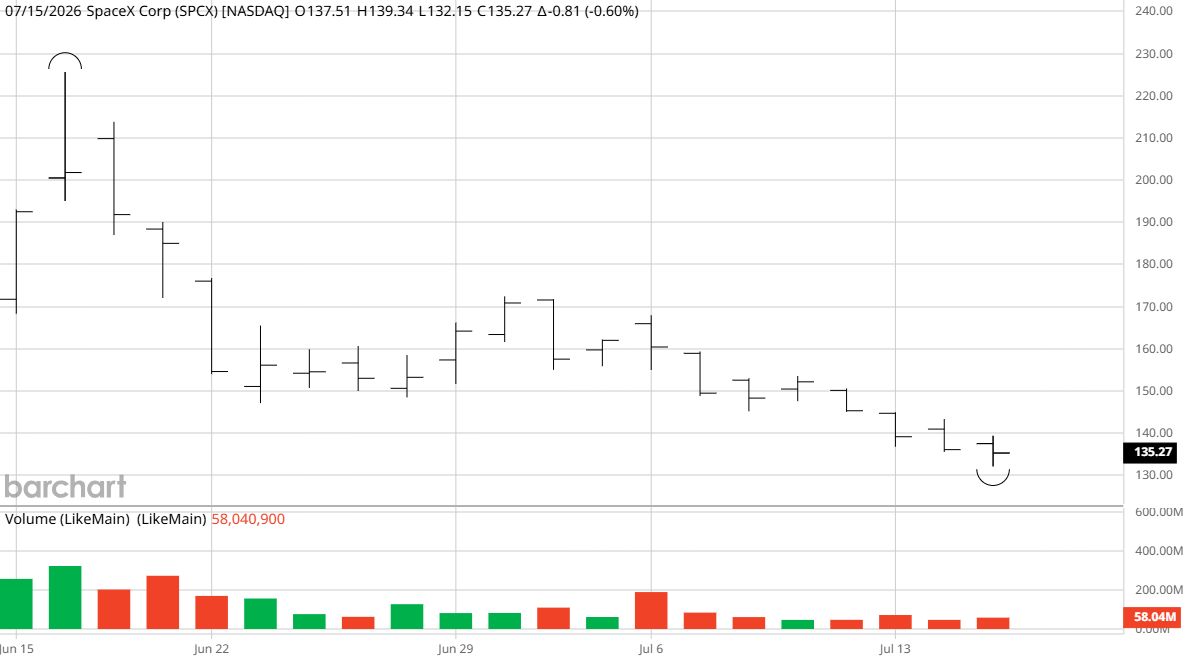

Before (SPCX) went public, I wrote that the extraordinary demand for the IPO might be the warning.

The shares, priced at $135, raced above $225 and have now completed the round trip. They briefly traded below the offering price before closing almost exactly where the story began. (SPCX) has fallen roughly 40% from its high and lost more than $1 trillion in market value in little more than a month.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The easy thing for me to do would be to take a victory lap. The more useful question is whether the stock is finally worth buying. My answer is not yet, but for the first time since the IPO, I am paying serious attention. A stock falling 40% tells you where it has been. It does not tell you what it is worth.

The IPO Price Is Not Fair Value

Investors are habituated to treating the IPO price as though it represents some natural level of support. (SPCX) was sold at $135, so when it returns to $135, it feels as though fair value has been restored. That is not how IPO pricing works.

The offering price was the number (SPCX) that its bankers and investors agreed upon during a competitive sales process. It valued the company at approximately $1.77 trillion and allowed (SPCX) to raise a record amount of capital. It was the price required to complete the deal, nothing more.

Aswath Damodaran, the NYU professor often called the dean of valuation, reached a different conclusion. After valuing (SPCX)’s launch, connectivity, and artificial intelligence businesses separately, he estimated the equity was worth around $1.3 trillion. That would place the shares closer to $100.

I would not treat any (SPCX) valuation as exact. Too much depends on businesses still being developed, markets that may not yet exist, and margins that could change dramatically. But Damodaran’s work gives investors something the excitement around the IPO did not: a sensible starting point.

The AI Assumptions Matter

His biggest concern was artificial intelligence. The launch business has a long operating history. Starlink has real customers, revenue, and improving economics. xAI is different. Investors are being asked to value a business that is further from profitability, requires giant spending, and competes against some of the best-capitalized technology companies in the world.

(SPCX)’s IPO materials described an enormous potential market for AI, most of it attached to xAI. The numbers were so large that small changes in assumed market share or future margins could move the valuation by hundreds of billions of dollars. That is where the valuation becomes difficult.

