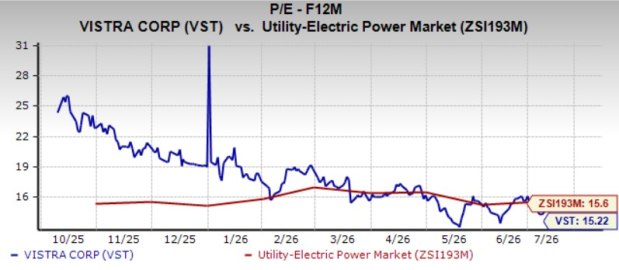

Vistra Corp. VST is currently trading at a forward 12-month earnings multiple of 15.22X, at a 2.42% discount to the Zacks Utility- Electric Power industry’s 15.6X. It is also lower than VST’s five-year median of 17.86X. VST has a VGM Score of B.

VST stock is presently trading at a discount to other industry players like NextEra Energy NEE and Dominion Energy D. NEE and D are currently trading at a higher P/E F12M multiple of 20.97X and 18.89X, respectively.

VST Trading at a Discount

Image Source: Zacks Investment Research

The stock trades at a discount on the forward 12-month P/E multiple, reflecting concerns over wholesale power price volatility, integration risks from acquisitions and the sustainability of elevated earnings.

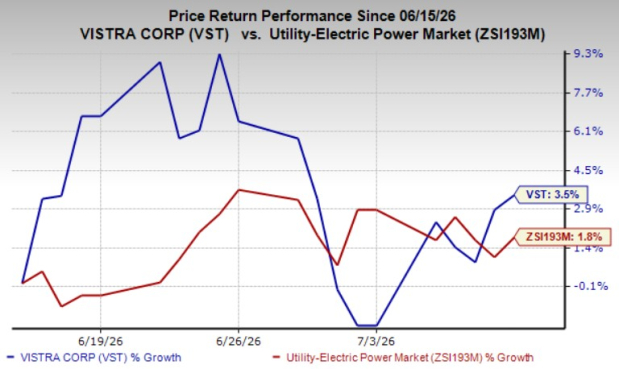

Vistra’s shares have gained 3.5% in the past month compared with its industry’s rally of 1.8%.

VST’s Price Performance

Image Source: Zacks Investment Research

Vistra offers an attractive long-term investment case, supported by its diversified generation portfolio, disciplined capital allocation and growing exposure to rising electricity demand from AI-driven data centers. The company also benefits from long-term power contracts and strategic acquisitions that strengthen earnings visibility.

While Vistra trades at a discounted valuation and has delivered recent share price gains, are these factors alone enough to justify buying the stock? Let's explore the key fundamentals that can help investors determine whether VST is a worthwhile addition to their portfolio.

Tailwinds Enhancing VST's Long-Term Prospects

Vistra is well positioned to capitalize on rising electricity demand driven by the rapid expansion of AI-powered data centers and increasing electrification of oilfield operations in the Permian Basin. Supported by nearly 44,000 megawatts (“MW”) of diversified generation capacity spanning natural gas, nuclear, coal, solar and battery storage, the company can reliably meet growing commercial and industrial power needs while advancing the transition toward cleaner energy.

Vistra continues to enhance earnings visibility through a disciplined hedging strategy and long-term power contracts. As of May 1, 2026, the company had hedged nearly 98% of its expected generation volumes for 2026, around 89% for 2027 and nearly 65% for 2028. Additionally, management expects almost half of adjusted EBITDA to be generated from stable, recurring sources, including long-term wholesale agreements and its retail electricity business, supporting predictable cash flows and earnings stability.

Vistra's long-term power purchase agreements with Meta and Amazon Web Services are expected to support sustained growth. These contracts secure predictable, recurring revenues, enhance earnings visibility and reduce exposure to wholesale power price volatility. As AI-driven data center demand continues to rise, the agreements with investment-grade customers strengthen cash flow stability and support Vistra's long-term financial performance.

