During a bruising 2025, Washington and Beijing spent months locked in a trade war that rattled supply chains, squeezed exporters, and reminded the world of the intertwining depth of the two economies. Now, with President Donald Trump sitting down with Chinese President Xi Jinping in Beijing, the mood has suddenly shifted from confrontation to cautious dealmaking. Markets are watching closely. U.S. stocks are hovering near record highs, investors are betting the two sides want stability more than another escalation, and expectations are building around a fresh extension of last year’s trade truce.

But while headlines may focus on tariffs, soybeans, and diplomacy, one American company could quietly walk away as the biggest winner of the summit – Boeing (BA). The aerospace giant has spent the past several years battling through safety scandals, production headaches, regulatory scrutiny, and a towering debt pile. Even strong April numbers were not enough to fully reignite investor excitement. Yet Beijing may hold the missing piece.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Boeing CEO Kelly Ortberg joined Trump’s delegation to China this week, signaling that aircraft negotiations are becoming a major part of the broader economic talks. And this is not about a token order. Reports suggest China is considering a purchase of roughly 500 Boeing 737 Max jets, alongside discussions for additional Dreamliners and 777X aircraft down the road.

If the agreement materializes, it could become one of the largest aircraft deals in aviation history, and potentially the moment Boeing’s comeback story finally starts looking real again.

About Boeing Stock

As one of the world’s largest aerospace and defense companies, Boeing plays a central role in shaping global aviation and security. Headquartered in Arlington, Virginia, the company develops and manufactures commercial airplanes, defense systems, and space technologies for customers in more than 150 countries. Boeing is widely recognized for aircraft such as the 737 and 787 Dreamliner and serves major institutions, including NASA and the United States Department of Defense. With a market cap of about $189.7 billion, Boeing remains a key force driving innovation across commercial aviation, defense, and space industries.

