Shares of Dell Technologies (DELL) soared more than 39% in after-hours trading after the company delivered blockbuster first-quarter fiscal 2027 results, driven by explosive demand for artificial intelligence (AI) infrastructure. Dell crushed Wall Street expectations and prompted management to increase its full-year outlook, highlighting that the company is among the biggest beneficiaries of the AI spending boom.

Into Dell’s Stellar Q1 Performance

Dell reported first-quarter revenue of $43.8 billion, representing 88% year-over-year increase. Moreover, its revenue was far above management’s prior guidance range of $34.7 billion to $35.7 billion. Profitability improved significantly alongside the surge in revenue. Gross margin dollars climbed 57% to $7.8 billion, while operating income jumped 154% to $4.2 billion.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Net income nearly tripled to $3.2 billion, driven by strong operational execution across the business. Adjusted earnings per share (EPS) reached a record $4.86, significantly outperforming both management’s guidance of $2.90 and analyst expectations of $2.79.

The company’s Infrastructure Solutions Group (ISG) was the key growth engine behind the quarter. ISG revenue surged to a record $29 billion, up 181% year-over-year. AI server demand remained exceptionally strong throughout the quarter, with Dell generating $24.4 billion in AI orders and registering $16.1 billion in AI server revenue.

www.barchart.com

www.barchart.com Notably, Dell’s ending AI backlog expanded to a record $51.3 billion. Management noted that demand continues to exceed supply. Despite converting massive order volumes into revenue during the quarter, Dell indicated that its AI pipeline continues to grow sequentially and remains multiple times larger than its existing backlog.

Dell’s AI momentum is being driven by broad-based demand across hyperscalers, cloud providers, sovereign entities, and enterprise customers. The company believes its expanding portfolio of AI infrastructure solutions is helping it gain market share as organizations aggressively invest in next-generation computing capabilities.

Traditional server demand also remained extremely healthy. Revenue from traditional servers rose 92% year-over-year, supported by enterprise customers refreshing aging infrastructure and expanding compute capacity to handle increasingly complex workloads. Dell highlighted that much of the installed server base still runs on 14th-generation or older systems, leaving a substantial refresh opportunity ahead.

In addition, AI inference workloads are beginning to create incremental demand for traditional compute infrastructure, adding another tailwind to growth.

Dell’s Strong Outlook Signals Continued Momentum

Looking ahead, Dell expects momentum to continue. For the second quarter, the company forecasts revenue between $44 billion and $45 billion, implying 49% growth at the midpoint. ISG revenue is expected to rise by approximately 75%, supported by approximately $15.5 billion in AI server revenue, while the Client Solutions Group (CSG) is projected to grow by roughly 20%.

Dell’s adjusted EPS for Q2 is expected to reach approximately $4.80, more than doubling from the prior year.

Dell also significantly raised its full-year outlook. The company now expects fiscal 2027 revenue between $165 billion and $169 billion, up from prior guidance of $138 billion to $142 billion, representing 47% growth at the midpoint. ISG revenue is projected to grow roughly 80%, driven by an estimated $60 billion in AI server revenue. Earlier, management projected $50 billion in AI revenue.

Traditional server revenue is expected to rise by more than 60%, while storage and CSG are both projected to continue growing.

On the profitability side, Dell expects operating income to increase more than 55% for the full year, while adjusted earnings per share are forecast to reach approximately $17.90, up roughly 75% year-over-year. This compares favorably to management's earlier forecast of $12.90.

Is There More Upside Left in Dell Stock?

Following the sharp post-earnings rally, Dell’s valuation will become more demanding. However, the company’s strong growth trajectory, massive AI backlog, and expanding earnings suggest further upside potential in Dell stock.

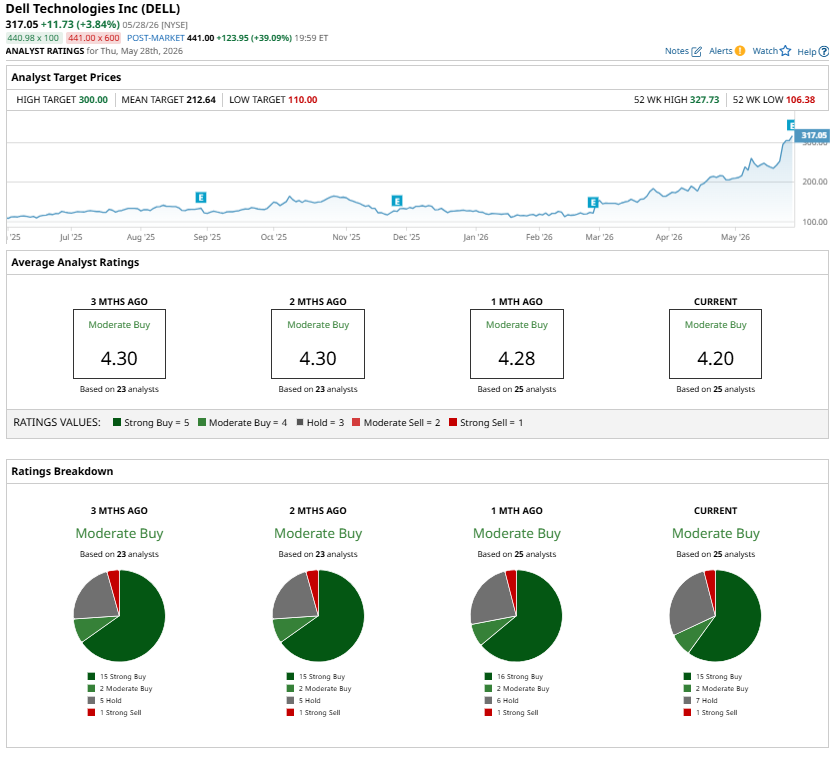

With enterprise AI adoption still in its early innings and infrastructure demand continuing to outpace supply, Dell appears well-positioned to remain one of the primary beneficiaries of the global AI investment cycle. Analysts are upbeat and maintain a “Moderate Buy” consensus rating.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AI Boom Powers Dell Stock’s Post-Earnings Rally. Get Ready for More Upside Ahead. The Quantum Computing Boom Is Back. IBM Proves It Is the Smartest Stock to Buy AI Hyperscalers Are Taking on Debt, But the Broader Market Looks More Leveraged Wedbush Just Set a New Street-High Price Target of $325 on Palo Alto Networks. What This Means for PANW Stock.