Murphy USA's MUSA merchandise business is increasingly being driven by one category, nicotine. While discretionary consumer spending remains under pressure, the company's nicotine offerings continue to generate strong sales and higher-margin profits, helping offset weakness in other in-store categories. Recent results indicate that nicotine has evolved beyond a traffic driver into one of Murphy USA's most significant earnings contributors.

During the first quarter, MUSA reported merchandise contribution of $210.2 million, up 7.3% year over year. On a same-store basis, merchandise contribution increased 4.9%, supported by both higher sales and expanding unit margins, which improved to 20.0% from 19.6% in the prior-year quarter. Nicotine remained the standout performer, with same-store contribution rising 11.5%, far exceeding the 2.7% growth recorded in non-nicotine merchandise. Management noted that nearly every merchandise metric benefited from nicotine's continued strength, while discretionary categories such as snacks and other non-essential products remained soft as consumers carefully managed household budgets.

Murphy USA's value-focused operating model has further reinforced this trend. Management highlighted that elevated fuel prices have attracted more value-conscious customers to its stores, creating additional opportunities for nicotine purchases. Unlike discretionary merchandise, nicotine products typically experience more stable demand regardless of broader economic conditions. As a result, the category continues to provide MUSA with a dependable source of inside-store profitability even as the retail environment remains cautious.

MUSA Stands Out Among Peers

MUSA is not the only convenience retailer benefiting from nicotine demand, but the category appears to be contributing more meaningfully to the recent merchandise growth than it does for several competitors.

Casey's General Stores CASY has expanded its assortment of cigarettes, modern oral nicotine products and other tobacco offerings. However, Casey's still relies heavily on prepared food and beverages as its primary engine for inside-store sales growth. While nicotine remains an important category, the company's long-term strategy is centered on foodservice expansion, resulting in a more diversified merchandise mix.

ARKO Corp. ARKO also generates a portion of its in-store sales from tobacco and nicotine products. Similar to MUSA, ARKO serves value-oriented consumers and views tobacco as an important traffic driver. At the same time, the company has been investing in foodservice, loyalty programs and private-label products to reduce its dependence on traditional tobacco categories. Compared with ARKO, MUSA's latest results suggest nicotine remains a more immediate catalyst for merchandise margin expansion, supported by robust demand for modern nicotine products and its everyday low-price strategy.

Although Casey's and ARKO both recognize nicotine as an important merchandise category, MUSA currently appears to be extracting greater earnings leverage from the segment, helping offset softer discretionary spending while supporting stronger merchandise contribution growth.

Valuation and Earnings Outlook Remain Favorable

MUSA's long-term outlook remains supported by resilient nicotine demand, continued retail expansion and disciplined execution. While non-nicotine discretionary categories could recover as consumer spending improves, nicotine currently provides the company with a stable source of higher-margin merchandise contribution and strengthens earnings resilience.

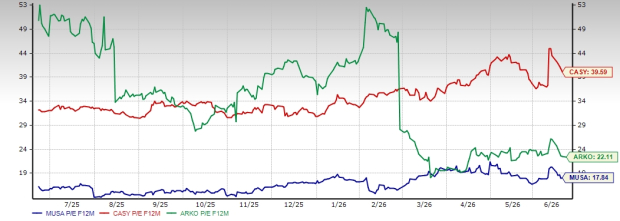

The stock also appears attractively valued relative to its growth prospects. MUSA trades at a forward price-to-earnings ratio of 17.84, well below Casey's 39.59 and ARKO's 22.11.

Image Source: Zacks Investment Research

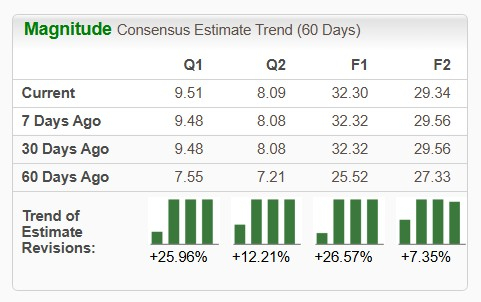

Analysts have also become increasingly optimistic about the company's earnings trajectory, raising 2026 EPS estimates by 26.57% and 2027 estimates by 7.35% over the past 60 days.

Image Source: Zacks Investment Research

From a stock performance perspective, MUSA has delivered solid returns but has trailed some peers. Over the past six months, ARKO’s shares have surged 60.9%, outperforming Casey's and MUSA, which gained 46.7% and 35.5%, respectively.

Image Source: Zacks Investment Research

Murphy USA's combination of attractive valuation, strong earnings momentum and nicotine-driven merchandise growth supports its favorable long-term outlook. MUSA currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Murphy USA Inc. (MUSA): Free Stock Analysis Report

Casey's General Stores, Inc. (CASY): Free Stock Analysis Report

ARKO Corp. (ARKO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).