Dave DAVE and Sezzle SEZL are fintech companies that target consumer-oriented payments and provide banking alternatives. While DAVE focuses on cash advances, SEZL offers interest-free installment plans at online stores.

Let us delve deeper to find out which of these two stocks investors should add to their portfolios.

The Case for DAVE

Dave’s growth is grounded in its customer-first strategy, whereby membership expansion contributes to the company’s solid financial performance. During the first quarter of 2026, the company witnessed 22% year-over-year growth in its new members to 695,000, with monthly transacting members gaining 18% year over year. Despite this sharp growth in customer base, the company managed to keep the customer acquisition cost flat year over year at $18 flat.

The company’s customer base expansion drove its first-quarter top line by 47% year over year. This impressive growth drove the company’s adjusted EBITDA by 57% year over year. Furthermore, the bottom line gained 64% year over year. Overall, the company displayed substantial operational efficiency and profitability.

With an upsurge in customer activity, ExtraCash originations surged 37% year over year. While this solid growth increased the inherent risk of credit default, the company’s proprietary AI and machine-learning-based CashAI v5.5 catered to the heightened risk. During the first quarter of 2026, Dave’s 28-day past-due (DPD) rate dipped to a record low of 1.69% from 1.7% reported in the year-ago quarter. Subsequently, the company’s net monetization rate was at 5.1%, marking the highest level achieved over the past four years.

On the liquidity front, Dave appears to hold a solid position. The company ended the first quarter of 2026 with $176 million in cash against current debt of $75 million. Furthermore, its current ratio of 3.86 surpassed the industry average of 1.57. A current ratio of more than bodes well with investors as it signals efficiency in paying short-term obligations.

The Case for SEZL

During the first quarter of 2026, Sezzle recorded remarkable growth of 37.3% year over year in its gross merchandise volume (GMV). This lofty growth led to a solid 29.2% year-over-year upsurge in the top line, which represented 12.2% of GMV. The top-line growth can also be attributed to a 34.8% year-over-year gain in Monthly On-Demand & Subscribers (MODS).

Sezzle’s noteworthy performance is fueled by the company’s customer-centric strategy that successfully boosted customer engagement. An improvement in average purchase frequency to 7.1X from the year-ago quarter’s 6.1X reflects the company’s solid customer engagement strategy. It demonstrates that customers do not use SEZL for one-off transactions, but rather utilize it for daily spending habits.

SEZL’s marketing expense more than doubled from the year-ago quarter. While this could have affected profitability, it improved operating income by 38.4% year over year. It highlights that the company’s ability to draw in customers is tied to its vigorous marketing spend without compromising scalability and efficiency. It led to a 48.4% year-over-year upsurge in active subscribers.

The company’s liquidity profile is a standout. As of the end of March 31, 2026, SEZL held cash amounting to $125 million with no current debt. Strength in its liquidity position is further evidenced by its current ratio of 3.65, an improvement from the preceding quarter’s 2.62. Furthermore, the metric exceeds the industry average of 1.1. That said, Sezzle’s current ratio is greater than 1, which is a green flag for investors as it signals efficiency in fulfilling short-term obligations.

How Do Estimates Compare for DAVE & SEZL?

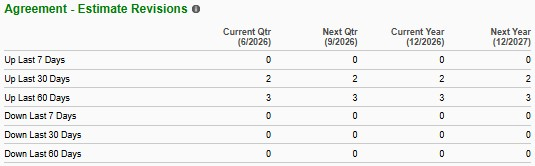

The Zacks Consensus Estimate for Dave’s 2026 revenues is $713.7 million, indicating an upside of 28.8% year over year. For 2026, the consensus mark for earnings is pegged at $15.46 per share, suggesting a 17.3% upsurge from the year-ago quarter’s actual. Over the past 60 days, three estimates for 2026 have shifted upward, with no downward revisions.

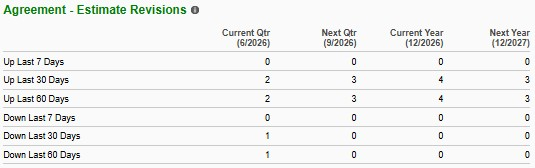

The Zacks Consensus Estimate for Sezzle’s 2026 sales is pinned at $592.6 million, implying a 31.6% year-over-year increase. The consensus estimate for earnings is pegged at $5.09 per share, suggesting a 41.8% jump from the year-ago quarter’s actual. Four estimates for 2026 have moved north in the past 60 days versus no southward revisions.

DAVE Trades Cheaper Than SEZL

Sezzle is currently trading at a forward 12-month price/earnings (P/E) ratio of 18.46, which is higher than the 12-month median of 17.24. Dave trades at a 12-month P/E ratio of 13.41, which is below the 12-month median of 21.29. This comparison highlights the fact that Dave is undervalued compared to Sezzle.

Verdict: DAVE is a Better Buy

Both Dave and Sezzle are outstanding stocks to add to your portfolio. However, Dave appears to be a better buy due to its superior financial growth and undervaluation. During the first quarter of 2026, DAVE outperformed SEZL with solid 47% year-over-year growth in its top line, fueled by a 22% year-over-year rise in members.

While the company experienced swift scaling, it maintained a customer acquisition cost of $18 and leveraged CashAI v5.5 to manage credit risk, resulting in a dip in its 28 DPD rate to a record low. Furthermore, Dave’s current ratio stands at 3.86, hinting at a stellar liquidity position. Notably, Dave trades at a cheaper price than SEZL, making it an undervalued gem and providing investors with a high-growth opportunity as the market realizes the stock’s true potential.

SEZL and DAVE sport a Zacks Rank #1 (Strong Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dave Inc. (DAVE): Free Stock Analysis Report

Sezzle Inc. (SEZL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).