Starlink can be analyzed. It has subscribers, pricing, and an economic model that is beginning to take shape. The launch business can be studied because (SPCX) has already changed the cost and frequency of reaching orbit. With xAI, much of the value still depends on what investors think might happen years from now.

(SPCX) lost nearly $5 billion last year and spent heavily on capital expenditure and research. Much of the increase came from AI and other long-duration projects. Those investments may eventually produce extraordinary returns. They may also consume cash for years before anyone knows whether the economics work.

At $135, (SPCX) is still valued at around $1.8 trillion. Based on expected revenue, the stock trades at a multiple that would look extreme for almost any other company. There is no meaningful price-to-earnings ratio because there are no earnings.

That does not make the company uninvestable, however. It tells you how much future success remains embedded in the price. At $225, investors were paying as though almost everything would work. At $135, they are still paying a lot for things to go well.

The Price Changed the Mood

People wanted (SPCX) more at $225 than they do now. The rockets remained equally reusable. Starlink did not lose 40% of its customers. (SPCX)’s ambition did not disappear. The price changed. Then the price changed how investors felt about the company.

At the top, investors were frightened of missing out. Only a small part of (SPCX) was available in the IPO, so buyers competed for a limited number of shares. Scarcity made the stock feel more valuable, and the rising price made it feel safer. Now investors are frightened of buying too early. This is normal market behavior. A rising stock feels safer as it becomes pricier. A falling stock feels more dangerous as the prospective return improves.

In my book, Price Catalysts, I make a distinction that matters here. A lower price is not a catalyst. A stock can become cheaper and remain so. Something must change expectations, cash flow, or ownership before a valuation gap begins to close.

(SPCX) is approaching all three.

The First Public Results

The company is expected to announce its first results as a public business in early August, although it has not formally set a date. Investors should finally get a clearer view of Starlink growth, operating profitability, capital spending, and how much cash AI is consuming. Those numbers will tell us whether the business is beginning to grow into the valuation or whether it still relies too heavily on distant outcomes. The earnings report matters, but the ownership structure may matter more.

The Lockup Could Create the Opportunity

(SPCX) made less than 5% of the company available in the IPO. That scarcity helped drive the initial surge. After the first earnings report, employees and early investors may become eligible to sell hundreds of millions of shares. By December, a much larger portion of the company's shares could be made available for trading.

The IPO created too many buyers chasing too few shares. The lockup expiration may reverse that. An employee selling (SPCX) stock after holding it for years is not necessarily telling you that Starlink is slowing or Starship has failed. They may want to buy a house, pay taxes, diversify their wealth, or turn years of paper gains into cash.

That matters because the seller may not care about fair value. They may simply want liquidity. I avoided (SPCX) when investors were fighting to get in. I may become interested when existing holders can finally get out.

What I Need Before Buying

The level I am watching is around $100. That would place (SPCX) close to Damodaran’s $1.3 trillion valuation. It would not make the shares conventionally cheap, but it would remove much of the IPO premium and nearly all the speculative premium from the first days of trading. I would still need evidence.

The best setup would be healthy Starlink growth, stronger cash generation, and discipline around AI spending, followed by lockup selling that pushes the shares lower without any corresponding deterioration in the business. That would provide me valuation, forced selling, and a reason for the pressure to end.

I would also consider buying above $100 if the initial public results materially improve the valuation case. If Starlink is growing faster than expected, margins are stronger, and (SPCX) can fund Starship and AI without continually returning to shareholders for capital, fair value can move higher.

But if Starlink disappoints, cash burn accelerates, or the company continues to spend heavily on AI without showing credible economics, even $100 may not be cheap. One price should never replace the work.

Damodaran also warned that mood and momentum could heavily drive (SPCX). The shares may rise even when the valuation does not support them. They could also fall below reasonable value when insider selling, disappointment, and fear arrive together. That is what I am watching for. (SPCX) is one of the most remarkable companies I have studied. But great companies can still be bad investments when the price assumes too much.

At $225, the story controlled the price. At $135, the valuation became part of the discussion. Near $100, with Starlink intact and forced selling underway, I would be ready to act.

On the date of publication, Jim Osman did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Quantinuum Just Struck a New Deal with Rolls-Royce. What That Means for QNT Stock Here. Why Jim Cramer Is Telling Retail Investors to Stay Far Away from the IBM Stock Dip Reddit Just Scored a New 'Outperform' Rating. What Comes Next for RDDT Stock. SpaceX Is Back at Its IPO Price. Here Is When I Would Buy It.