The fight to control AI data centers is shaping the chip story in 2026. Nvidia Corporation (NVDA) CEO Jensen Huang thinks data center buildouts could reach $1 trillion by 2028, and that kind of money is pulling every serious player into the race.

Advanced Micro Devices (AMD) just reported Q1 data center revenue of $5.8 billion, up 57% year-over-year (YOY), and landed an OpenAI deal covering six gigawatts of computing capacity, which firmly puts it in the top tier of infrastructure suppliers. Nvidia Corporation has gone even further, rolling out its Vera Rubin Space-1 chip system at GTC 2026 for potential use in space-based data centers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Intel Corporation (INTC) now wants in on that conversation. The company plans to launch a new AI data center chip by year-end, going straight at the high-performance market, where NVDA and AMD dominate. CEO Lip-Bu Tan said back in February 2026 that Intel Corporation was building a fresh GPU effort led by Eric Demers, and at Computex 2026, it finally pulled the curtain back on Crescent Island, a new chip set to start sampling in the second half of 2026.

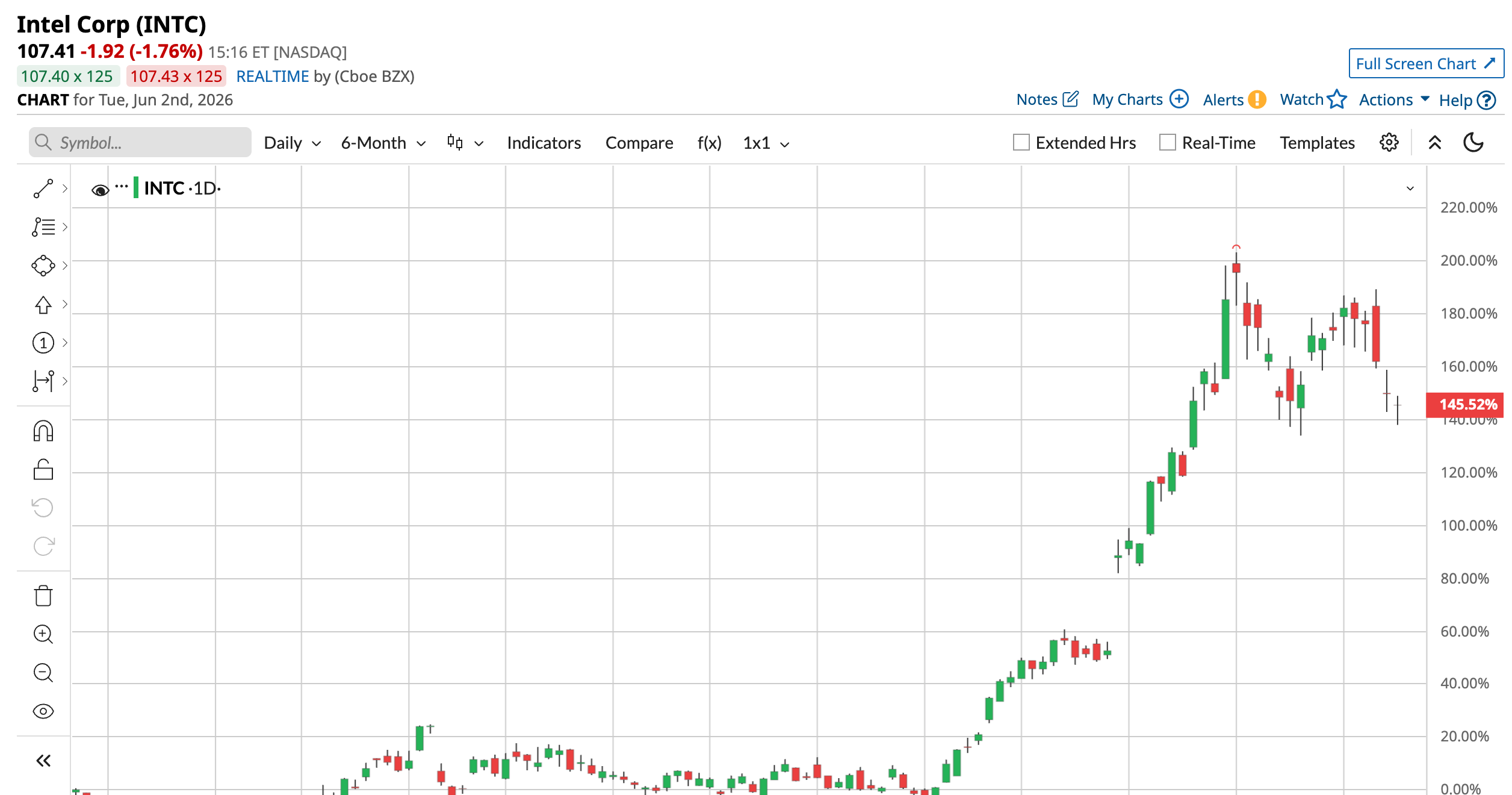

The market is already treating this as a big swing. Intel Corporation’s stock has jumped 442.9% over the past 52 weeks and is up 190.43% year-to-date (YTD), making it one of the strongest large-cap chip trades available.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com With a $5.4 trillion Nvidia Corporation on one side and a fast-climbing Advanced Micro Devices on the other, does Crescent Island turn this into a true three-way race in AI data centers, or are investors simply getting ahead of themselves on Intel Corporation’s comeback story?

Can Intel Really Challenge Nvidia and AMD?

Intel's pushback into high-end chips feels more focused. CEO Lip-Bu Tan told investors in February 2026 that the company was building a fresh GPU effort led by Eric Demers and Kevork Kechichian, with a clear target in mind: go after the data center business that Nvidia Corporation and Advanced Micro Devices now dominate.

The new chip, Crescent Island, is a data center GPU that Intel Corporation first showed in late 2025 and updated at Computex 2026, with test units expected to reach customers in the second half of 2026.

