GitLab (GTLB) took a hard hit on Tuesday, with shares falling nearly 15% after the company unveiled a major restructuring plan. The DevOps software maker said it will cut about 14% of its workforce, or roughly 350 roles, as it tries to tighten costs and sharpen its focus on profitability.

The selloff was sharp, but the reaction was not surprising. Software stocks have been pressured for months as enterprise customers slow spending and become more selective with new deals. That has hurt several names across the space, including Atlassian (TEAM) and JFrog (FROG). GitLab, though, has always stood out a bit from the pack thanks to its all-in-one platform and remote-first culture.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors, the big question is whether this drop is a warning sign or a chance to buy a quality business at a better price.

How Did GTLB Stock Perform?

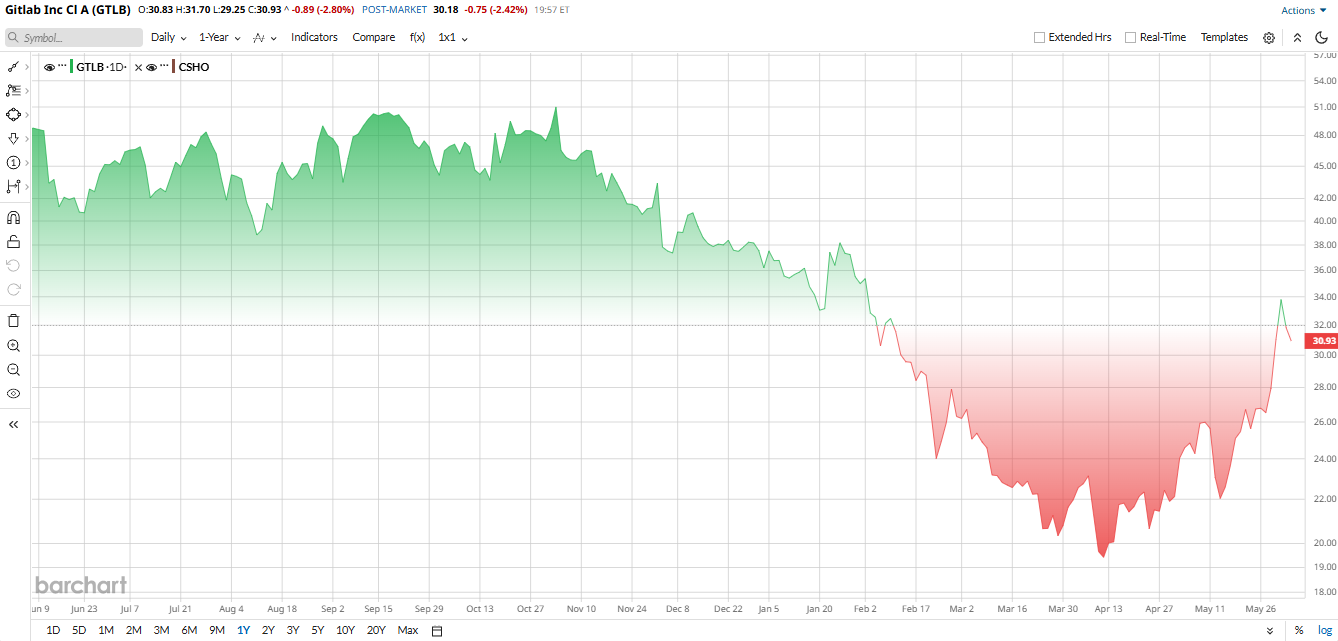

GitLab’s stock has already been under serious pressure before this latest blow. Shares are down more than 33% over the past year and had already fallen about 18% year-to-date (YTD) in 2026. With the stock now sitting well below both its 50-day and 200-day moving averages, the chart still looks weak. Sellers remain in control for now.

Still, the valuation picture is starting to look more interesting. GitLab currently trades at about 6 times forward sales, while the software sector median is closer to 8 times. Its enterprise value-to-revenue ratio is also just under 5, compared with an industry median around 7. That is not dirt cheap, but it is a noticeable discount. After such a steep reset, the market is clearly pricing in a lot of bad news.

www.barchart.com

www.barchart.com AI and Efficiency Are Driving GitLab’s Next Chapter

The restructuring move is designed to help with exactly that. By trimming headcount and streamlining operations, GitLab expects to cut annual expenses by about $60 million. Management wants to redirect more resources toward the areas where customer demand is strongest while also improving its path to profitability. That makes sense on paper, even if the headlines sound harsh.

The company still has a lot going for it beyond the cost cuts. GitLab’s platform is built to handle the entire software development cycle in one place, from planning and coding to security and deployment. That single-application approach is one of its biggest strengths. It makes collaboration easier and gives customers one system instead of a patchwork of tools.

GitLab is also leaning harder into AI. In 2026, the company has been deepening its GitLab Duo offerings, which can help automate code reviews and vulnerability fixes. That is an important move because AI has become one of the strongest selling points in software. GitLab is also expanding its managed service footprint through a major cloud partnership, giving it another route to reach enterprise customers. These efforts show management is not just cutting costs. It is also trying to position the business for the next phase of growth.

GitLab’s Fundamentals Remain Strong Despite Slower Growth

The latest quarterly results were mixed but not disastrous. For the fiscal first quarter ended April 30, 2026, revenue rose 18% year-over-year (YoY) to $282 million. That is still solid growth, even if it is a step down from the 30%-plus pace investors once expected. Subscription revenue remained the main driver at $255 million, while professional services constituted the rest.

