CoreWeave (CRWV) is not a normal cloud company. It sells Nvidia (NVDA)-powered GPU capacity to AI labs, enterprises and hyperscalers that need compute fast. That gives it a firm seat in the AI buildout, but it also leaves investors with a capital-heavy model, weighty borrowing and a stock that can move hard on every headline.

That's what happened on Thursday when CoreWeave announced a $3.5 billion debt offering to raise more capital for its fast-growing AI cloud business. The move shows the extensive amount of money the company still needs to continue expansion. And it also raises a bigger question for investors. Is CRWV worth buying now, or is the stock already too expensive?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

What Does the Valuation Say About CRWV Stock?

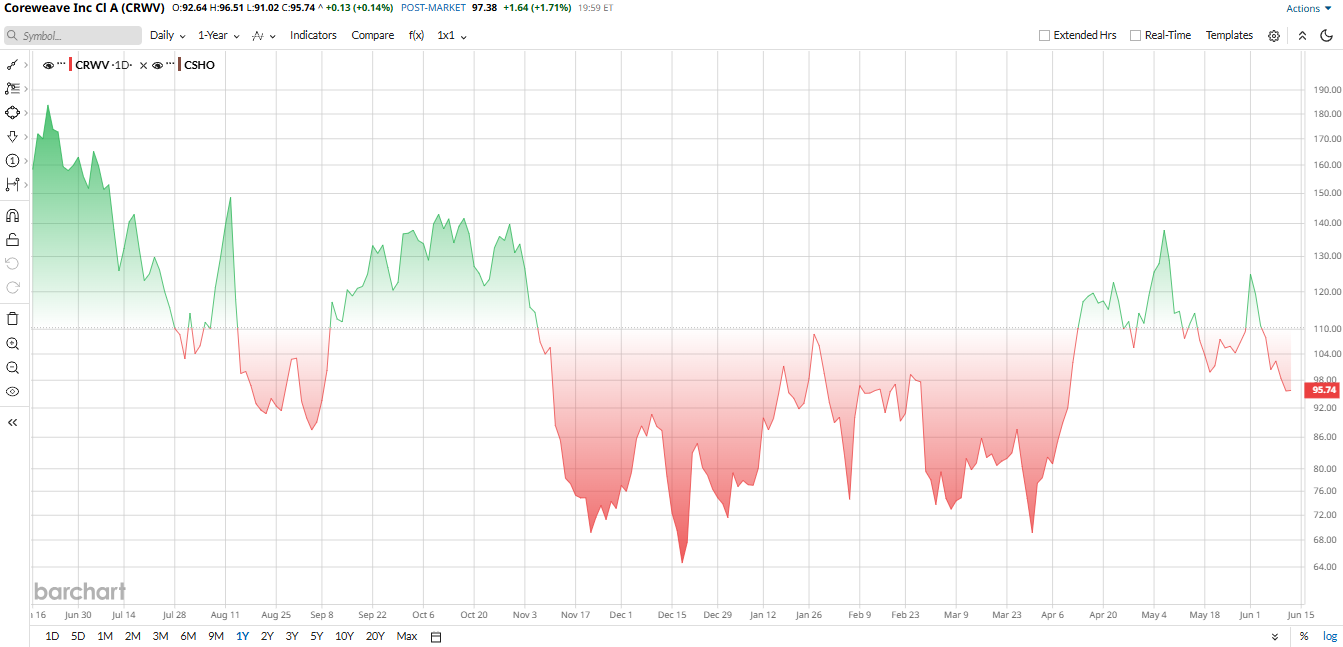

CRWV has been a roller coaster over the past year. The stock ripped higher after the IPO, then got hit by worries about debt, capex, and lumpy execution. In the latest Barchart technical read, the shares were still up 40.41% year to date (YTD), but they sat below the 50-day and 200-day moving averages. That is not what you want to see if you are betting on clean momentum.

Valuation of this AI giant doesn't look cheap at all. Reuters reported that CoreWeave’s valuation had climbed to $61.6 billion, and the company is guiding for about $12.5 billion in revenue this year. That puts the stock at roughly 4.33 times forward sales, which is fine for a hot growth name, but not exactly a bargain when profits are still negative, and the company keeps financing expansion with debt. However, its price-to-cash flow (TTM) of 9.17 times is 50% cheaper than the sector, suggesting some relative affordability.

www.barchart.com

www.barchart.com Why the $3.5 Billion Debt Deal Matters

Hence, the $3.5 billion convertible note sale matters significantly. CoreWeave priced 1.75% convertible notes due 2032 and said it would use the proceeds for general corporate purposes after funding capped calls that are meant to reduce dilution. The notes were upsized from $3 billion, which indicates the company wanted plenty of room to keep building.

Investors did not cheer the new debt, but they also did not run for the exits. The market has already learned that CoreWeave’s growth engine needs a lot of fuel. New data centers, Nvidia chips, and customer commitments all cost money. So the offering wasn't a shock. It was more of a reminder that the AI boom is expensive, even for the companies winning contracts.