Intel has shifted the way in which it runs the business. It has been pulling capacity away from consumer PCs and leaning harder into server chips, helping lift data center revenue to $4.7 billion in the latest quarter. Work on its 18A manufacturing process and the $14.2 billion move to take full control of Fab 34 in Ireland are part of the same story: trying to convince big customers that Intel Corporation can actually build these chips at scale.

Nevertheless, the hill is still steep. Nvidia’s software and tools keep many customers locked in, while Advanced Micro Devices is already winning big cloud deals with its own accelerators. Intel Corporation’s Gaudi line never really broke through, so Crescent Island has to do more than just exist.

The bullish view is that if Intel Corporation hits its manufacturing goals, wins third-party foundry work and gets any real traction with its new GPU, there is still room for the stock to grow into its AI narrative. The cautious view is that this all costs a lot, margins are thin, and the leaders are not standing still, so Crescent Island may end up proving Intel belongs in the conversation without yet proving it can catch up.

Earnings, Street Sentiment and What Lies Ahead

Intel’s next earnings update is coming on July 23, and expectations are finally pointing in the right direction. Wall Street is looking for EPS of $0.10 for the June 2026 quarter, compared with a loss of $0.26 a year ago, which works out to 138.46% growth. Estimates then step up to $0.14 for September versus $0.11 last year (27.27% growth), and full‑year 2026 EPS is pegged at $0.63 after a loss of $0.12 in 2025, a 625% swing back into the black.

That helps explain why KeyBanc’s January call still carries weight. Analyst John Vinh lifted Intel Corporation to “Overweight” with a $60 target, pointing to real progress in the foundry business and stronger demand for server CPUs tied to big AI data center builds.

In his view, Intel Corporation does not have to win the GPU race right away to benefit; it can already make money from tighter CPU supply, better pricing and growing interest in advanced packaging while its new chip lineup ramps up.