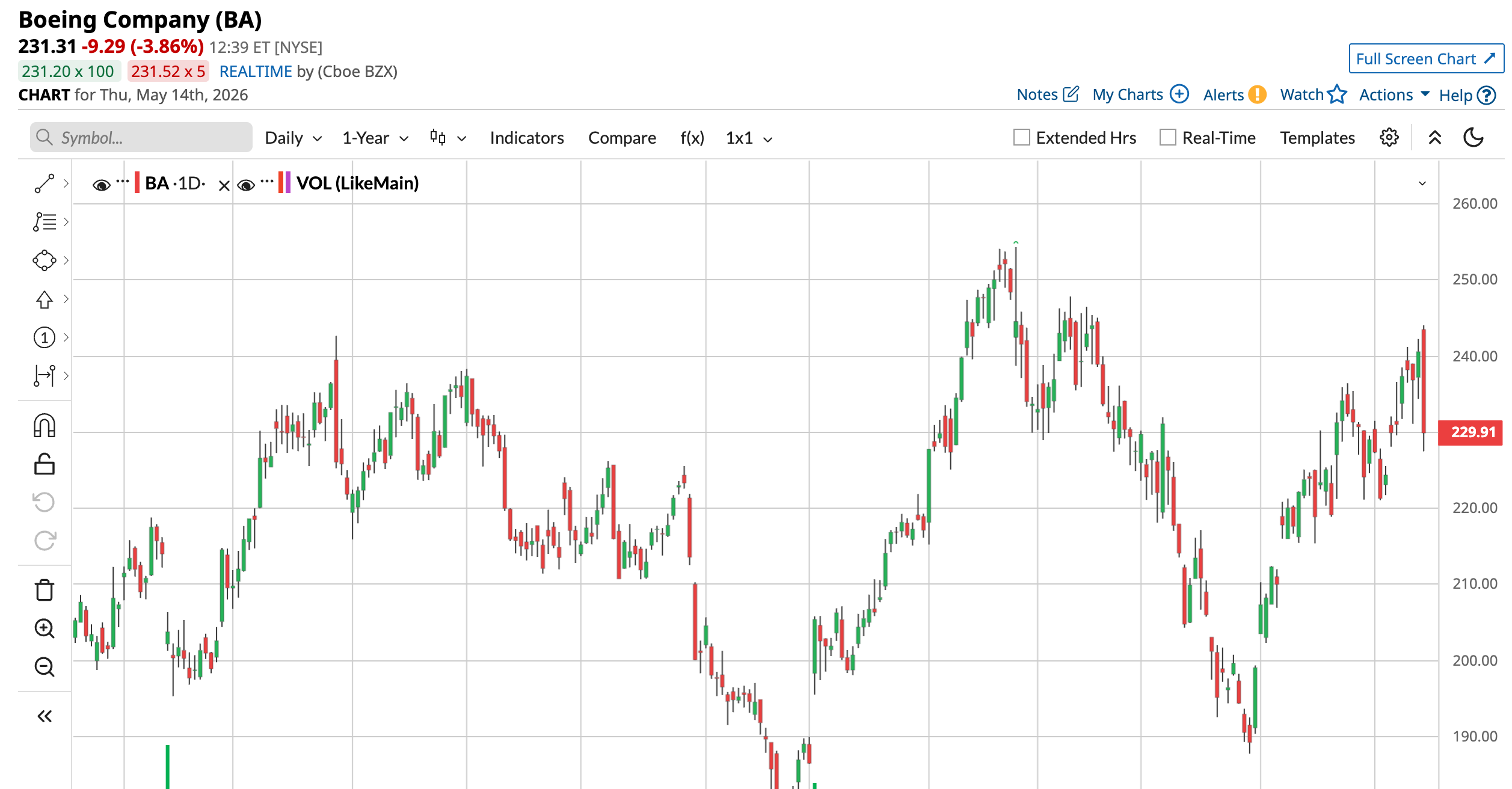

Boeing stock has quietly been building momentum. Shares of the aerospace giant have climbed 11.83% over the past 52 weeks and surged nearly 17.69% in just the last six months as investors increasingly bought into the company’s recovery story. Earlier this year, Boeing touched a high of $254.35 in January. While the stock has pulled back about 9.5% from that level, it is still holding onto a 5.44% gain year-to-date (YTD).

Technically, however, it sends a mixed message. Boeing’s 14-day RSI sits at 51.52, creeping closer to overbought territory and suggesting the rally may be getting stretched. But the MACD oscillator is flashing a caution signal. While the broader chart still suggests improving momentum, the indicator suggests bullish strength is beginning to fade. The MACD line has slipped below the signal line, while the histogram has moved into negative territory with red bars emerging – a sign that near-term buying momentum may be cooling.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Boeing’s turnaround story does not come at a bargain price. The stock, priced at 1.94 times forward sales, sits above both its historical average and many industry peers. But right now, investors seem less focused on finding a discount and more interested in buying into a recovery story, one where Boeing’s climb back to cruising altitude is just getting started.

Boeing Surges After Q1 Report

Last month, Boeing’s first-quarter results gave investors a fresh dose of optimism and lifted shares more than 5.5%. It offered fresh signs that the company’s turnaround is gaining traction as numbers topped Wall Street expectations and strengthened confidence in CEO Kelly Ortberg’s recovery strategy.

Boeing posted $22.2 billion in revenue for the quarter, up 14% year-over-year (YOY) and ahead of forecasts. Its non-GAAP loss per share amounted to -$0.20, still a loss, but far better than analysts had expected from a company that spent the last few years buried under crises, production setbacks, and regulatory headaches.

Right now, rather than obsessing over the headline numbers, investors are focused on the basics like deliveries, cash burn, and whether the company is finally finding steady air beneath its wings. And on those fronts, Boeing showed meaningful progress.

Boeing delivered 143 commercial jets during the quarter, up from 130 a year ago, as production slowly recovered from the fallout tied to the Alaska Air door-plug incident in early 2024. The 737 Max accounted for 114 deliveries, nearly 80% of total output. The company also shipped 29 wide-body aircraft, including 787 Dreamliners and 777s, showing demand for long-haul travel still remains solid globally.

Meanwhile, Boeing’s cash situation is appearing less alarming. Adjusted free cash flow was negative $1.45 billion, still deep in the red but dramatically improved from last year’s burn rate. Operating cash flow also improved sharply, down from negative $1.6 billion reported a year ago to a negative $179 million in Q1. Plus, Boeing ended the quarter with nearly $21 billion in cash and investments in marketable securities while trimming debt modestly.

And then there’s the backlog – the giant number Wall Street loves to watch. Boeing’s backlog swelled to nearly $695 billion, including more than 6,100 commercial airplanes waiting to be built and delivered. Despite inflation, geopolitical chaos, and higher fuel costs, airlines worldwide still desperately need planes.

Boeing is aiming for something it has not consistently delivered in years, which is positive free cash flow. Management expects between $1 billion and $3 billion in FCF for fiscal 2026, with improvement building throughout the year and the second half turning positive. Looking further out, Boeing sees cash flow accelerating through higher aircraft deliveries, stronger defense execution, and growth in services. The management even believes hitting $10 billion in FCF is well within reach as it works through its massive backlog.

