difficult for NVIDIA to meet sky-high expectations. Thus, investors seeking AI exposure should look for much smaller companies with greater room for expansion. Notable among them are Western Digital Corporation WDC and Seagate Technology Holdings plc STX, whose shares have soared 662.8% and 464.5%, respectively, over the past year, outpacing NVIDIA’s gain of 22.6%.

Both Western Digital and Seagate stand to gain from the rapid growth in AI-driven demand for data storage. Let’s take a closer look at the key catalysts that could drive further upside in these AI stocks –

Western Digital’s AI Storage Boom Could Drive Further Upside

Rising demand for high-value enterprise hard disk drives and a favorable pricing environment have created a solid growth runway for Western Digital. The company’s revenues totaled $3.34 billion in the fiscal third quarter of 2026, up 45% year over year, according to the company’s press release.

Furthermore, the company expects revenues for the fiscal fourth quarter of 2026 to be about $3.65 billion, plus or minus $100 million. The upbeat guidance reflects robust demand for AI infrastructure, with cloud providers and enterprise customers continuing to invest in high-capacity storage to meet increasing AI workloads.

In the fiscal third quarter, Western Digital’s non-GAAP gross margin rose to 50.5% from 40.1% in the prior-year period. The company projects further margin expansion, with fiscal fourth-quarter non-GAAP gross margin expected to reach 51-52%. The improving gross margin is providing Western Digital with greater financial flexibility to invest in research and development, enhance earnings growth and create long-term value for shareholders.

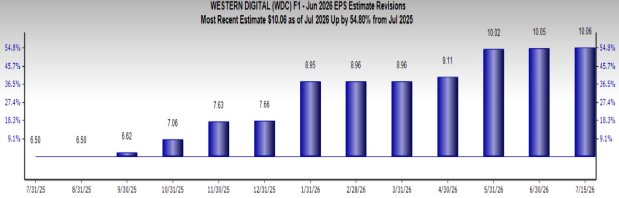

As a result, the company’s expected earnings growth rate for the current year is 104.1%. The Zacks Consensus Estimate of $10.06 for WDC’s earnings per share (EPS) is up 54.8% year over year.

Image Source: Zacks Investment Research

Seagate’s AI Infrastructure Play Gains Momentum Amid Rising Demand

Seagate is well-positioned to sustain its growth momentum, banking on rising data-center storage demand, expanding margins, and robust cash flows. These favorable trends could provide the required upside for Seagate’s shares, strengthening its position as a potential beneficiary of the AI infrastructure boom.

For the fiscal fourth quarter of 2026, Seagate expects revenues of around $3.45 billion, plus or minus $100 million, more than the $3.11 billion reported in the fiscal third quarter of 2026, according to investors.seagate.com.

Moreover, a non-GAAP gross margin of 47% in the fiscal third quarter reflected improved operational execution and enhanced profitability. Additionally, the company’s free cash flow of $953 million in the fiscal third quarter showcased the strength in its core business.

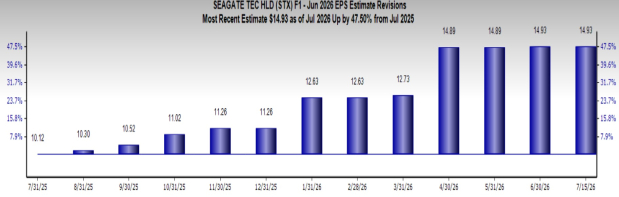

Supported by these trends, Seagate’s expected earnings growth rate for the current year stands at 84.3%, while the Zacks Consensus Estimate of $14.93 for STX’s EPS represents a 47.5% increase from the prior-year period.

Image Source: Zacks Investment Research

Both Western Digital and Seagate currently have a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).