The Western Union Company WU is benefiting from its diversified product base and expanding digital ecosystem, the strong performance of the Consumer Services and the Branded Digital businesses and strategic acquisitions and partnerships. Its forward P/E of 4.52X is significantly lower than the industry average of 16.32X. The company has a Value Score of A.

Western Union — with a market capitalization of $2.6 billion — is a global financial service provider that specializes in fast, secure cross-border money transfers, payments and digital financial services across 200+ countries and territories. In the year-to-date period, shares of WU have fallen 11.4% compared with the industry’s 15.5% decline.

Courtesy of solid prospects, WU currently carries a Zacks Rank #3 (Hold).

Let’s delve deeper.

Where Do Estimates for WU Stand?

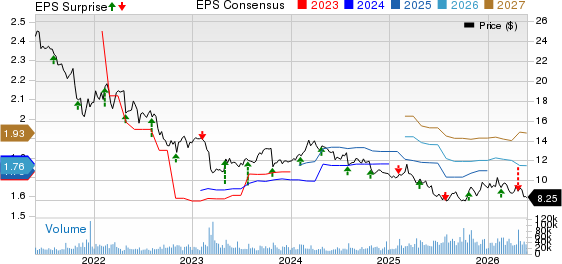

The Zacks Consensus Estimate for Western Union’s 2026 earnings is pegged at $1.76 per share, which has remained stable over the past seven days. The consensus mark for revenues is pinned at $4.3 billion for 2026, implying a 5.2% year-over-year rise. WU beat earnings estimates in two of the trailing four quarters and missed twice.

The Western Union Company Price, Consensus and EPS Surprise

The Western Union Company price-consensus-eps-surprise-chart | The Western Union Company Quote

WU’s Growth Drivers

Western Union’s growth strategy is increasingly centered on digital expansion and higher-value consumer services. In the first quarter of 2026, the company reported 9% year-over-year growth in branded digital revenues alongside a 21% rise in digital transactions, highlighting continued momentum in online remittances and account-to-account transfers. Consumer Services revenues also climbed 24%, supported by the expansion of the Travel Money business and stronger bill payment activity.

The company is accelerating its expansion strategy through acquisitions, retail partnerships and digital wallet development. The pending Intermex acquisition is expected to strengthen WU’s retail network across the Americas, while acquisitions such as Dash in Singapore and Lana in Mexico are enhancing its wallet ecosystem and cross-border payment capabilities. The company is integrating these platforms into its Beyond infrastructure to support faster wallet-to-wallet transfers, lower payout costs and broader international reach. Partnerships with Kroger, Deutsche Post and Canada Post are also expanding WU’s retail footprint and improving customer access across key markets.

Western Union is focusing on technology modernization and digital asset innovation. The rollout of USDPT, the Digital Asset Network and Stable Cards is expected to improve settlement efficiency, enabling real-time cross-border transactions and offering customers new payout options. It is also investing in cloud migration, AI-driven automation and platform modernization to reduce operating costs and improve productivity.

Western Union remains committed to enhancing shareholder value through dividends and share buybacks. Its current dividend yield is 11.4%, significantly higher than the industry average of 0.8%. In the first quarter of 2026, the company rewarded its shareholders with share buybacks worth $45 million and paid dividends of $74 million.

WU’s Key Risks

There are some factors that investors should keep a careful eye on.

Western Union continues to face pressure in its Americas retail business, where weaker transaction trends and lower fixed cost coverage are weighing on profitability. The Consumer Money Transfer segment revenues slipped 3% year over year in the first quarter of 2026.

WU’s levered balance sheet is concerning. Its total debt-to-total capital of 74.2% at the first-quarter end is significantly higher than the industry’s figure of 46.2%. Debt outstanding as of March 31, 2026, was $2.6 billion, above its cash balance of $909.2 million. Also, its return on invested capital (ROIC) of 8.7% is much lower than the industry average of 23.3%.

Key Picks

Some top-ranked stocks in the business services space are Sezzle Inc. SEZL, Dave Inc. DAVE and Priority Technology Holdings, Inc. PRTH, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Sezzle’s current-year earnings is pinned at $5.09 per share and has witnessed four upward revisions in the past 30 days against no movement in the opposite direction. Sezzle beat earnings estimates in each of the trailing four quarters, with the average surprise being 17.4%. The consensus estimate for current-year revenues is pegged at $592.6 million, implying 31.6% year-over-year growth.

The Zacks Consensus Estimate for Dave’s current-year earnings is pinned at $15.46 per share and has witnessed two upward revisions in the past 30 days against no movement in the opposite direction. Dave beat earnings estimates in each of the trailing four quarters, with the average surprise being 45.8%. The consensus estimate for current-year revenues is pegged at $713.7 million, implying 28.8% year-over-year growth.

The Zacks Consensus Estimate for Priority Technology’s current-year earnings is pinned at $1.24 per share and has witnessed one upward revision in the past 30 days against no movement in the opposite direction. Priority Technology beat earnings estimates in two of the trailing four quarters and missed twice, with the average surprise being 4.4%. The consensus estimate for current-year revenues is pegged at $1 billion, implying 8.5% year-over-year growth.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Western Union Company (WU): Free Stock Analysis Report

Dave Inc. (DAVE): Free Stock Analysis Report

Priority Technology Holdings, Inc. (PRTH): Free Stock Analysis Report

Sezzle Inc. (SEZL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).