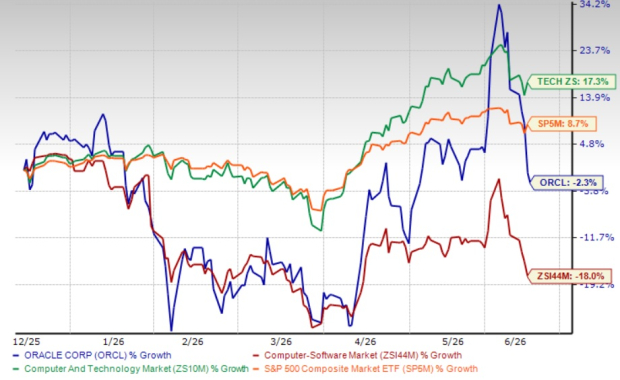

Oracle ORCL shares took a sharp hit on June 11, 2026, tumbling between 8% and 10% in a single session following the release of fourth-quarter fiscal 2026 results the previous evening. Shares of Oracle have lost 2.3% in the past six-month period.

The stock, which closed at approximately $201 before the earnings announcement, slid toward the $180-$184 range as investors reacted negatively to the company's aggressive capital spending plans and a large equity fundraise that raised dilution concerns. The pullback dragged the stock further from its 52-week high of $345.72, though it remains above its 52-week low of $134.57. The selloff, coming despite a broad-based earnings beat, underscores a market that is increasingly scrutinizing the cost of Oracle's AI ambitions rather than celebrating the revenue momentum.

ORCL’s 6-Month Performance

Image Source: Zacks Investment Research

ORCL’s Q4 Results: A Beat With Caveats

Oracle posted record fourth-quarter total revenues of $19.2 billion, up 21% in USD, driven by record cloud revenues of $9.9 billion, up 47%. Within the cloud, infrastructure revenues surged 93% to $5.8 billion, while cloud applications grew 10% to $4.1 billion. GAAP EPS rose 21% to $1.45, and non-GAAP EPS climbed 24% to $2.11. For the full fiscal year, total revenues reached a record $67.4 billion, up 17%, with cloud revenues rising 39% to $34.0 billion. On the AI front, Oracle disclosed that the Oracle Multicloud AI Database grew 404% in the fiscal fourth quarter, making it the company's fastest-growing business ever.

Beyond revenues, Oracle reported a significant AI engagement milestone. Remaining Performance Obligations ended the quarter at $638 billion, up 363% year over year and $85 billion sequentially from the end of the fiscal third quarter. On the product side, Oracle's June 2026 OCI AI update highlighted new capabilities, including the addition of Cohere Rerank 4 and expanded multimodal support, as well as expanded OCI Enterprise AI availability in the UAE Central (Abu Dhabi) region, signaling continued geographic buildout of its cloud infrastructure.

Capex Overshoot and Negative Free Cash Flow Are Real Headwinds

The headline numbers, however, were overshadowed by a financial structure that alarmed investors. Oracle reported $23.7 billion in negative free cash flow for fiscal 2026, with capital expenditures jumping 162% to $55.7 billion — exceeding the company's own $50 billion projection for the year. In the fiscal fourth quarter alone, the company spent $15.9 billion on capital expenditures. Adding to investor unease, Oracle announced plans to raise approximately $40 billion through a combination of debt and equity financing in fiscal 2027, including a previously announced $20 billion at-the-market equity issuance. The prospect of meaningful share dilution, layered on top of already deeply negative free cash flow, is a near-term overhang that investors cannot easily dismiss.

Compounding the concern, management flagged during the earnings call that gross margins will step down due to the timing for the ramp-up of data center projects into their full revenue contribution. This signals that profitability pressure will linger into fiscal 2027 before the contracted backlog begins converting meaningfully into earnings.

Forward Guidance: Growth Intact Amid Execution Risk

Oracle's guidance for the first quarter of fiscal 2027 calls for total revenue growth of 27-29% and total cloud revenue growth of 57-63% in constant currency, with non-GAAP EPS of $1.72-$1.76. For the full fiscal year, Oracle confirmed prior revenue guidance of $90 billion and raised non-GAAP EPS guidance to $8.05, representing 18% growth. The $90 billion revenue target implies a significant step-up from the $67.4 billion reported in fiscal 2026 and meeting it will require flawless execution across data center ramp-ups, GPU procurement and customer delivery timelines. Oracle also confirmed plans to bring almost one gigawatt of computing power online in the current quarter — roughly equivalent to the total for all of fiscal 2026.

The Zacks Consensus Estimate for ORCL's fiscal 2027 earnings is pegged at $8 per share, marking an upward revision of 0.1% over the past 30 days. The earnings figure suggests 0.83% decline over the figure reported in fiscal 2026.

Oracle Corporation Price and Consensus

Oracle Corporation price-consensus-chart | Oracle Corporation Quote

The $638 billion RPO is a genuine long-term catalyst. However, a significant portion of it involves large-scale AI contracts where customers prepaid for GPU purchases or supplied their own GPUs to Oracle, which alters the traditional economics of how that backlog translates into free cash flow and earnings per share. Investors eyeing a near-term re-rating will need to wait for evidence that the backlog converts cleanly.

Valuation and Competitive Landscape

From a valuation standpoint, ORCL stock is currently trading at a premium with a trailing 12-month Price/Earnings ratio of 31.05x, which is higher than the Zacks Computer - Software industry average of 24.37x. Oracle carries a Value Score of D.

ORCL’s Premium Valuation Raises Concern

Image Source: Zacks Investment Research

Against this backdrop, Oracle faces intensifying competition from three hyperscalers who are simultaneously its cloud rivals and, in some cases, its infrastructure partners. Amazon AMZN is aggressively pursuing AI vertical integration through AWS, while Microsoft MSFT reported strong Azure momentum and confirmed capital expenditures of approximately $190 billion for 2026. Alphabet GOOGL-owned Google Cloud is pushing a full-stack AI approach built on custom TPUs, with Gemini Enterprise recording 40% quarter-over-quarter growth in paid monthly active users and processing more than 16 billion tokens per minute via direct API use. Amazon has expanded Bedrock with Titan Ultra 2, featuring a two-million-token context window, while Microsoft launched Azure Confidential AI with hardware-backed enclaves, reinforcing its position in regulated industries like finance and healthcare. Google Cloud's growing TPU-as-a-service offering, Amazon's recent $50 billion OpenAI commitment that expands AW' AI model access through Bedrock, and Microsoft Azure's deeply embedded Copilot ecosystem collectively represent formidable competition that could challenge Oracle's ability to win new workloads beyond its existing customer base.

Conclusion

Oracle's record fourth-quarter results confirm that the AI infrastructure opportunity is real and the demand is substantial. However, with deeply negative free cash flow, rising equity dilution, compressing near-term margins and an expensive valuation relative to peers, ORCL warrants a Hold stance for now. Investors should monitor how efficiently Oracle converts its record $638 billion backlog into sustainable earnings before adding exposure. ORCL stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).