The Latest Quarter Was Big on Growth

CoreWeave’s latest quarter was strong on the top line and rough on the bottom line. Revenue reached $2.078 billion, up from $982 million a year earlier, and the company posted a net loss of $740 million, wider than the $315 million loss in the same quarter last year. Adjusted operating income fell to $21 million from $163 million, and adjusted net loss widened to $589 million. Cash and cash equivalents were $2.244 billion at quarter-end.

The growth story is still real. Backlog reached $99.4 billion, and CEO Michael Intrator said, “This was the strongest bookings quarter in CoreWeave’s history.” He also said the company had surpassed 1 GW of active power and was on the way to more than 8 GW by 2030. That is a huge number, and it shows why bulls keep leaning in.

Yet, the market focused on the weak side of the report. CoreWeave guided second-quarter revenue to $2.45 billion to $2.6 billion, below Wall Street’s roughly $2.7 billion target, while 2026 capex could run $31 billion to $35 billion.

Certainly, the company has the demand. But how much more pain can it endure while it keeps building?

What CoreWeave Is Doing, and What Wall Street Thinks

The banner theme in 2026 is expansion. CoreWeave inked onto "giant deals" that include Meta Platroms (META), Anthropic and Jane Street, while also further progressing into a +5 GW of AI factories by 2030 by strengthening its relationship with Nvidia. The good part is apparent. The bigger the capacity, the higher the revenue. The danger is as clear as the source of the danger. More capacity, and more costs, and more debt, and more opportunities for mishaps and miscalculations when executing.

Wall Street is split, but with a positive tone. Citi's Tyler Radke has a positive view of CoreWeave with a $160 target and a “Buy” rating, though he believes the company still has plenty of “durable” AI demand.

On the other hand, Morgan Stanley warns of debt and concentration of customers for “Equal-Weight” rating and $46 targets.

Other remains bullish, D.A. Davidson upped the count to $68 from $36 but said the model was flawed. Bernstein is bearish on the big hyperscaler relationships and has a $56 rating, as they don't have a lasting impact as they seem to. There's one common easy theme. All prefer the development. Not everyone believes in the balance sheet.

