lululemon athletica inc. (LULU), headquartered in Vancouver, Canada, designs, distributes, and retails athletic apparel, footwear, and accessories under the lululemon brand for women and men. Valued at $13.8 billion by market cap, the company produces fitness pants, shorts, tops and jackets for yoga, dance, running, and general fitness.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and LULU perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the apparel retail industry. LULU's reputation for quality and innovation has built a loyal customer base, driving repeat purchases and positive word-of-mouth. Their consistent R&D investment leads to unique products that set them apart from competitors, allowing control over the customer experience and margins.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

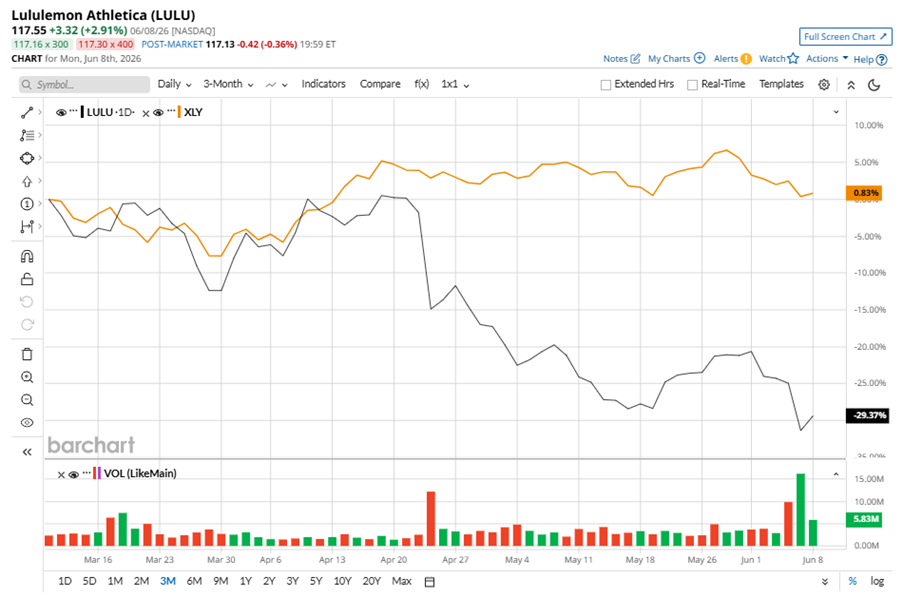

Despite its notable strength, LULU slipped 56% from its 52-week high of $266.95, achieved on Jun. 9, 2025. Over the past three months, LULU stock declined 30.9%, notably underperforming the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) marginal gains during the same time frame.

www.barchart.com

www.barchart.comShares of LULU plummeted 43.4% on a YTD basis and 55.7% over the past 52 weeks, considerably underperforming XLY’s YTD 3.4% losses and 8.8% returns over the last year.

To confirm the bearish trend, LULU has been trading below its 50-day moving average since late January, with slight fluctuations. The stock is trading below its 200-day moving average over the past year.

www.barchart.com

www.barchart.comLULU’s underperformance largely reflects the impact of higher tariff costs, along with investments in store openings, optimizations, and its distribution network.

On Jun. 4, LULU reported its Q1 results, and its shares closed down by 8.6% in the following trading session. Its EPS of $1.69 beat Wall Street expectations of $1.67. The company’s revenue was $2.5 billion, beating Wall Street forecasts of $2.4 billion. The company expects full-year EPS to be $10.95 to $11.15, and revenue ranging from $11 billion to $11.2 billion.

In the competitive arena of athleisure, adidas AG (ADDYY) has taken the lead over LULU, with a 4.1% downtick on a YTD basis and 21.4% decline over the past 52 weeks.

Wall Street analysts are cautious on LULU’s prospects. The stock has a consensus “Hold” rating from the 31 analysts covering it, and the mean price target of $167.58 suggests a 42.6% ambitious potential upside from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

McDonald’s Stock Could Be Bottoming, Creating a Contrarian Bet for Long-Term Investors Intel Becomes Plan B for the Semiconductor Industry. Here's How That's a Winning Strategy Dear KLA Stock Fans, Mark Your Calendars for June 12 Iran War Apathy Has Left Rare Earth Stocks in Critical Condition. Stay Far Away from the REMX ETF’s Dangerous Trap.