WM WM is benefiting from continued demand for its robust infrastructure and extensive asset network, including landfills, recycling facilities and waste-to-energy plants. The company’s strategic acquisitions, pricing and cost-control strategies boost operational efficiency and profit margins. WM stock’s steady returns, low volatility and the company’s shareholder-friendly policies are added advantages.

However, low liquidity and high debt dampen profitability, scalability and overall financial performance. The stock lacks momentum, making it less attractive to momentum investors who often seek higher short-term returns.

How Is WM Faring?

WM’s robust waste collection, recycling and disposal infrastructure enables it to maintain good, long-standing customer relationships and steady revenues. The company provides collection, transfer, recycling, resource recovery and disposal services to residential, commercial, industrial and municipal customers. WM ensures sustainable, long-term growth while building competitive advantages by leveraging its extensive network of assets, including landfills, recycling facilities and waste-to-energy plants, to offer advanced recycling solutions and produce renewable energy.

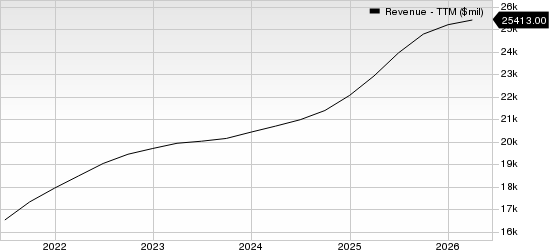

Waste Management, Inc. Revenues (TTM)

Waste Management, Inc. revenue-ttm | Waste Management, Inc. Quote

The company is focused on its pricing and cost control strategies. WM ensures that price adjustments are aligned with the quality, reliability and demand for the services. It optimizes routes, enhances service delivery and improves operational processes. WM also integrates modern technology and process improvements to reduce costs and boost service reliability and customer satisfaction.

WM pursues acquisitions to drive growth. It recently acquired Stericycle, which specializes in collecting and disposing of regulated medical waste, such as sharps, pharmaceuticals and controlled substances, trace chemotherapy waste and pathological waste. This acquisition has provided a complementary platform in the medical waste sector with robust growth dynamics.

The company offers steady returns and low volatility due to the essential nature of waste management services. This appeals to long-term investors and those seeking stability during market fluctuations. WM has embraced sustainability initiatives and innovation, such as converting landfill gas into renewable energy, which solidifies its growth prospects.

WM consistently rewards its shareholders through constant dividend payments despite fluctuations in its cash position. It paid dividends of $1.1 billion, $1.2 billion and $1.3 billion in 2023, 2024 and 2025, respectively. This demonstrates the company’s dedication to creating long-term value for investors.

Meanwhile, WM operates in a stable industry with consistent demand, resulting in steady but modest stock price movements. This enables it to generate stable revenues and incremental growth, but it lacks explosive growth. Therefore, the stock may not be ideal for momentum investors.

The company's recent acquisitions and ongoing investments in renewable energy have significantly increased its debt load. WM must allocate a portion of its cash flow to service these debts, including interest payments and principal repayment. This dampens the bottom line and operational performance.

WM’s current ratio (a measure of liquidity) at the end of the first quarter of 2026 was 0.93, lower than the industry average of 1.08. A current ratio below 1 often indicates that the company may not be well-positioned to pay off its short-term obligations.

WM reported mixed first-quarter 2026 results. It earned an adjusted profit of $1.81 per share, which topped the Zacks Consensus Estimate by 3.4% and increased 8.4% from the year-ago quarter’s level. Revenues of $6.23 billion missed the consensus estimate by 1.1% but rose 3.5% year over year.

WM currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings Snapshots of Some Players

Rollins, Inc. ROL reported impressive first-quarter 2026 results. ROL’s adjusted earnings of 24 cents per share matched the consensus mark and rose 9.1% from the year-ago quarter. ROL’s total revenues of $906.4 million surpassed the consensus mark by 1.3% and increased 10.2% year over year.

Equifax Inc. EFX reported better-than-expected first-quarter 2026 results. EFX’s adjusted earnings per share of $1.86 beat the Zacks Consensus Estimate by 10.1% and increased 21.6% from the year-ago quarter. EFX’s revenues of $1.6 billion surpassed the consensus estimate by 2.3% and improved 14.4% year over year.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Equifax, Inc. (EFX): Free Stock Analysis Report

Waste Management, Inc. (WM): Free Stock Analysis Report

Rollins, Inc. (ROL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).