Innovative Industrial Properties IIPR is trading at $51.90 with a 6-12 month price target of $59.00. The stock also offers an annual dividend of $7.60, which translates to a yield of about 14.9%.

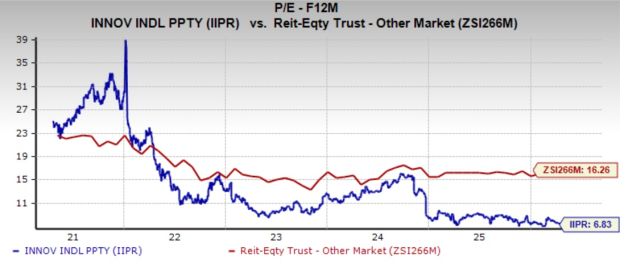

Valuation is part of the appeal. IIPR trades at 6.83x forward 12-month earnings, a steep discount versus 16.26x for its sub-industry, 15.97x for the sector, and 21.75x for the S&P 500.

Image Source: Zacks Investment Research

IIPR Snapshot for Investors: Yield, Multiple, and Target

At today’s price, the dividend is doing much of the heavy lifting for total return. A $7.60 annual payout against a $51 stock price creates a yield profile that stands out even within income-oriented real estate investment trusts.

The multiple adds to the value setup. At 6.83x forward earnings, the market is pricing IIPR well below broader real estate peers and far below the S&P 500, implying investors still want a clear path to cash flow stability.

Innovative Industrial Gets a Strong Near-Term Rating Signal

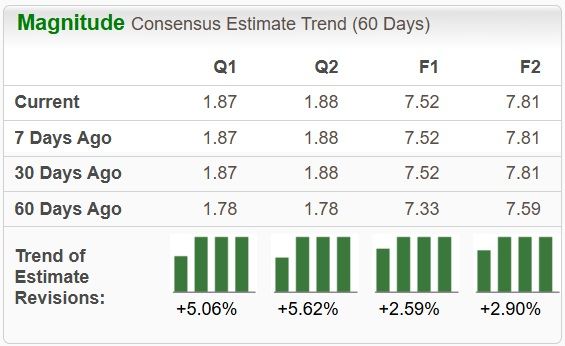

IIPR currently carries a Zacks Rank #1 (Strong Buy), which reflects favorable trends in earnings estimate revisions over the one- to three-month horizon. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Style Score mix explains what the market is rewarding right now. IIPR posts a Momentum Score of B and a Value Score of C, while Growth is weaker at F and the combined VGM score is F. In other words, the near-term setup is being driven more by price and estimate dynamics than a traditional growth narrative.

Image Source: Zacks Investment Research

IIPR’s Bull Case Depends on Rent Roll Recovery

The core “why now” hinges on tenant conditions and industry catalysts that could improve operator cash flow. Management pointed to potential cannabis rescheduling to Schedule III and possible adult-use expansions in Virginia, Pennsylvania, and Florida. A key consideration is the potential removal of 280E, which the company believes could strengthen operator credit quality and support rent obligations.

Portfolio positioning matters here. IIPR has 16 properties across these states spanning about 2.6 million square feet, contributing roughly one-fourth of annualized base rent, giving the company meaningful exposure if these catalysts develop.

Operationally, the recovery argument is tied to re-tenanting progress. IIPR completed new leases covering about 339,000 square feet in 2025 and signed or negotiated agreements for more than 900,000 square feet tied to receivership and litigation assets. Management also noted that re-leasing typically requires modest capital, around $10 to $15 per square foot, supporting operating leverage as collections stabilize.

Innovative Industrial Has a Dividend Track Record to Defend

Income investors are not just buying a headline yield. IIPR maintained its quarterly dividend at $1.90 and declared $7.60 for the full year, continuing a pattern of annual dividend increases since inception. Since 2020, the dividend has grown at an 11% compound annual rate.

The near-term payout outlook is linked to improving cash flow coverage trends. Adjusted funds from operations per share rose sequentially to $1.88 in fourth-quarter 2025 from $1.71 in the third quarter, helped by rent recoveries and investment income. That late-2025 improvement is a key marker for investors watching whether recurring cash flow can reassert itself.

IIPR’s Diversification Adds Income, Not Just a New Story

The IQHQ investment is increasingly central because it is already contributing to income. In 2025, IIPR committed up to $270.0 million to IQHQ, structured as a $100.0 million revolving credit facility and up to $170.0 million of preferred equity. As of Dec. 31, 2025, $150.0 million had been funded.

The contribution showed up meaningfully in results. Fourth-quarter 2025 included $5.0 million in quarterly interest and dividend income from IQHQ, supporting adjusted funds from operations during a period when cannabis-tenant issues were pressuring rental revenue.

Innovative Industrial’s Biggest “Buy” Debate Is Tenant Risk

The decision point is whether tenant stress continues to disrupt rent collection and portfolio economics. Concentration is high: the top 10 tenants accounted for about 72% of annualized base rent at year-end 2025, and two key tenants, PharmaCann (roughly 10%) and 4Front (about 6%), had leases in default during 2025.

Occupancy also weakened during the year, with leased occupancy falling from 98.4% on March 31, 2025 to 95.8% by Sept. 30, 2025. At the same time, management flagged that re-leasing economics can reset lower, with some transactions around or below 50% of prior contractual rent, depending on the asset and market.

For context, other real estate investment trusts in the same broader peer set offer more conventional income profiles. LTC Properties, Inc. LTC shows a dividend yield of 5.79% and a Zacks Rank #3 (Hold). SmartStop Self Storage REIT, Inc. SMA has a 5.05% yield and a Zacks Rank #4 (Sell). IIPR’s yield is materially higher, but the tenant-credit swing factor is also larger.

IIPR Checklist: What to Watch Through 2026

First, track execution around the PharmaCann transition. The settlement requires PharmaCann to turn over properties in New York and Pennsylvania by May 20, 2026 and Ohio by May 26, 2026, and IIPR has said it is in active discussions with prospective tenants for all three locations.

Second, monitor the 4Front timeline. IIPR reached tentative agreements with prospective new tenants for four 4Front-related assets, with expectations that agreements take effect after receivership proceedings conclude, which the company expects by the third quarter of 2026. That sets the stage for whether late-2026 leasing starts can become a real cash flow driver.

Third, stay focused on the balance sheet and interest burden. Interest expense rose to $20.2 million in 2025, with $102.5 million outstanding on the revolver at year-end and roughly $291.0 million of notes maturing in 2026. How refinancing terms evolve, and whether rent recovery keeps pace, will shape the next leg of earnings stability.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Smartstop Self Storage REIT Inc (SMA): Free Stock Analysis Report

LTC Properties, Inc. (LTC): Free Stock Analysis Report

Innovative Industrial Properties, Inc. (IIPR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).