There were also signs of progress on profitability. Net loss narrowed to $8 million from $22 million a year earlier. Adjusted earnings per share turned positive at $0.09, compared with a loss of $0.04 per share in the same quarter last year. Free cash flow came in at $38 million, and GitLab ended the quarter with $1.2 billion in cash and equivalents. That gives the company plenty of flexibility.

Retention also remains healthy. Dollar-based net retention was 118%, which is still strong even though it slipped from 125% a year ago. That suggests existing customers are still spending, even if the pace of expansion is cooling.

Guidance was another reason the stock may not be in free fall for long. For the current quarter, GitLab expects revenue between $286 million and $290 million, with adjusted EPS of $0.10 to $0.11. For the full year, it guided for revenue of $1.18 billion to $1.20 billion and adjusted EPS of $0.42 to $0.47. That range lines up closely with what Wall Street was already expecting, so the outlook is more of a reset than a collapse.

Analysts Opinions on GTLB Stock

Analysts remain divided, but the tone is still mostly constructive. Morgan Stanley downgraded the stock to “Equal Weight” and cut its price target to $48 from $62, saying the restructuring shows how quickly enterprise spending patterns have shifted. Goldman Sachs stayed bullish, keeping a “Buy” rating and a $60 target, while Needham’s Mike Cikos called the selloff overdone and kept a “Buy” rating with a $65 target.

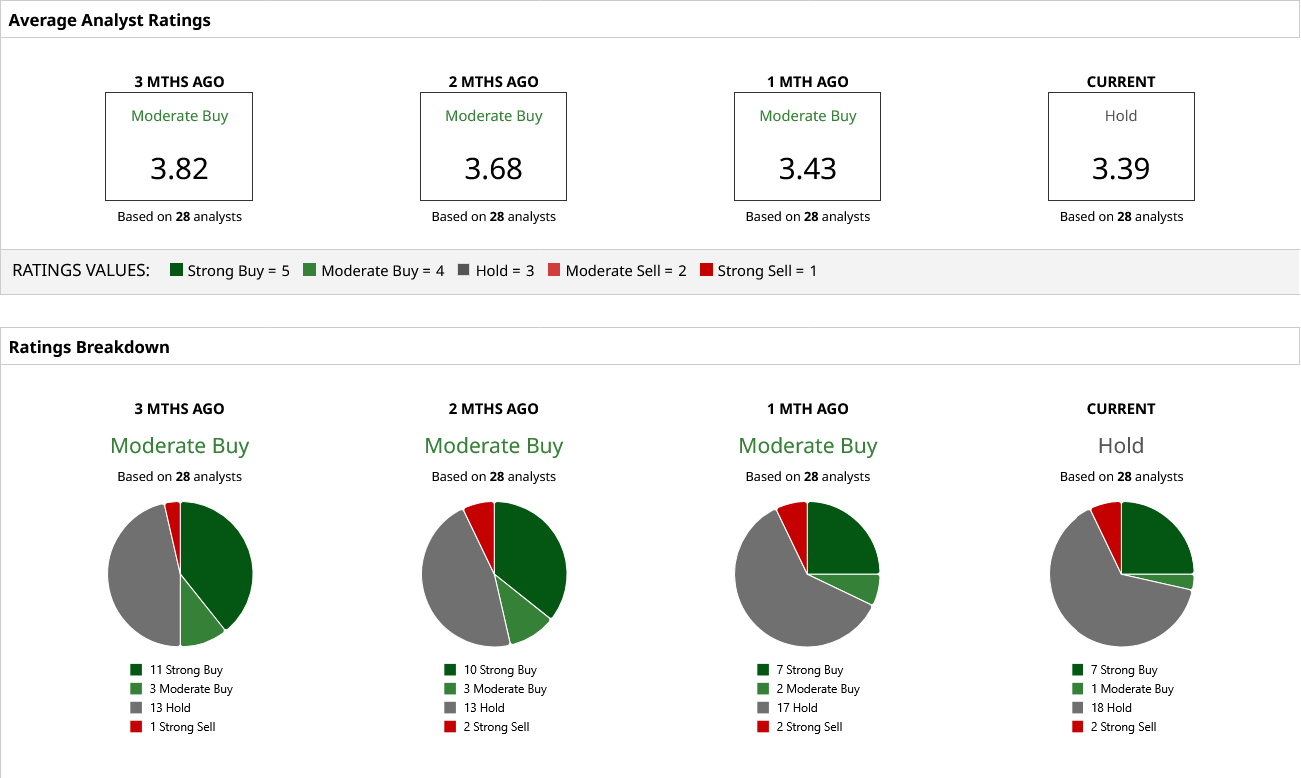

That said, the Street's overall ratings of GTLB have dimmed in the past three months. Declining analyst ratings slipped the stock from a consensus “Moderate Buy” into a “Hold” over the last month, with an average price target of $32.87, which the stock is currently trading near. However, the street high target of $65 gives the stock room to run more than 115%.

That is why GitLab remains interesting. The market is punishing the stock for slower growth and a painful restructuring. But the business is still growing, margins are improving, cash is strong, and the valuation looks more reasonable than it did a year ago. This may not be a clean story, but for long-term investors, the panic could be creating an opening.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

GitLab Shares Sink After Layoff News. Why Analysts Still See Massive Upside. The Dow's Split Personality: Why Some Winners Soar While Others Drag Down the Dow Greg Abel is Writing Checks for Berkshire Hathaway in a Hurry. You Should Write One for BRK.B Stock. Retail Investors Are Beating Wall Street Benchmarks With AI Stocks. Why That Could Change Soon.