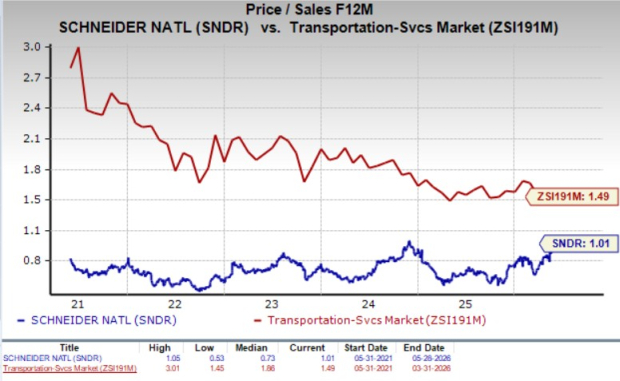

Schneider National, Inc. (SNDR) looks cheap from a valuation standpoint. Considering the forward 12-month price-to-sales ratio (P/S-F12M), Schneider is trading at a discount compared to the industry.

The stock has a forward 12-month P/S-F12M of 1.01X compared with 1.49X for the industry over the past five years. These factors indicate that the stock’s valuation is attractive. Schneider has a Value Score of B.

Schneider P/S Ratio (Forward 12 Months) Vs. Industry

Now, the question is whether it is worth buying, holding, or selling the Schneider stock at current prices. Let us delve deeper to find out.

Tailwinds Working in Favor of Schneider Stock

Schneider’s management provided upbeat full-year 2026 earnings guidance. The company expects 2026 adjusted earnings per share (EPS) to be in the range of 70 cents to $1.00, which is above the 2025 adjusted EPS of 63 cents. The upside is expected to have been aided by the cost reduction initiatives. With the successful attainment of the cost savings target in 2025, SNDR is hopeful to achieve another $40 million in targeted cost savings in 2026. SNDR aims to boost its earnings by leveraging productivity and asset efficiency actions while improving the topline without incremental growth investments. The Zacks Consensus Estimate is currently pegged at 90 cents per share.

Schneider’s solid balance sheet increases financial flexibility. The company ended first-quarter 2026 with cash and cash equivalents of $227.8 million, along with the current debt level of $10.7 million. This implies that the company has sufficient cash to meet its current debt obligations. Further, SNDR’s long-term debt has declined to $388.1 million at first-quarter 2026-end from $565.8 million at the end of first-quarter 2025.

A strong balance sheet enables the company to reward shareholders with dividends and share repurchases. As a reflection of its shareholder-friendly stance, in 2022, 2023 and 2024, SNDR paid dividends of $55.7 million, $63.6 million and $66.6 million, respectively. As of March 31, 2026, the company had returned $17.1 million in the form of dividends to shareholders year to date.

SNDR is also active on the buyback front. In January 2026, SNDR's board of directors approved a new stock repurchase program, effective immediately, under which up to $150 million of the company’s outstanding Class A common stock, and/or Class B common stock, may be acquired over the next three years. This share buyback program supersedes and replaces the $150 million stock repurchase authorization approved by SNDR's board on Jan. 31, 2023 (the “Prior Repurchase Program”), which was scheduled to expire on Jan. 31, 2026, and is substantially similar to the Prior Repurchase Program.

SNDR repurchased 4.4 million shares for a total of $110.1 million under the Prior Repurchase Program. As of March 31, 2026, the company had repurchased a total of 0.2 million Class B shares amounting to $5.2 million under the new program. Buybacks not only reduce the total outstanding share count, thereby increasing earnings per share, but also signal management's belief in the intrinsic value of the stock. Such shareholder-friendly moves instill investor confidence and positively impact the company's bottom line.

What Do Earnings Estimates Say for Schneider?