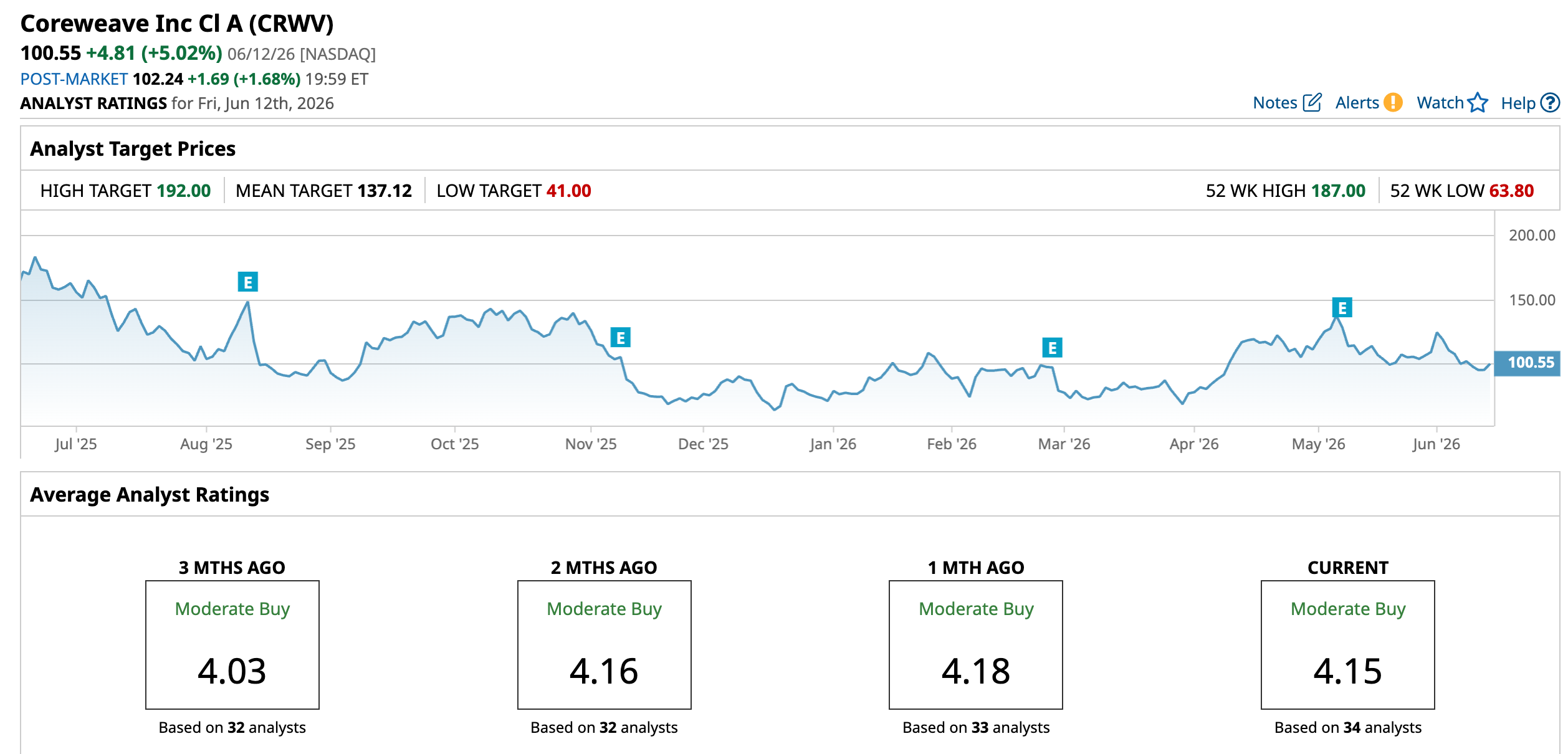

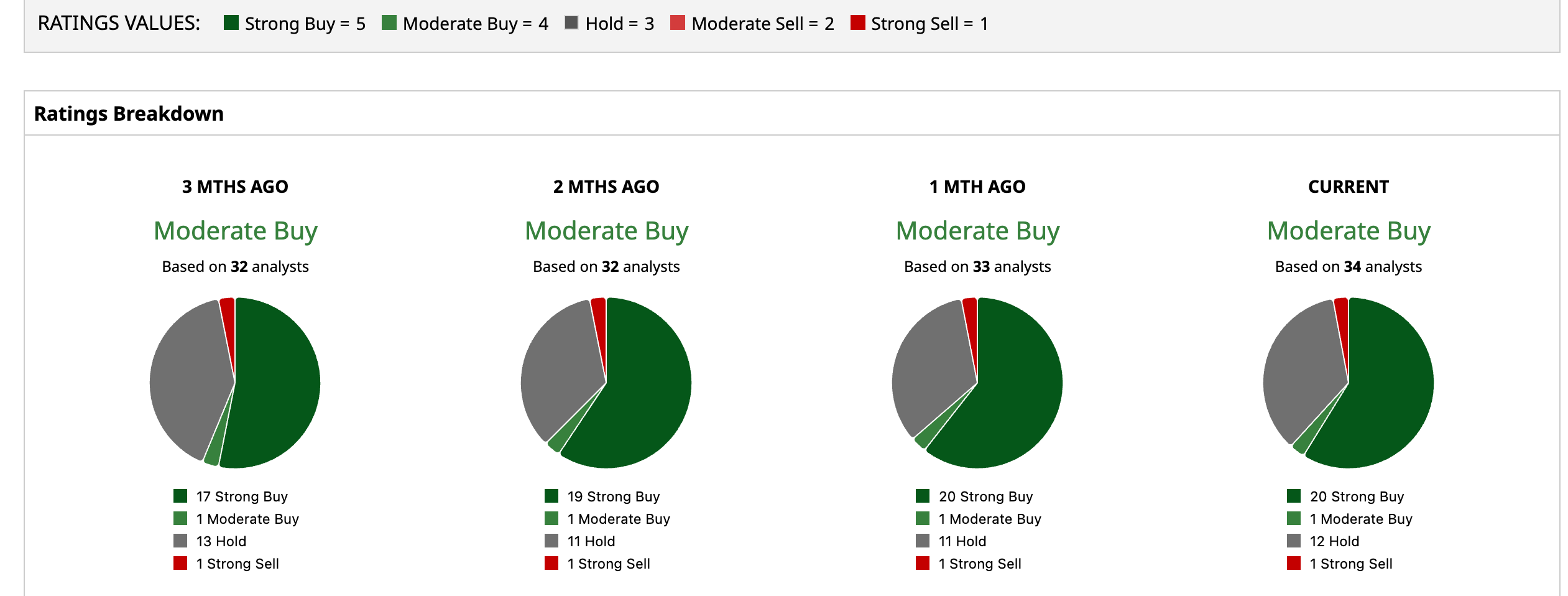

The ratings consensus among 34 analysts point to a “Moderate Buy” for CoreWeave. Twenty are bullish, providing a “Strong Buy” rating, one gives a “Moderate Buy,” 12 give a “Hold,” and the remaining analyst is bearish with a “Strong Sell.” The analysts set an average price target of $137.12, which implies 36.4% upside potential. The Street-high price target of $192 implies an upside potential of 91% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX's First Full Week, FOMC and Other Key Things to Watch this Week CoreWeave Just Raised $3.5 Billion. How to Play the AI Stock Here. Adobe CFO Quits to Join a Chipmaker. You Shouldn’t Quit ADBE Stock. When the AI Trade Collapses, These 3 S&P 500 Sectors Are Your Best Bet