H.B. Fuller Company FUL is no longer just a broad specialty chemicals story. The investment debate now centers on whether a cleaner portfolio, stronger pricing discipline and medical expansion can support steadier margins.

That setup looks constructive, but not one-sided. Softer consumer-linked demand, flexible packaging weakness and automotive pressure still limit the near-term volume story.

How FUL Is Reshaping Its Business

Following its fiscal 2025 realignment and the sale of the North America Flooring business, H.B. Fuller reports through three segments: Hygiene, Health & Consumable Adhesives, Engineering Adhesives and Building Adhesive Solutions.

The mix spans packaging, converting, hygiene, healthcare, transportation, electronics, clean energy, aerospace, appliances, roofing, building envelope, HVAC insulation and infrastructure. The strategic direction is clear. FUL is shifting toward more resilient and higher-value niches instead of relying mainly on raw volume growth.

H. B. Fuller Company Price and Consensus

H. B. Fuller Company price-consensus-chart | H. B. Fuller Company Quote

H.B. Fuller Pricing Still Drives Results

Pricing remains the clearest support for the current thesis. In the fiscal second quarter, net revenues rose 5.8% year over year to $950 million, while organic revenues increased 2.6%, helped by pricing that more than offset slightly lower volume.

Margin execution was also stronger. Adjusted gross margin expanded 200 basis points to 34.2%, driven mainly by pricing execution and restructuring savings. Adjusted EBITDA rose 9% to $181 million, while adjusted EBITDA margin improved 70 basis points to 19.1%.

Why FUL Still Faces Demand Friction

The weaker side of the story is volume. The Hygiene, Health & Consumable Adhesives unit saw strength in medical, tape and label and end-of-line packaging, but flexible packaging remained weak.

Engineering Adhesives also had mixed trends. Aerospace, electronics and general industries were stronger, but automotive declined by mid-single digits. These pressures leave earnings more dependent on price, mix, sourcing and cost control than on a broad-based volume recovery.

Avery Dennison Corporation AVY gives investors another way to look at materials tied to packaging and labeling demand. RPM International Inc. RPM, with exposure to specialty coatings, sealants and building materials, is also relevant for investors tracking construction-linked materials trends.

What H.B. Fuller Expects Next

For fiscal 2026, H.B. Fuller still expects net revenues to increase in the mid-single digits and organic revenues to rise in the low single digits. Foreign currency translation is expected to add 1-2% to revenues.

Management now expects adjusted EBITDA of $650-$675 million and adjusted earnings of $4.60-$4.90 per share. Operating cash flow is projected at $300-$325 million, with cash generation weighted to the second half of the year.

FUL Signals for Momentum and Value

The bottom line is that FUL has a credible margin story, but it still needs to prove that pricing, restructuring and mix can offset uneven end-market demand. The proposed Advanced Medical Solutions acquisition adds another potential higher-margin growth platform, but it also brings integration and leverage considerations.

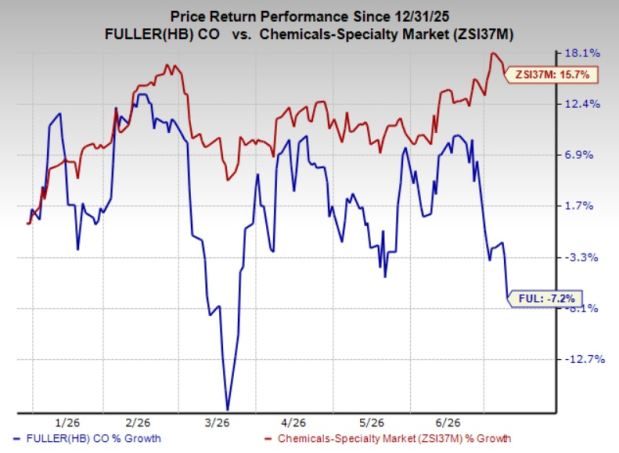

Shares of FUL have lost 7.2% so far this year against the industry’s 15.7% rise.

Image Source: Zacks Investment Research

FUL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also has a VGM Score of A, with a Value Score of A, Momentum Score of A and Growth Score of C. That combination points to favorable value and momentum characteristics, while the Growth Score signals that growth questions have not fully disappeared.

Estimate revisions also remain supportive, with the current fiscal-year earnings estimate up 2.1% over the past four weeks. For investors, FUL looks best framed as a margin-and-mix execution story, not a simple volume recovery play.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

H. B. Fuller Company (FUL): Free Stock Analysis Report

Avery Dennison Corporation (AVY): Free Stock Analysis Report

RPM International Inc. (RPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).