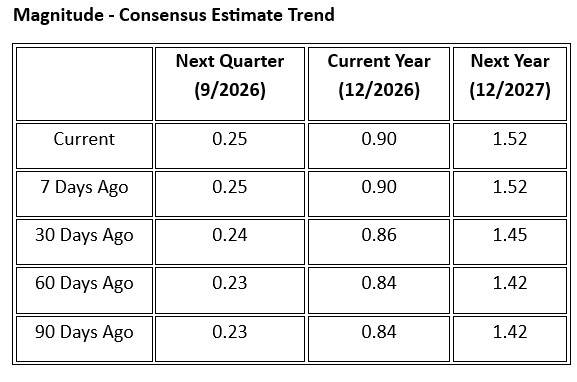

The positive sentiment surrounding Schneider stock is evident from the fact that the Zacks Consensus Estimate for the third quarter of 2026 and full-year 2026 earnings has been revised northward in the past 90 days. The consensus mark for 2027 earnings has also been projected upward in the past 90 days.

The favorable estimate revisions indicate brokers’ confidence in the stock.

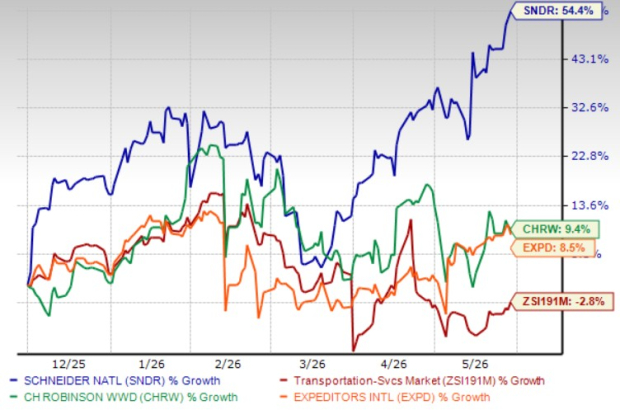

Schneider Stock’s Price Performance

Shares of Schneider have gained 54.4% over the past six months, outperforming the transportation-services industry’s 2.8% decrease, as well as that of other industry players, Expeditors International of Washington, Inc. (EXPD) and C.H. Robinson Worldwide, Inc. (CHRW).

Schneider Stock’s Six-Month Price Comparison

Headwinds Weighing on Schneider Stock

Schneider is weighed down by an increase in third-party carrier capacity costs, unplanned auto production shutdowns and raised healthcare costs. As a result, despite witnessing a decline in capital expenditures from $573.8 million at the end of 2023 to $380.3 million at the end of 2024 to $289.2 million at the end of 2025, SNDR’s 2026 expectation for capital expenditures is above the prior-year actual figures of 2024 and 2025. For 2026, net capital expenditures are expected to be in the range of $400-$450 million. A rise in capital expenditures does not bode well for the company's bottom-line growth.

Macro-economic uncertainty continues to remain an overhang. The company's bottom line is significantly affected by the ongoing inflationary environment and supply-chain disruptions, which are driving up overall costs, particularly in the insurance domain and directly impacting operating expenses. Increased insurance expense and weakness in the freight market continue to hurt SNDR’s prospects.

Schneider's segmental revenues continue to be hurt by higher maintenance costs, lower gains on the sale of assets, increased fuel expense, lower brokerage volume and lower revenue per order. Market volatility and rising costs continue to challenge SNDR, potentially impacting its growth and earnings in the near term.

Not an Opportune Time to Buy Schneider Stock

There is no doubt that the stock is attractively valued, and consistent shareholder-friendly initiatives (in the form of dividends and share buybacks), a solid balance sheet and cost reduction initiatives act as tailwinds for Schneider’s bottom-line growth.

Despite these positives, we advise investors not to buy Schneider stock now, as it continues to be hurt by an increase in third-party carrier capacity costs, unplanned auto production shutdowns, raised healthcare costs, higher maintenance costs, lower gains on sale of assets and increased fuel expense. Lower brokerage volume and lower revenue per order continue to hurt SNDR's logistics segment. The ongoing volatile macro environment marked by economic uncertainty, shifting tariff regulations and geopolitical tensions also clouds Schneider’s prospects.

Considering all these factors, we advise investors to wait for a better entry point and not buy SNDR stock now. For those who already own the stock, it will be prudent to stay invested. The company’s current Zacks Rank #3 (Hold) justifies our analysis. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

C.H. Robinson Worldwide, Inc. (CHRW): Free Stock Analysis Report

Expeditors International of Washington, Inc. (EXPD): Free Stock Analysis Report

Schneider National, Inc. (SNDR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).