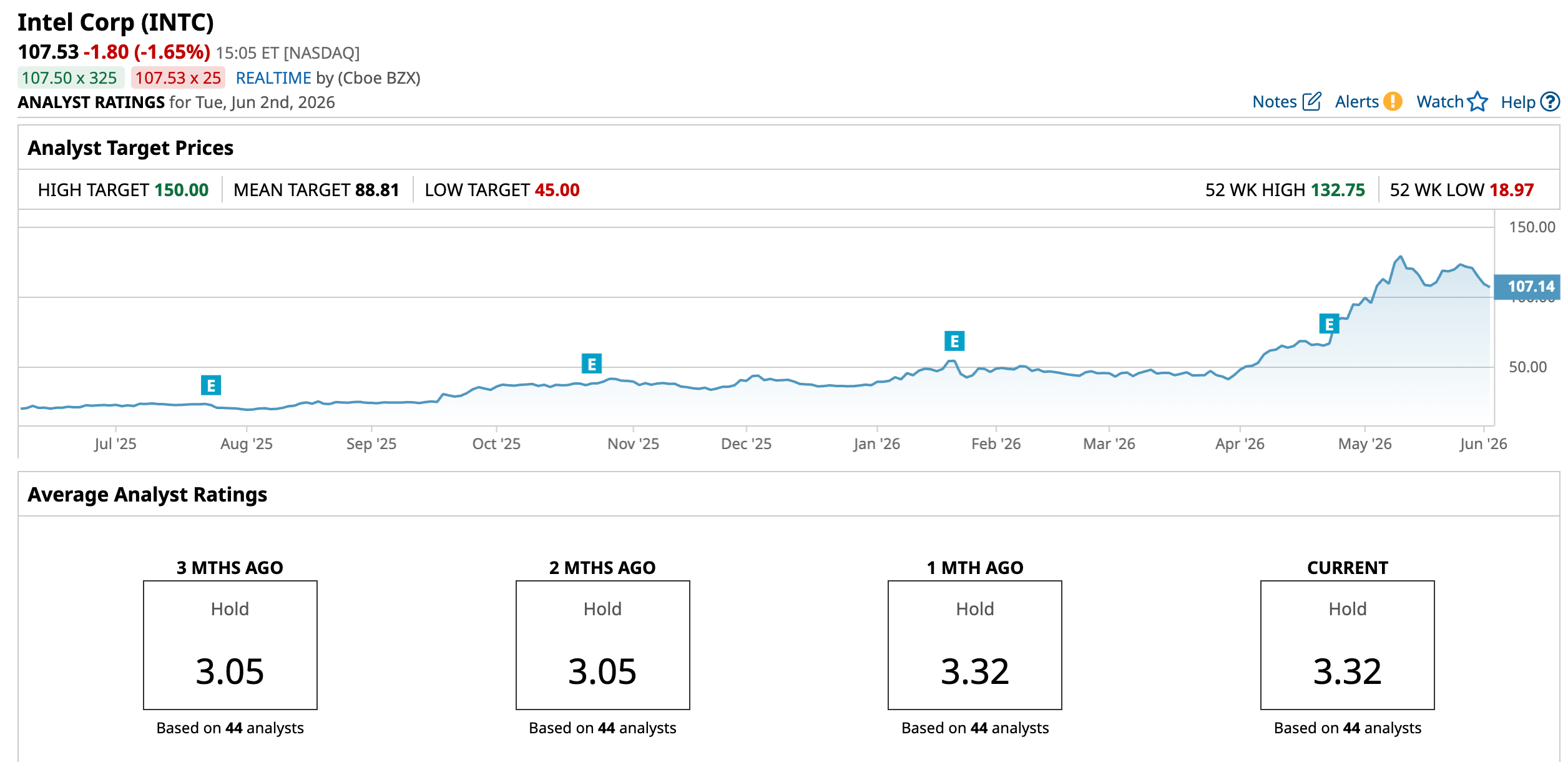

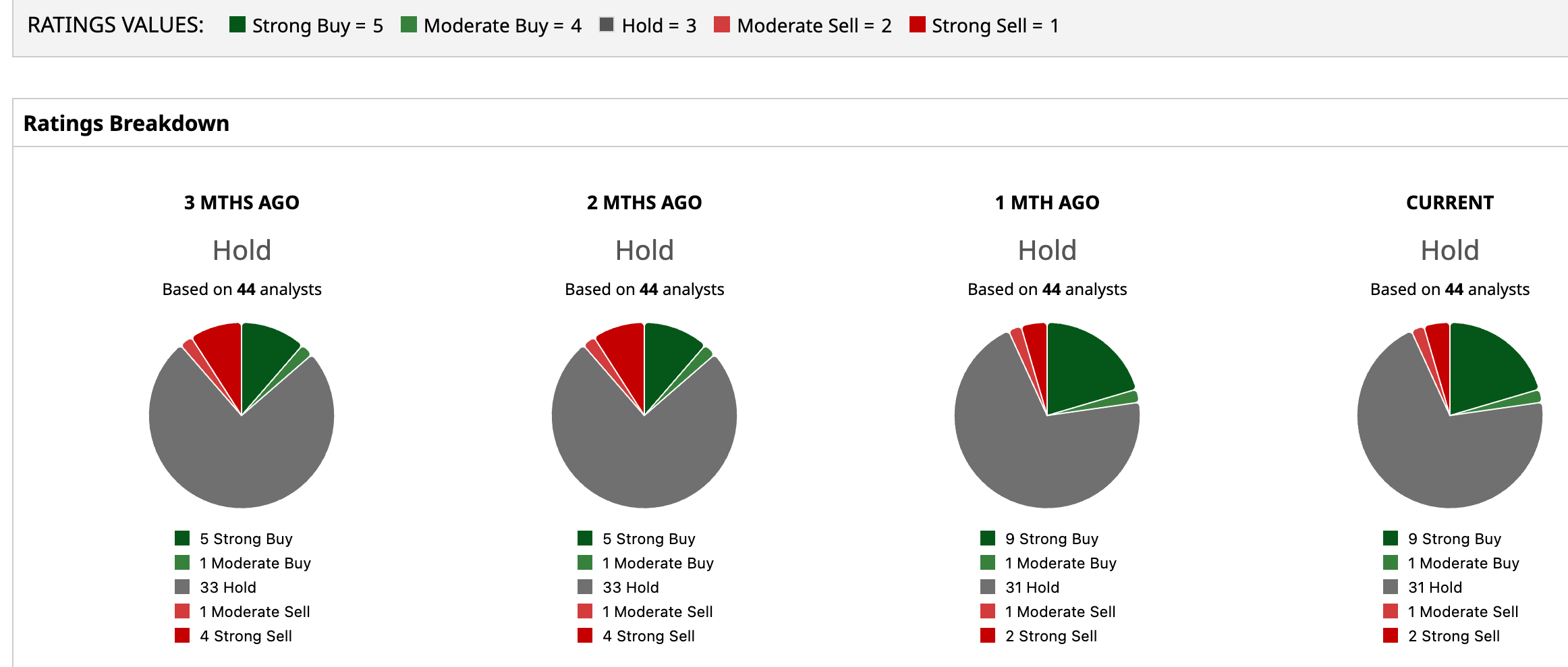

Even so, among 44 analysts covering Intel Corporation, a consensus carries a “Hold” rating, and the average price target of $88.81 represents a 17.4% downside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

In the end, Intel looks less like a sure bet to dethrone Nvidia and AMD and more like a high‑beta side door into the AI data center boom. Crescent Island and the broader GPU push show Intel is serious about claiming a slice of accelerated computing, but its real edge for now is monetizing AI indirectly through server CPUs, advanced packaging, and a slowly healing foundry story. Given how far the stock already trades above the Street’s mean target, the risk/reward skews toward volatile, expectation‑driven upside rather than a smooth grind higher, with pullbacks likely if execution stumbles or AI enthusiasm cools.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Berkshire Hathaway Agrees to Buy Taylor Morrison for $6.8 Billion. What This Means for TMHC Shareholders. Intel Sets Sights on Nvidia and AMD With Upcoming AI Data Center Chip Launch by Year End Even If Eli Lilly Stock Continues to Shine, Stay Away from This Pharmaceutical ETF Micron Stock Could Still Have Nearly 70% Upside Potential Left in Its Tank