Mama’s Creations, Inc. MAMA is building a bigger story than a single legacy brand. The company is scaling a refrigerated, deli-prepared foods platform that can serve multiple retailer needs from one supplier.

Fiscal 2026 results reflected that momentum, with net sales up 39.2% to $171.7 million as distribution widened, velocities improved, and the September 2025 Crown 1 Foods acquisition added scale.

MAMA’s Deli Platform in One Minute

Mama’s Creations manufactures and distributes fresh deli-prepared foods sold through more than 12,000 grocery, mass, club, and convenience stores in the United States. Products are primarily merchandised in supermarket delis and prepared-food sections, including grab-and-go formats, salad bars, hot bars, and sandwich counters.

What stands out in 2026 is the shift in positioning. The company began with the MamaMancini’s brand and Italian family recipes, but it has broadened into a multi-brand refrigerated prepared-food platform. Today, the mix spans all-natural meatballs, meat loaf, sausage, chicken entrées, salads, olives, paninis, sandwiches, and ready-to-heat meals.

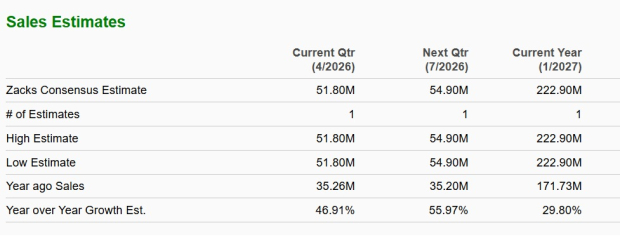

Image Source: Zacks Investment Research

Mama’s Creations Brands Broaden the Deli “Basket”

The portfolio is designed to cover multiple deli occasions, which matters when retailers want fewer, more capable suppliers. MamaMancini’s anchors the lineup with protein-centric Italian-style entrees and clean-ingredient positioning. T&L Creative Salads brings gourmet salads and deli items. Olive Branch adds olives and other savory prepared products.

Crown 1 Foods expands the basket further with value-added proteins, premium ready-to-heat meals, and modified-atmosphere packaging technology, along with strong retailer relationships across bulk and single-serve formats. Put together, this breadth supports more shelf presence across the deli set, not just a single “slot.”

MAMA’s National Distribution Push Is the Core Catalyst

Distribution expansion is the most direct growth lever in 2026. The company is gaining placements across grocery, mass, club, and convenience channels, supported by new item placements and promotions. Walmart has added eight branded stock keeping units into as many as 2,000 stores, Target is ramping toward roughly 2,000 stores, and Food Lion is already at about 1,200 stores.

Management’s goal of adding a net two stock keeping units across top accounts is important because it is designed to compound. More items at existing retailers can drive repeatable reorders as velocities build and replenishment normalizes, rather than relying only on one-time launches. It also helps diversify the geographic mix beyond the company’s Northeast roots.

For context, Walmart WMT carries a Zacks Rank #3 (Hold), underscoring how competitive and performance-driven national shelf space can be. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Mama’s Creations Rides Deli-Prepared Food Tailwinds

The demand backdrop remains supportive. Consumers are increasingly shifting meal occasions toward grocery prepared foods as restaurant inflation remains meaningfully above grocery inflation. Retailers are also investing in grab-and-go deli offerings because they can drive traffic, increase basket size, and reduce labor needs.

Mama’s portfolio is aligned with that setup because it is protein-centric and ready-to-eat, fitting the convenience-driven deli occasion. The company is also positioning itself as a national “one-stop-shop” deli solutions provider, which can resonate with large retailers looking to simplify their prepared-food supplier base.

MAMA’s Innovation Engine Expands Doors and Occasions

Innovation is becoming a more material growth driver, especially as retailers look for differentiated, labor-saving solutions. Recent launches include chicken-based meals-for-one, paninis, stuffed meatballs, premium deli proteins, and new refrigerated meal offerings tailored to retailer needs.

Paninis, in particular, significantly exceeded early expectations and expanded into more than 2,000 doors. That kind of success matters because it can unlock incremental shelf space and assortment expansion within existing customers, extending growth without requiring only new retailer wins. Crown 1 also adds cross-selling potential by opening premium accounts to legacy items and bringing Crown capabilities into existing relationships.

Mama's Creations, Inc. Price, Consensus and EPS Surprise

Mama's Creations, Inc. price-consensus-eps-surprise-chart | Mama's Creations, Inc. Quote

Mama’s Creations: Why Margin Improvement Is a Key “Watch”

Profitability has improved with scale, procurement leverage, and operating discipline, even as the Bay Shore facility continues ramping. Fiscal 2026 gross margin rose to 25.1%, and fourth-quarter fiscal 2026 gross margin reached 25.9%.

The margin playbook centers on centralized procurement, improved freight efficiency, in-house chicken trimming, automation, production balancing across facilities, enhanced planning systems, and labor productivity improvements as overtime declines. Over time, management targets a mid- to high-20% corporate gross margin profile. Investors should watch whether Bay Shore margins move closer to corporate targets as integration initiatives progress.

MAMA’s Key Risks Behind the Growth Story

The growth setup comes with clear risks. Input-cost volatility remains a swing factor for the Zacks Rank #4 (Sell) company, including protein, packaging, and freight, and pricing may not always reset immediately in competitive grocery channels. Customer concentration is also meaningful, with two customers accounting for approximately 38% and 17% of fiscal 2026 gross revenue.

Quarterly results can be uneven due to club rotations, multi-vendor mailers, and promotional timing, which can lift one period and create tougher comparisons later. Execution risk is another watch item as the company balances production and systems across a three-facility network and works to improve Bay Shore profitability through procurement savings, logistics optimization, throughput gains, and rationalization.

A simple “what would you notice first” framing is volatility in quarterly performance: mix shifts, heavier promotions, or softer gross margin progression tied to commodity and freight swings. For comparison, Tyson Foods TSN, another protein-exposed name, currently holds a Zacks Rank #2 (Buy), highlighting how fast sentiment can move in categories sensitive to input costs and margin swings.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT): Free Stock Analysis Report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).