Wells Fargo & Company (WFC) provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. The San Francisco, California-based company has a market cap of $245.1 billion and operates through Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, and Wealth and Investment Management segments.

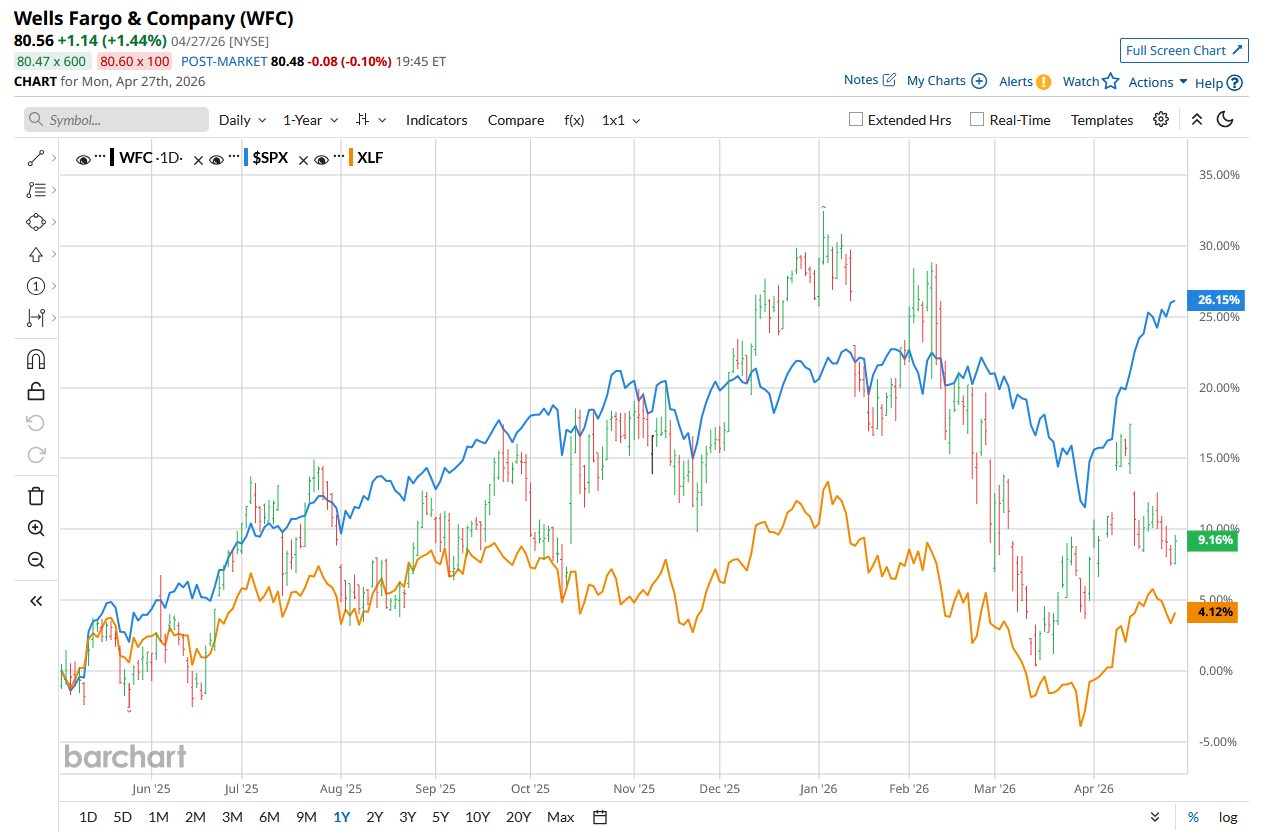

Shares of the company have lagged behind the broader market over the past year and in 2026. WFC stock has risen 15.5% over the past 52 weeks and has declined 13.6% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 29.8% over the past year and risen 4.8% in 2026.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Narrowing the focus, WFC has outperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 7.9% rise over the past 52 weeks, but has lagged behind its 5.4% decline this year.

www.barchart.com

www.barchart.com On Apr. 14, WFC stock declined 5.7% following the release of its worse-than-expected Q1 2026 earnings. The company’s total revenue rose nearly 6% from the prior year’s quarter to $21.4 billion and missed the Street’s estimates. Moreover, its adjusted EPS amounted to $1.56, also coming in below Wall Street’s forecasts.

For the current year ending in June, analysts expect WFC’s EPS to increase 11% year over year to $1.71. Moreover, the company has surpassed analysts’ consensus estimates in three of the past four quarters, while missing on one occasion.

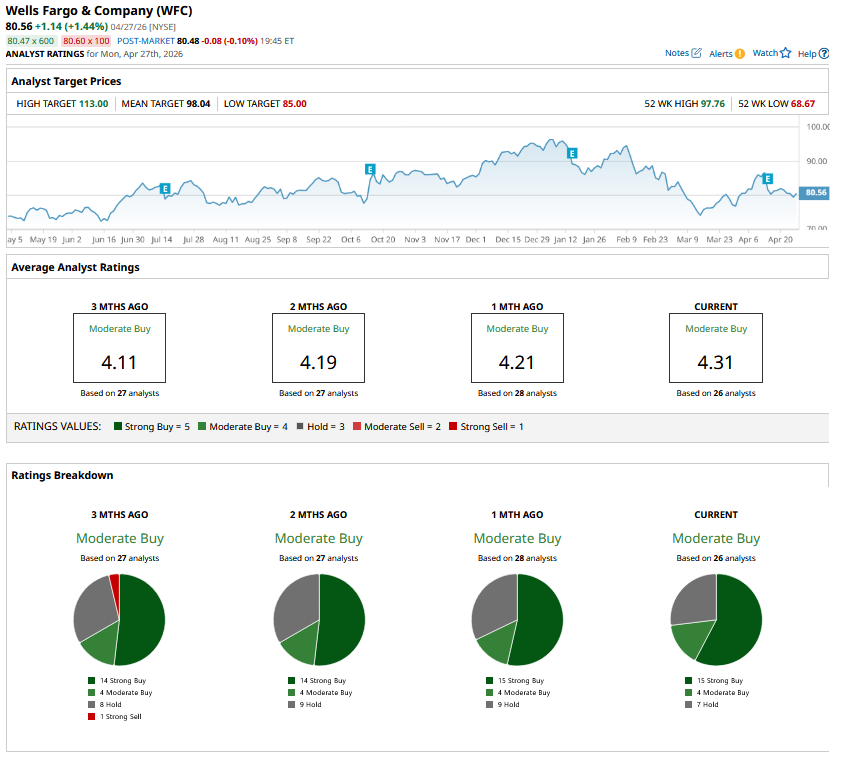

Among the 26 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 15 “Strong Buy” ratings, four “Moderate Buy” ratings, and seven “Hold” ratings.

www.barchart.com

www.barchart.com This configuration has remained mostly stable in recent months.

On Apr. 15, Piper Sandler analyst Scott Siefers maintained a “Buy” rating on Wells Fargo and set a price target of $100.

WFC’s mean price target of $98.04 indicates a premium of 21.7% from the current market prices. Its Street-high target of $113 suggests a robust 40.3% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now Dear Sandisk Stock Fans, Mark Your Calendars for April 30 This Analyst Just Upgraded SNAP Stock. Here's Why. Marvell Technology Just Sent POET Stock Plummeting. What Comes Next?