Analysts tracking Boeing predict Q2 revenue to be around $24 billion, while losses are expected to be -$0.23 per share. Looking ahead to fiscal 2026, losses are anticipated to narrow by 98.6% YOY to -$0.15 per share, before catapulting skyward to a $4.06 profit per share in fiscal 2027.

Boeing’s Strong April Numbers

Boeing kept the momentum going in April, putting up numbers that likely caught Wall Street’s attention. The company booked 135 net new orders during the month, almost matching everything it brought in during the entire first quarter. April included orders for 57 737 Max jets and 51 787, along with 28 orders for the 777X.

Through the first four months of the year, Boeing has landed 284 net orders after accounting for cancellations and conversions, marking its strongest start to a year since 2014.

Boeing delivered 47 commercial jets in April, one more than the previous month. That matters because deliveries are where the real money starts showing up – customers typically pay the bulk of an aircraft’s cost once the jet is delivered, making it one of the most closely watched numbers for investors. The April tally included 34 of Boeing’s workhorse 737 Max jets and six 787 Dreamliners.

The company is still dealing with a few speed bumps. Certification delays tied to premium cabin seats continue to slow some 787 deliveries, but Boeing is sticking with its target of delivering between 90 and 100 Dreamliners this year.

What Do Analysts Expect for Boeing Stock?

