Revolve Group, Inc.’s RVLV international business continues to gain momentum, reinforcing its position as an important contributor to the company’s long-term growth strategy. During the first quarter of 2026, international net sales increased 20% year over year to $68.9 million, outpacing domestic growth of 15%. Notably, this marked the 13th consecutive quarter in which international growth outpaced the U.S. business, highlighting the strength of Revolve Group’s expanding global footprint.

The company’s localized merchandising and marketing initiatives are driving stronger customer engagement across key international markets. Management highlighted exceptional momentum in Mexico, where enhanced service levels and a localized marketing strategy helped drive customer growth of more than 80% year over year. This performance demonstrates the effectiveness of tailoring the customer experience to local market preferences while supporting broader international expansion.

International growth also remained resilient despite macroeconomic and geopolitical challenges. Management noted that the business delivered healthy international performance even as demand in the Middle East was affected by geopolitical tensions, underscoring the strength of consumer demand across other global markets. Broad-based double-digit growth across both the REVOLVE and FWRD platforms reflects the company's ability to gain market share internationally.

Beyond digital expansion, Revolve Group is strengthening its brand through selective physical retail investments. The company recently signed a lease for its third retail store in Miami, one of its strongest U.S. markets, with plans to open the location by the end of 2026. Management believes that combining physical stores with its digital-first platform will enhance brand awareness, improve omnichannel engagement and support customer acquisition over time.

Management remains optimistic about the long-term international opportunity, identifying global expansion as one of Revolve Group’s key strategic priorities. Supported by localized merchandising, targeted marketing initiatives and continued investments in technology and customer experience, the company believes its international business is well-positioned to remain an important driver of sustainable, profitable growth.

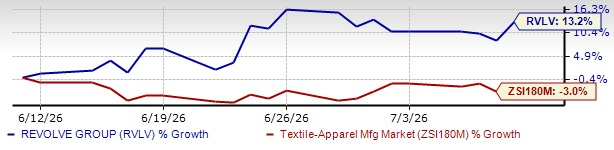

RVLV’s Price Performance, Valuation & Estimates

Shares of Revolve Group have gained 13.2% over the past month against the industry’s 3% decline.

Image Source: Zacks Investment Research

From a valuation standpoint, RVLV trades at a forward price-to-sales ratio of 1.18X, below the industry’s average of 2.31X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Revolve Group’s fiscal 2026 earnings implies a year-over-year decline of 1.2%, while the same for fiscal 2027 indicates an uptick of 10.6%. Estimates for fiscal 2026 and 2027 have been remained unchanged over the past 30 days.

Image Source: Zacks Investment Research

Revolve Group currently carries a Zacks Rank #3 (Hold).

Key Picks

Genesco Inc. GCO is a Nashville-based specialty retail and branded company. It sells footwear and accessories in retail stores. The company flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Genesco’s current fiscal-year earnings indicates growth of 55.2% from the year-ago actuals. GCO delivered a trailing four-quarter average earnings surprise of 3.8%.

Designer Brands Inc. DBI designs, produces and retails footwear and accessories. It offers shoes, boots, sandals, sneakers, socks, handbags and accessories. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Designer Brands’ current fiscal-year earnings and sales suggests growth of 137.5% and 0.5%, respectively, from the year-ago actuals. DBI delivered a trailing four-quarter average earnings surprise of 112.8%.

Tapestry, Inc. TPR is the designer and marketer of fine accessories and gifts for women and men in the United States and internationally. The company also holds a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Tapestry’s current fiscal-year earnings and sales indicates growth of 36.5% and 13.9%, respectively, from the year-ago actuals. TPR delivered a trailing four-quarter average earnings surprise of 15.6%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Revolve Group, Inc. (RVLV): Free Stock Analysis Report

Genesco Inc. (GCO): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

Designer Brands Inc. (DBI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).