Vistra’s ability to generate strong free cash flow continues to boost its performance. For 2026, the company expects adjusted FCFbG of $3.9-$4.7 billion, supported by strong liquidity. This financial strength enables Vistra to continue buybacks while investing in high-return growth opportunities, including nuclear energy, solar and storage projects, and the full ownership of Vistra Vision.

Headwinds for Vistra

Vistra's long-term growth remains subject to regulatory approvals, interconnection timelines and the successful execution of acquisitions and expansion projects. Any delays could defer earnings and cash flow growth. Additionally, while its robust hedging program supports near-term earnings stability, lower hedge coverage beyond 2027 increases exposure to wholesale power price and commodity market volatility.

Vistra’s performance has been impacted by a significant incident at its 300-MW Moss Landing battery storage facility in California, which resulted in the facility being completely taken offline.

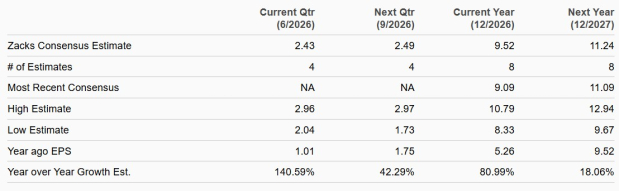

Vistra’s Earnings Estimates Moving Up

The Zacks Consensus Estimate for VST’s 2026 and 2027 earnings per share indicates year-over-year growth of 80.99% and 18.06%, respectively.

Image Source: Zacks Investment Research

The same for D’s 2026 and 2027 earnings per share indicates year-over-year growth of 4.97% and 18.06%, respectively.

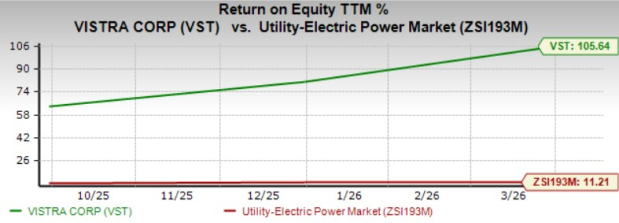

VST Stock Returns Higher Than Its Industry

Return on equity (“ROE”) is a key indicator of a company’s financial performance. It reflects how effectively a corporation uses shareholders' equity to generate profits and is widely regarded as a measure of profitability and operational efficiency.

VST’s trailing 12-month ROE is 105.64%, way ahead of its industry average of 11.21%.

Image Source: Zacks Investment Research

NEE’s trailing 12-month ROE is 12.25%, also up from its industry average.

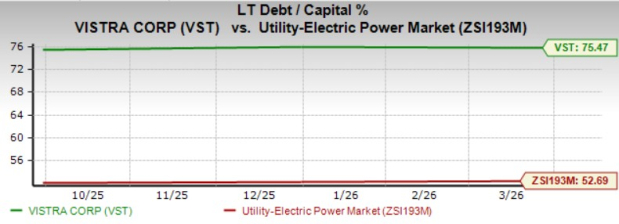

VST’s Long-Term Debt to Capital

Vistra’s long-term debt to capital is currently pegged at 75.47%, much higher than its industry average of 52.69%.

Image Source: Zacks Investment Research

Wrapping Up

Vistra offers an attractive long-term investment case, supported by its diversified generation portfolio and growing exposure to rising electricity demand from AI-driven data centers. The company also benefits from long-term power contracts and strategic acquisitions that strengthen earnings visibility. The free cash flow generation capacity and shareholder-friendly initiative make the stock attractive.

However, Vistra faces risks from wholesale power price volatility, integration challenges related to acquisitions and uncertainty over the sustainability of its elevated earnings. The company also carries higher long-term debt than many of the industry peers, while the shutdown of the Moss Landing energy storage facility following the accident could weigh on its long-term growth prospects.

Considering these concerns, prospective investors should remain on the sidelines and wait for a more favorable entry opportunity before adding VST to their portfolios. Vistra currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vistra Corp. (VST): Free Stock Analysis Report

NextEra Energy, Inc. (NEE): Free Stock Analysis Report

Dominion Energy Inc. (D): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).