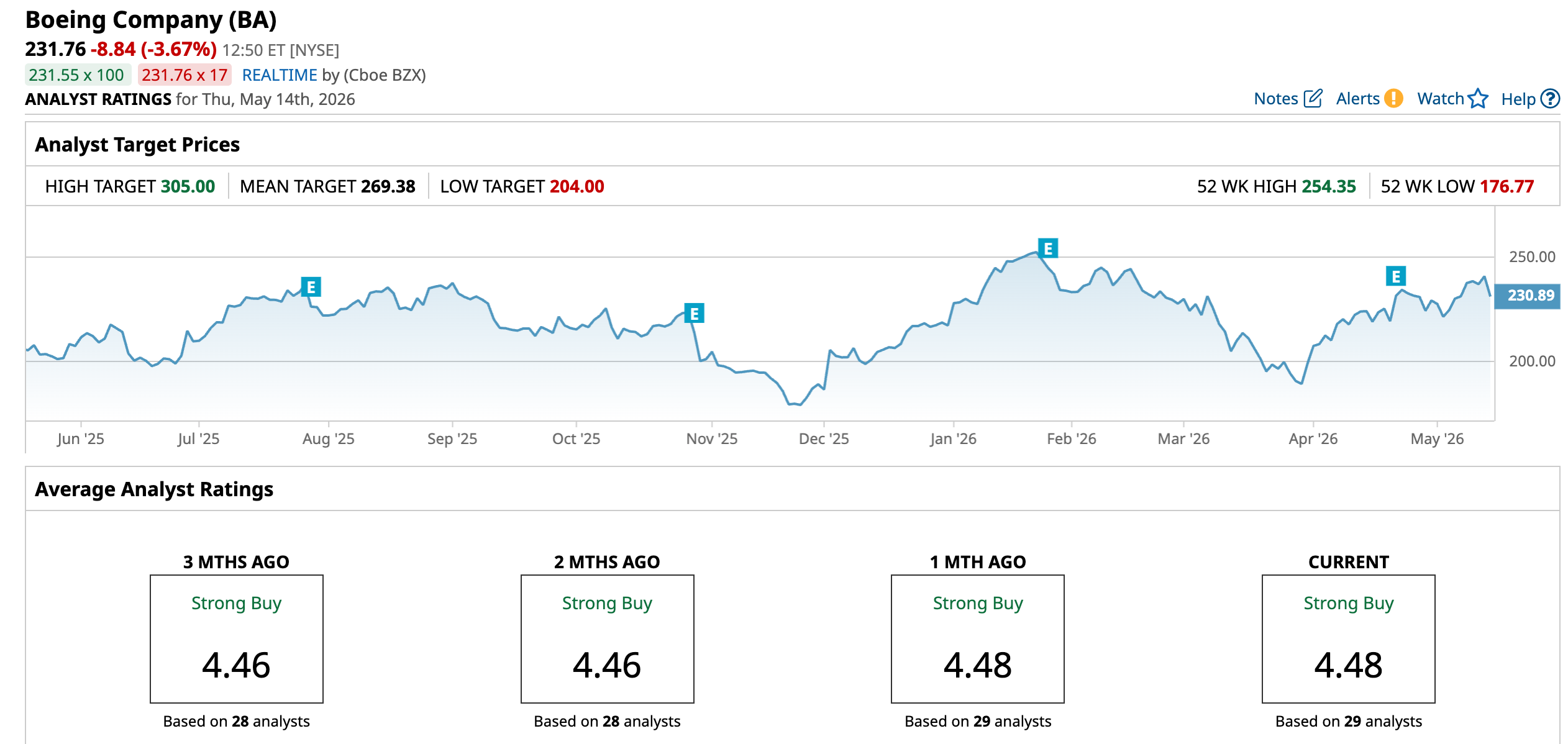

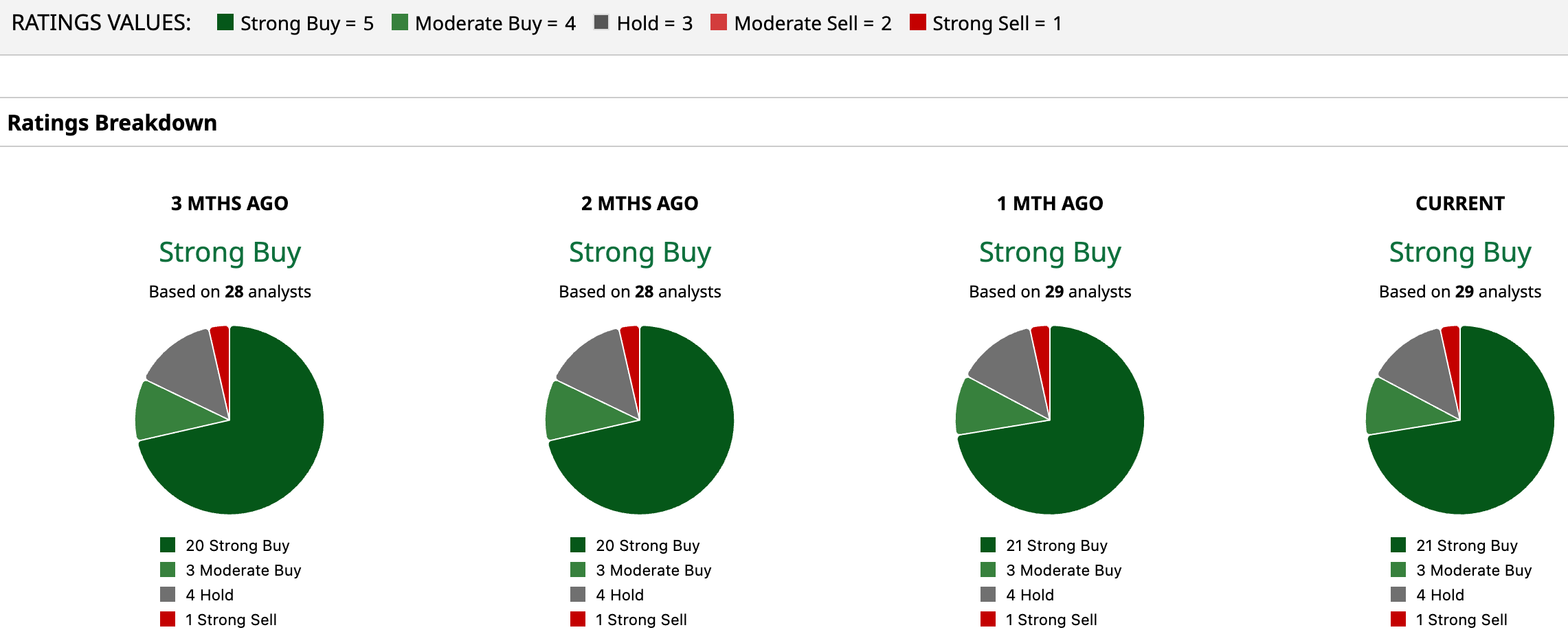

Boeing stock has a consensus “Strong Buy” rating overall. Out of 29 analysts covering the aerospace stock, 21 recommend a “Strong Buy,” three give a “Moderate Buy,” four analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

The optimism also shows up in price targets. BA’s mean target of $269.38 suggests an upside potential of 16.23%. And for the biggest bulls on the Street, the runway stretches even further. The Street-high price of $305 implies the stock could rise as much as 31.6% from here, signaling growing confidence that Boeing’s comeback may still be in its early innings.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The AI Boom Has a Power Problem. This Stock May Be the Biggest Winner. How Boeing Stock Could Be the Biggest Winner From the Trump-Xi Meetings in China As South Korea Walks Back Its AI Tax Proposal, the Brief Selloff in MU Stock Is a Non-Event Nvidia Stock Is the King of the AI Castle. History Tells Us It Will Fall Hard and Its Replacement Will Emerge From Thin Air.