nVent Electric NVT and Vertiv VRT are major players in the data center market, particularly in the rapidly growing area of AI data center infrastructure and liquid cooling solutions. While nVent Electric mainly sells electrical enclosures, connections and protection products used across industrial, commercial and infrastructure markets, including data centers, Vertiv focuses on power and cooling infrastructure for data centers.

Both NVT and VRT are positioned to benefit from long-term infrastructure and data-center investment trends. However, from an investment point of view, one stock offers a more favorable outlook than the other right now. Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which stock offers a more compelling investment case.

The Case for nVent Electric Stock

nVent Electric is benefiting from strong demand for data center infrastructure, which is becoming a major driver of its revenue growth. In the first quarter of 2026, the company reported organic sales growth of 34%, with infrastructure sales rising nearly 80% year over year. Management said data centers were the biggest contributor to growth, helping the company deliver record sales, orders and backlog.

The company is seeing demand across both gray-space and white-space data center applications. In the gray space, growth was driven by engineered buildings, enclosures and power connections. In the white space, liquid cooling, power distribution units and cable management solutions performed well. Management noted that growth was broad-based across the portfolio and supported by demand from hyperscalers, neocloud providers, multitenant operators and distribution partners.

nVent Electric's order trends also remain strong. Organic orders increased about 40% in the first quarter, largely driven by AI data center projects. Backlog reached a record $2.6 billion, rising in the low double digits sequentially. The company stated that most of its backlog extends beyond 12 months and into 2027, providing visibility into future revenues. In the first quarter, new products added more than 20 percentage points to sales growth, with many of those products tied to data center applications.

To support demand, nVent Electric is increasing capacity across its operations, which should help the company generate more revenue once fully ramped up. The company recently opened its new Blaine, MN, facility and expects production to ramp up through 2026. It is also investing in additional capacity for liquid cooling and other data center products. Overall, the above-mentioned factors show that data center demand is likely to remain an important revenue growth driver for the company.

The Case for Vertiv Stock

Vertiv continues to benefit from strong spending on AI data centers. During the first-quarter 2026 earnings call, management stated that customers are moving ahead with larger AI projects and demand remains strong across its key markets. The company's pipeline continues to grow, and orders are expected to increase in 2026. The Americas remained the strongest market, while demand remains healthy across India, the rest of Asia and China. Management stated that the AI infrastructure build-out is still in its early stages, which should support demand over the long term.

To meet this demand, Vertiv is increasing investments across its business. The company is expanding manufacturing capacity for power management, cooling products, infrastructure solutions and IT systems. During the first quarter, Vertiv completed the acquisition of PurgeRite, which strengthens its liquid cooling services. Further, VRT is also adding more engineers, increasing service capacity and expanding testing facilities. These investments should support higher customer demand and increase production capacity.

Vertiv is also expanding its product portfolio to address changing AI data center requirements. The company said customers are increasingly adopting integrated solutions such as OneCore and SmartRun, which combine power, cooling and infrastructure into a single system to speed up deployment. Management expects demand for liquid cooling and next-generation power technologies, including 800-volt architecture, to increase as AI workloads become more power-intensive.

However, EMEA remained Vertiv's weakest region in the first quarter. Organic revenues in the EMEA region fell 29% year over year because the company received fewer orders in the second and third quarters of 2025. Management expects sales to improve in the second half of 2026 as order activity and customer demand recover. If orders remain weak or projects are delayed, EMEA's recovery could take longer than expected and could weigh on Vertiv's overall growth.

How Do Earnings Estimates Compare for NVT & VRT?

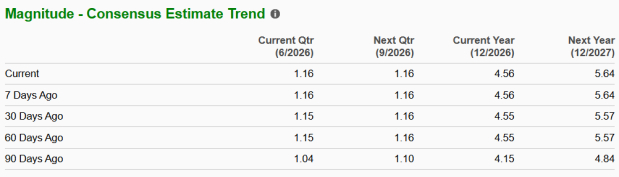

The Zacks Consensus Estimate for NVT’s 2026 and 2027 EPS is pegged at $4.56 and $5.64, respectively. The estimates for 2026 and 2027 have been revised upward by a penny and 7 cents, respectively, over the past 30 days.

Image Source: Zacks Investment Research

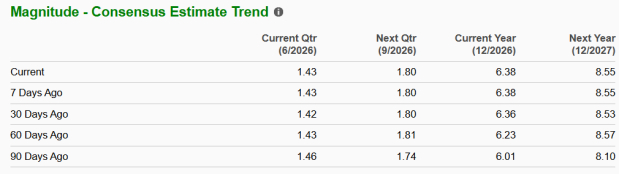

The Zacks Consensus Estimate for VRT’s fiscal 2026 and 2027 EPS is pinned at $6.38 and $8.55, respectively. The estimates for fiscal 2026 and 2027 have both been revised upward by 2 cents over the past 30 days.

Image Source: Zacks Investment Research

NVT vs. VRT: Price Performance and Valuation

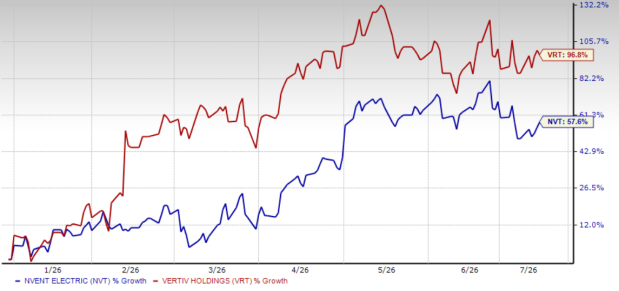

Year to date, shares of nVent Electric and Vertiv have surged 57.6% and 96.8%, respectively.

NVT vs. VRT: YTD Price Return Performance

Image Source: Zacks Investment Research

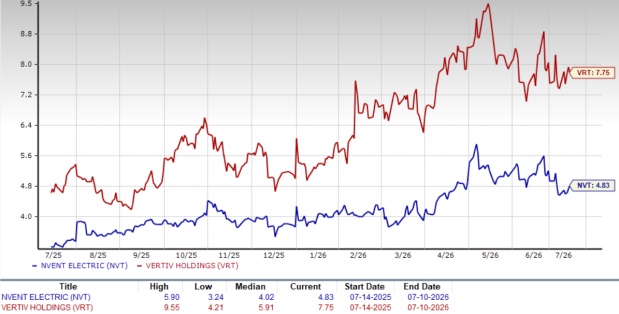

Currently, nVent Electric is trading at a forward sales multiple of 4.83X, lower than Vertiv’s forward sales multiple of 7.75X. VRT does seem pricey compared with NVT. In contrast, NVT’s reasonable valuation makes it more attractive for investors looking for value and stability.

NVT vs. VRT: Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: NVT Has an Edge Over VRT

Both nVent Electric and Vertic are benefiting from higher spending on AI data centers and infrastructure. However, VRT’s near-term prospects suffer from weaker demand in the EMEA region, where the recovery depends on stronger order activity in the second half of 2026.

In contrast, nVent Electric is experiencing strong demand for data center infrastructure, which is helping drive strong orders and a growing backlog. Further, NVT’s reasonable valuation offers some downside protection as well, making the stock an attractive buy.

Currently, nVent Electric sports a Zacks Rank #1 (Strong Buy), giving a clear edge over Vertiv, which carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

nVent Electric PLC (NVT): Free Stock Analysis Report

Vertiv Holdings Co. (VRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).